Last year, the California Public Utilities Commission launched an effort to grapple with how the rise of distributed energy resources, third-party energy services business models, and community-choice aggregators were fundamentally altering the state’s energy landscape — for good, or potentially, for ill.

As a regulator with the mission to keep energy affordable, reliable and decarbonized, the CPUC’s main concern was how these trends are taking market share and power away from the state’s investor-owned utilities, which it regulates, and putting it into the hands of third parties over which it may or may not have control.

On Thursday, the CPUC’s Policy and Planning Division released a new white paper on this “California Customer Choice Project,” condensing the past year’s learnings into a set of history lessons, along with a list of potential pitfalls — and a few possible solutions — for a state that’s rapidly approaching a turning point on this path.

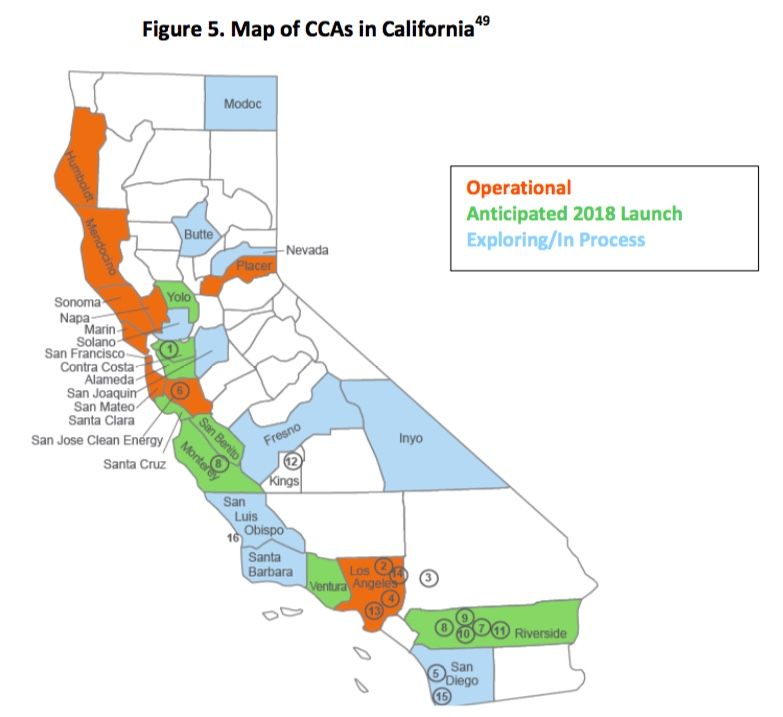

Distributed net-metered solar, community-choice aggregators (CCAs) and “Direct Access” customers are expected to account for as much as 25 percent of retail electric load as of this year, according to CPUC data. That share could grow to as much as 85 percent by the mid-2020s, based on projections of the rapid growth of behind-the-meter DERs, as well as the rapidly expanding roster of cities and counties seeking CCA status.

“Californians have signaled in a variety of ways that they like choice over how they get their electricity,” CPUC Commission President Michael Picker, who launched the customer choice project last year, said in an interview this week. “But what are the best ways to give them that choice and still achieve all our goals? That’s a very hard thing to answer.”

As with a similar white paper that launched the customer choice project last May, this week’s report has far more questions than answers. In a written introduction, Picker laid out some of the key high-level questions, including:

- “How do we protect safe delivery of electricity to meet customer demand in an increasingly fragmented market?”

- “How will we ensure that increasing fragmentation of suppliers and buyers will add up to meet our ambitious clean energy goals?”

- “How will we make sure that different players are meeting their responsibilities to provide all the energy resources we need to make the grid work?”

But amidst its questions, this week’s white paper does contain a few strong policy suggestions, some that would require new legislation, and others that are part of proceedings already underway at the CPUC, the California Energy Commission and state grid operator CAISO.

Key ideas include an integrated procurement process for the state, exploring regionalization of energy markets beyond the state’s borders, and defining what happens if a third-party energy provider gets big and then fails. “I would expect to see proposals later this summer to take care of some of these issues,” Picker said.

The CPUC will be holding a workshop in the coming months to discuss the new white paper’s findings. Picker said he expects it to be a forum for DER providers, CCA advocates and proponents of increased direct access to energy markets to explain how they’re intending to help solve the problems it identifies.

Avoiding a repeat of the 2001 energy crisis

Some of the goals can be summed up fairly succinctly. “We don't want to have the lights go out, and we don’t want to have massive price increases,” Picker said — a nod to the state’s own disastrous history with energy deregulation in the 1990s.

Much of the white paper is dedicated to a history of this flawed deregulation plan, the resulting energy crisis of 2000-2001, and the responsive creation of the regulatory structures that still guide the state today. Those include resource adequacy requirements, the loading order and preferred resources, the state’s renewable portfolio standard, utility power-purchase agreements with independent power producers, frozen residential rates, caps on direct access, and the rest.

The report also delves into four other markets that have deregulated to one degree or another — New York, Illinois, Texas and the United Kingdom — with an eye toward which aspects of their implementations are helpful, cautionary, or inapplicable to California’s unique set of circumstances.

California’s investor-owned utilities Pacific Gas & Electric, Southern California Edison and San Diego Gas & Electric still serve about 84 percent of the state’s load, compared to 16 percent by public or municipal utilities and 12 percent by CCAs.

But the ranks of CCAs have grown dramatically in the past few years to include eight operational entities, with more than a dozen more being formed or expanded at present. For PG&E, the share of load served by CCAs territory has jumped to nearly 20 percent, starting with Marin Clean Energy and Sonoma Clean Power, and expanding to new CCAs being proposed in Silicon Valley and the East Bay. While Southern California Edison still hasn’t seen much of an impact, the planned formation of the Los Angeles County Community Choice Energy could change that dramatically.

On the larger commercial and industrial side, California’s Direct Access program was heavily restricted after the 2001 energy crisis, and now stands at about 13 percent of statewide energy load. These larger customers are served by electric service providers, or ESPs — some of which also implement CCAs for the communities that have created them.

One of the biggest problems with this shift is that the investor-owned utilities still remain the provider of last resort in case a CCA or an ESP fails. “One of the lessons of the last electricity crisis is that SDG&E had to absorb a lot of customers really quickly from the failure of electric service providers in 2001, and that meant they had to be buying a lot of electricity in the spot market for customers they didn’t know they were going to have,” Picker said. “Those kinds of things worry me.”

There’s also the problem with fragmenting reliability requirements among many smaller providers, he said. This has already come up in the area of resource adequacy, or the reserves required to be obtained by all load-serving entities in the state.

“We saw some people who were unable to get all their resource adequacy requirements they needed last summer, particularly in some of the locally constrained areas where it’s not easy to get that capacity,” he said. While the CPUC doesn’t identify which parties failed to secure their RA requirements, 11 waivers were applied for last year, most of them ESPs with little certainty as to how many customers they would have the following year, or whether they’d be in areas facing capacity constraints.

CCAs and ESPs also have much smaller balance sheets and much higher costs of capital than utilities, which makes it much harder for them to sign long-term power contracts, Picker said. “There are more and more challenges emerging as people may not be able to finance long-term contracts, because they’re engaging in short-term markets. […] Most ESPs and Direct Access customers, they may have one-year contracts for big customers that need the contracts this year, but don’t know if they’re going to be there next year.”

That’s a lot different from utilities, which continue to serve customers in the same territories year after year. But “even the utilities don’t know who their customers are going to be next year, because of the CCA formation,” Picker said. “They don’t want to do long-term contracts.”

Key principles and possible solutions

One of the potential fixes to the shared resource adequacy challenge is a statewide procurement process, Picker noted. Illinois created such a procurement structure for the municipal energy aggregators — its version of CCAs — that now serve about 1.8 million of the state’s 5 million residential customers, for example.

Picker also noted California’s controversial idea to expand its grid markets to the broader Western U.S. region as a possible solution. “That could make things work a bit more cheaply, and more reliably,” he said. But there are stark differences of opinion among energy and environmental groups as to whether it would open the state to dirtier energy from the coal-heavy Rocky Mountain region and undermine its carbon reduction goals.

There are also more fundamental issues that need to be addressed, Picker said. For example, California has decoupled its utility revenues and rate structures from the direct sale of electricity. But it hasn’t yet decoupled the utilities’ financial health from the number of customers it serves, he said.

“We don’t make them indifferent to the fact that other people are taking away their market share,” he said. “That’s easy to fix if the legislature is willing to” — perhaps, he suggested, by lifting the current $10-per-month cap on fixed charges to cover fixed distribution system costs, or instituting demand charges for different elements that are driven by congestion.

California’s investor-owned utilities have also been influential in executing clean energy goals, from the RPS and loading order, to their energy storage and EV infrastructure investment plans.

“There is a question whether the necessary capital investment needed to decarbonize the electric sector to meet the state’s 2030 goals and beyond can be financed and, if so, delivered on time if the state transitions away from a few larger buyers to many small buyers,” the report noted.

Beyond the sheer scale of the investment needed, there’s the matter of whether the CPUC has power to impose those same priorities on CCAs, ESPs or Direct Access customers, Picker noted. Right now, the CPUC doesn’t even have the authority to adjudicate customer complaints or billing disputes between load-serving entities and their customers, as it does over the utilities and their customers, the paper noted.

“In theory at least, CCAs should harness the sense of community and local elected officials to do more than just resell electricity,” Picker said. “They should be doing things to help people commit to electrification of transportation, to decarbonize and electrify buildings.”

Of course, CCAs and their backers have long said that one of their main motivations has been to push beyond the utilities' clean energy goals and purchase renewables more directly. The paper notes that “CCAs have argued that having local control will yield lower rates, a greener grid, better service, more technological innovation, greater distributed resources such as behind-the-meter and more rapid response to customers’ needs. Metrics need to be established to ensure that the statewide goals are met as well.”

41

41

15

15

9

9