The solar PV industry is in considerable flux. Overbuilt manufacturing capacity, stagnant inventory and weak global macroeconomic conditions have significantly altered long-held industry fundamentals. Polysilicon, in scarce supply over the last four years, is now readily available. Inventories have become bloated, and prices have fallen sharply across every step of the value chain. Players with sub-optimal cost structures are being tightly squeezed, forcing some to outsource production through contract manufacturers. The balance of power has shifted from module producers to project developers, leading to a scramble towards downstream integration by many upstream companies. Consolidation is beginning to rear its head with news of acquisitions and mergers, and insolvencies may not be too far away.

Amid such turmoil, a spate of developments has placed the United States at the cusp on this brave new solar reality. Unlike governments in other leading markets such as Spain and Germany, whose attitude towards solar has visibly soured, policy momentum over the last eight months has been growing ever stronger, both at the federal and state levels. Thus far, however, much of the discussion between policy makers, market participants and industry observers has focused on the growth of end-markets, while precious little space has been devoted to the other side of the coin – i.e., domestic production. Historically, production has tended to make its home where end-demand has been located, as Germany and Japan can attest. In both these countries, attractive subsidy programs generated strong domestic markets, whose development led to a corresponding increase in domestic production capacity. This begs the question as to how the emergence of the U.S. as a major end-market could impact the domestic manufacturing landscape.

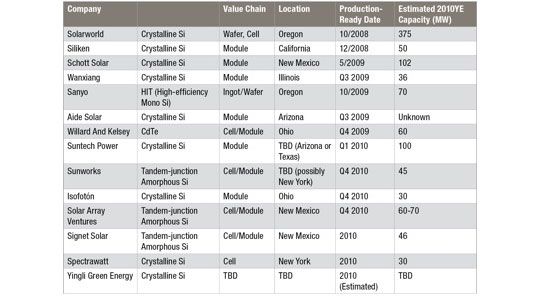

As detailed in GTM Research's recently published report PV Manufacturing in the United States: Market Outlook, Incentives and Supply Chain Opportunities, evidence indicates the momentum is already building: a major trend over the last eight months has been the announcement of new PV manufacturing facilities in the U.S. A few of these, such as Solarworld's giant cell and wafer production facility in Oregon and Schott Solar's module plant in New Mexico, have already been constructed and have commenced operation. Beyond these, there are at least ten major manufacturing facilities in the pipeline that are scheduled to begin production by the end of 2010, as displayed in Figure 1. More crystalline silicon plants were announced in the first half of 2009 than in the previous three years combined, which is clear evidence of the gathering momentum for increasing PV plant construction in the U.S. and points to recent political and policy-related developments as a catalyst. Crystalline silicon-based facilities are owned largely by established European (Isofoton) and Asian (Suntech, Sanyo) producers, while thin-film plants investment is primarily from new U.S.-based entrants (Sunworks, Willard and Kelsey Solar Group).

Figure 1: Newly Announced/Constructed PV Manufacturing Facilities in the U.S.

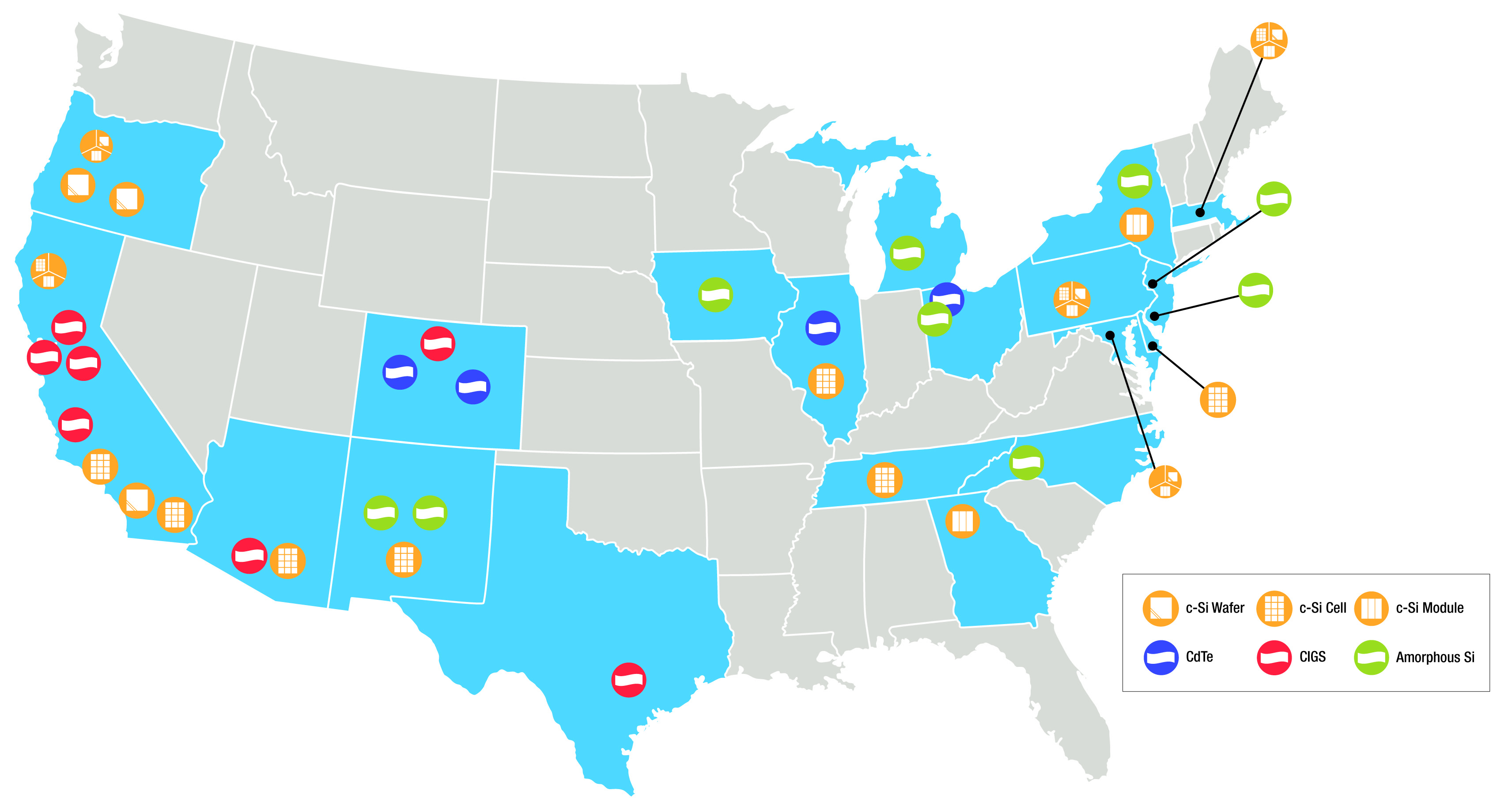

As displayed in Figure 2, the U.S. will contain a total of 37 PV manufacturing facilities by 2012, compared to 26 at the beginning of 2009. Eighteen states will have some form of manufacturing presence in PV by 2012, nine (Oregon, California, Arizona, New Mexico, Colorado, Michigan, Ohio, Massachusetts, New York, and Pennsylvania) of which are expected to have producible output in excess of 100 MW by 2012, compared to only three (Ohio, Michigan, Oregon) in 2009. This is exactly the case for module production as well, meaning that production will no longer be concentrated in a few states as is the case at present. Looking at the value chain participation for crystalline silicon-based facilities, there is a strong trend towards constructing module facilities compared to cell and wafer plants, particularly for foreign companies. This is highly suggestive of expectations by manufacturers of the U.S. emerging as a strong end-market, since modules are the closest step in the value chain to the end-user and locating module production close to demand reduces sometimes hefty shipping costs and drives higher visibility to the customer – which is crucial in such an oversupplied environment.

Figure 2: U.S. PV Manufacturing Facility Map, 2012

Click on the above image to a see a higher-resolution version of this map.

The question that lingers, however, is whether the build-out of PV manufacturing in the U.S. is a short-term fad or a more sustained trend. Definite answers remain elusive, but one can still separate those aspects of the industry that are more prone to transformation versus those having the potential for long-term stability. The U.S. is currently the home base for the development of disruptive, innovative PV technologies. To the extent that the PV technology does not completely mature, this will likely remain the status quo for future generations of technology as well. And there is sufficient evidence to believe that such innovation will continue – as discussed at length in GTM Research's report PV Innovations in North America, there were currently 72 technology-differentiated PV startups in North America as of January 2009, and there are more such firms in the U.S. than in Europe and Asia combined. Whether or not successful manufacturers end up "pulling a First Solar" and focusing on Asian locations for later ramp-ups, they are likely to first scale operations on the domestic front, close to R&D resources and core management. This is indeed the case for the VC-backed U.S. CIGS firms.

As concerns the production of the more mature technologies (both traditional crystalline silicon and certain thin-film solutions, to the extent that they are better understood over time) in the long-term, the future depends on the evolution of many complex and interacting industry dynamics. Firstly, will production continue to follow markets, as has been the case historically? Secondly, will the oft-argued commoditization of the upstream aspects of the industry (wafers, cells, modules) lead to costs and prices emerging as the sole determining factor for buyers, or will there be a place for brand recognition and other non-economic drivers in determining uptake? Thirdly, will the cost spread between U.S./European and Asian production widen or contract over time, and could shipping costs end up having a material say in the final analysis? Fourthly, what role will economic protectionism have to play in the future? To the extent that the Chinese PV subsidy program mandates that eligible modules be domestically produced (as is widely expected, will it lead to a counter-punch by Western nations to drive the adoption of domestically produced components? And could absorption of locally produced modules by Chinese installations create opportunities for producers in other countries?

As industry participants throw all manner of possible solutions to the current turmoil and see what sticks, time will certainly add more color and precision to the eventual outcomes. For now, though, one thing is clear. The old days of European and Japanese production dominance, supply chain bottlenecks, bloated cost structures, and easy feed-in tariff-driven profits are fast dying, and are not likely to return: the industry is in the middle of a rapidly evolving reconfiguration of manufacturing strategies and business models, and companies will have to think on their feet to exploit opportunities to stay ahead of the competition. The first wave of companies behind the re-emergence of a strong domestic manufacturing market in the U.S. as outlined here could in retrospect serve as example of such prescience.

41

41

15

15

9

9