PacifiCorp, the multi-state Rocky Mountain utility that’s been trying to restrict third-party wind and solar contracts under federal PURPA regulations, is now planning a $3.5 billion investment of its own in a wind-powered future.

In a Tuesday filing, the utility owned by Warren Buffett’s Berkshire Hathaway told regulators that it wants to bring an additional 1,100 megawatts of wind power on-line between now and 2020, most likely through power-purchase agreements with projects in Wyoming, where the wind blows strong and steady.

The Integrated Resource Plan also calls for the repowering or retrofitting and replacing of an existing 900 megawatts of wind turbines and building a $700 million, 140-mile long transmission line to connect these resources with customers in Oregon and Nevada, and to the broader Western energy grid.

These short-term investments are part of a much longer-range plan, not covered by the initial $3.5 billion, which calls for 850 megawatts of new wind and 1,040 megawatts of solar power between 2028 and 2036 -- the deadline for PacifiCorp to retire about 3,600 megawatts of coal-fired power plants.

All in all, it’s an important investment in renewables for a utility that’s been getting a lot of criticism of late for its stance on green power. Specifically, PacifiCorp has been asking regulators in the six states where it operates to undercut the way solar and wind power can be financed under the federal Public Utility Regulatory Policies Act, or PURPA, which has become a key driver of green energy investment in the past few years.

In simple terms, PURPA requires that utilities take on renewable power that's cheaper than the "avoided-cost rate" of building new power plants. Just how the law is implemented varies from state to state, but in general, it didn't matter too much until wind and solar costs started falling to the point where they could beat that avoided-cost rate.

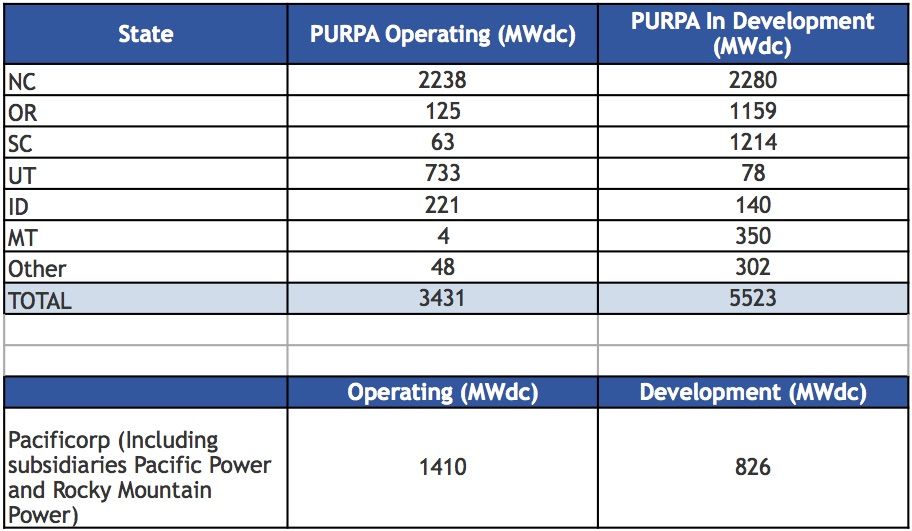

GTM Research analyst Colin Smith predicts that PURPA will be the No. 1 driver of utility-scale solar in 2017 and 2018. “The first real PURPA market was in Utah. The costs of utility solar had finally gone down enough that a number of developers said, 'We can leverage these projects under the avoided-cost rate, and get fixed PURPA contracts.' That led to a bunch of different markets” opening up, he said. Today's active PURPA markets include Idaho, Montana, Oregon, and, notably, North Carolina.

Meanwhile, PacifiCorp and its subsidiaries Pacific Power and Rocky Mountain Power have seen an influx of about 1,400 megawatts of PURPA-enabled renewable energy come on-line, with another 826 megawatts in development, according to GTM Research.

“You’ve got a true boom -- in the terms of a boom-and-bust cycle -- in the market,” Smith said. “PacifiCorp has said, 'We have more utility solar in our connection queue than we have load forecasted for the year.'”

In response, the utility started asking regulators to reduce the number of years for PURPA-driven contracts, which typically run for 20 years, down to as few as two years. It's a timeframe that would be next to impossible to finance, solar advocates say. Idaho regulators approved such a change last year, but a similar request was rejected by Oregon regulators last month.

Even so, the utility’s argument makes some sense, Smith said -- namely, the contention that the law has no upper bound for how much renewable energy it can mandate utilities to accept. If the share of wind and solar grow to the point where they start to cause transmission grid imbalances, costs could rise to the point where “PURPA’s intentions aren’t really being executed properly, in that it is costing the utility more than it is saving them.”

"Pushback against PURPA doesn’t necessarily mean that the utility is against renewables,” Smith noted. PacifiCorp is a prime example -- the utility has procured most of its existing wind power through standard requests for proposals, which allow developers to compete on price to serve the utility's long-term power needs. “There's nothing to date to indicate that they'd do anything differently this time,” he said.

GTM Research analyst Matt DaPrato added, “From a wind perspective, these are pretty big numbers.” First, the 900-megawatt repowering project is across PacifiCorp's entire owned fleet, some of which was installed as recently as 2010. "Replacing turbines at 10 years is pretty much unheard of,” he said. But the benefits will be significant; repowering could result in a 30 percent to 50 percent generation boost, he said.

Meanwhile, the 1,100 megawatts of new wind power is “a full play for the PTC access,” he said, referring to federal Production Tax Credit (PTC) that is set to be phased out slowly over the next four years. In terms of price points, with the PTC, combined with where prices are for PacifiCorp's sister Berkshire utility, MidAmerican Energy, "This is probably $15 per megawatt-hour wind.”

For comparison, the 2015 Department of Energy Wind Technologies Market Report determined the national average levelized price of a wind PPA was around $20 per megawatt-hour.

DaPrato also noted that PacifiCorp is a key participant in California grid operator CAISO’s Energy Imbalance Market, which since 2014 has allowed short-term energy trading between California and a growing number of Berkshire Hathaway-owned utilities, starting with Nevada’s NV Energy.

But the relationship between PacifiCorp’s coal-fired power and California’s green energy goals has so far stymied a broader effort to expand these interstate connections through a regional balancing authority -- an entity that could coordinate day-ahead energy markets across the 36 separate utility-managed transmission systems that make up the Western grid.

PacifiCorp’s big transmission project, dubbed the Energy Gateway, will help integrate California’s market with its Wyoming wind, DaPrato added. Large portions are already done, primarily in Utah, where a rising population and economic growth are increasing energy demand. But “the east and west portions pretty much connect windy Wyoming with Utah and Northern California load,” he said. And so PacifiCorp's big wind plans could very well be a play to take part in the Golden State's renewable energy market.

41

41

15

15

9

9