Residential solar specialist Vivint Solar beat its megawatt guidance, started offering loans and cash sales, and, importantly, showed some positive signs after its near-acquisition and near-death experience with now-bankrupt SunEdison.

This season's earnings calls in the solar industry have been a bit strained -- and stock prices have suffered. (See our coverage of SunPower, Enphase, First Solar and SolarEdge.)

Here are some highlights of Vivint Solar's Q2 financial and operational results.

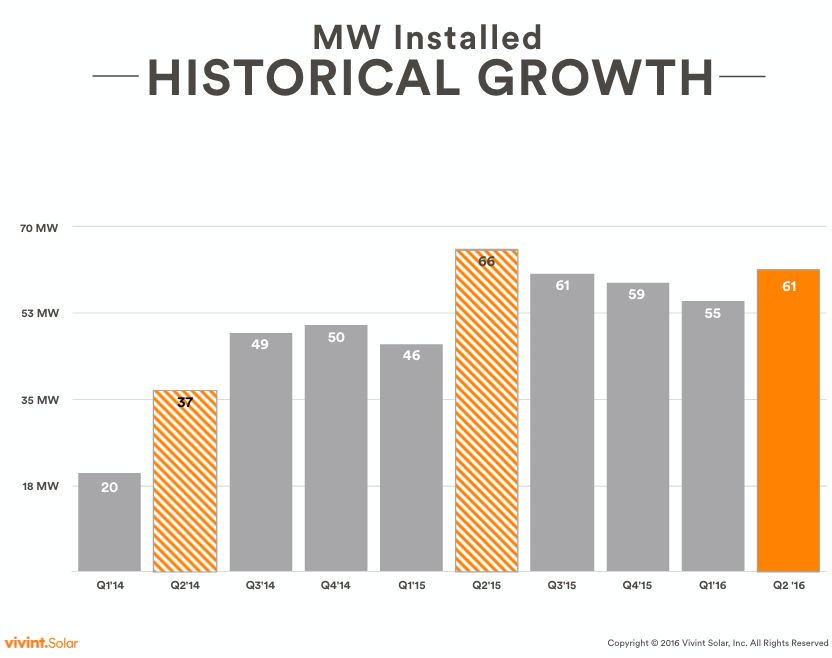

- Vivint beat guidance with 61 megawatts deployed in the quarter, down 6 percent year-over-year

- Revenue grew 116 percent year-over-year

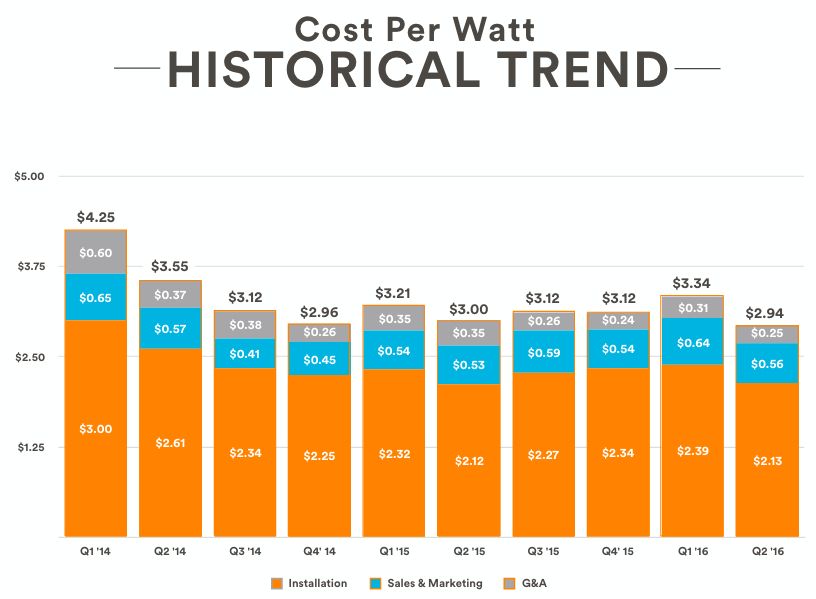

- Total blended cost per watt was $2.94, down from $3.34 in the first quarter, with install cost at $2.13 per watt, sales at $0.56 per watt and G&A at $0.25 per watt.

- 74 megawatts booked for the quarter, remaining flat year-over-year

- Cash sales are expected to grow compared to PPAs

- Loss from operations trimmed from ($72.30) in Q2 '15 to ($36.50) in Q2 '16

- Retained value increased 64 percent year-over-year

- Vivint raised customer prices across half of its service territory

-

As of June 30, 2016, Vivint had $36.5 million in undrawn capacity in the aggregation facility, $125 million in undrawn capacity in the term debt facility, and 32 MW of installation capacity remaining in its tax equity funds. Subsequent to quarter end, Vivint entered into a $313 million term debt facility.

UBS sees trends "indicative that the market is moving away from the SCTY quantity-focused business model of larger MW deployment, toward a more quality- and cost-focused business model."

Oppenheimer Equity observes, "With VSLR’s recent expansion of its term loan facility, we believe the company is demonstrating its ability to close large deals in a relatively short time frame. While the company will need to raise additional tax equity for Q4 '16 and 2017 deployments, we expect the company to close a facility in a timely manner considering the wide availability of tax equity," adding, "This month VSLR closed a five-year $313M term loan facility, which provides back leverage financing for approximately 307 MW ($1.02/W). With higher advance rates that are higher than the aggregation facility, we view the term loan as a sign that debt investors are taking note of VSLR's de-risking of its balance sheet -- and rewarding it appropriately."

Guidance

Vivint "now expects FY 2016 megawatt installations to be below prior FY 2016 guidance of 260 megawatts as it focuses on strategic initiatives to enhance value retained per watt, which include raising customer costs in certain markets, limiting small system installs, and offering higher margin cash and loan sales, which are expected to negatively impact megawatt volumes in the short term."

41

41

15

15

9

9