Germany’s track record with geothermal electricity has been far less dynamic than its impressive history with wind and PV. Only 7.5 megawatts of geothermal electricity have been installed to date [1], compared to over 7,000 megawatts of PV installed in 2010 alone (and again in 2011). [2]

Part of the reason is that Germany is pursuing emerging technologies such as enhanced geothermal systems (EGS) because it does not have a strong hydrothermal resource [3], [4]. EGS involves fracturing hot dry rock deep in the earth to create channels through which liquids can be circulated and heated. This heated liquid is used to generate electricity at lower temperatures, and may use a process such as the Organic Rankine Cycle.

With a weak resource and a focus on an emerging technology, Germany does not expect to secure a significant amount of its electricity from geothermal technologies in the near term. Its national plan projects just ~300 megawatts of geothermal, compared to ~51,000 megawatts of PV, by 2020. [5]

Nevertheless, Germany covers some of the geothermal development risk through two main national policies: (1) the renewable energy market incentive program that supports drilling and district heat networks and (2) the national feed-in tariff (FIT) that provides renewable projects with distinct payments. For geothermal projects, the FIT payments cover a portion of the drilling costs.

Policies that support drilling are important for new geothermal development because resource identification and confirmation drilling are riskier than resource identification for other commercialized RE technologies. Geothermal plants take four to seven years to develop, and the upfront development costs can account for more than 50 percent of total geothermal project costs [6], [7]. Moreover, geothermal prospecting -- surface exploration and exploratory drilling -- can be expensive, and success is not guaranteed. Geothermal projects have exploration success rates of 10 percent to 40 percent [8], [9], and drilling may yield only unproductive or 'dry' wells. As a result, geothermal exploration and projects face high financing costs, if they can be made bankable to interested investors, and many projects will have difficulty receiving any financing.

Therefore, Germany modified its Market Incentive Program (Marktanreizprogramm, or MAP) to assist with geothermal drilling and district heat networks. The German government decided to support drilling new wells by providing early grants and reduced-rate loans to lower the early-stage risks of geothermal development. The program does not cover the full cost of upfront resource exploration or confirmation drilling costs (it is currently being revised but is expected to cover up to 30 percent of the drilling costs). [10]. However, by providing some funding upfront, the government lowers the financial risk of drilling dry wells. There are benefits and drawbacks to an upfront program like this -- the driller needs to have some skin in the game to do their best work, but they may try to inflate costs to get more money upfront, resulting in increased taxpayer burdens.

Importantly, some drilling costs are covered under the FIT payment level as well, once the power plant is operational. Under the German FIT, generators are provided a 20-year, fixed price payment (see graph below) and are guaranteed interconnection. The national utilities must also purchase all of a renewable energy generator's output and dispatch renewable generation into the system before dispatching non-renewable resources. Thus, German project developers do not have to deal with power purchaser risks, because they have certain long-term revenues.

In Germany, FIT payment levels are determined by calculating the levelized cost of energy (LCOE) for each eligible technology over 20 years to make development feasible based on the cost of building a power plant, plus a profit. For geothermal, the FIT has been designed to take the cost and risk of geothermal exploration into account, although payments do not cover the entire cost of drilling. Drilling costs are assumed to make up 47 percent of the project's total installed costs under the most recent version of the FIT [10]. These drilling costs are based on experience from six geothermal projects with 11 production wells and 47,000 meters of drilling. For each project (all of which are smaller than 5 megawatts), drilling costs amounted to between €20 million and €28 million (US $28 million to $39 million). Interestingly, drilling was more expensive than initially thought and drilling cost assumptions were exceeded by as much as 70 percent among the projects for which the government collected data [10].

The German government used a weighted average cost of capital of 9.3 percent when calculating the FIT payment to reflect the costs of capital for some exploration, as well as power plant construction and operation phases. The German government analysis assumed that the exploration phase is 100 percent equity-financed, with a 20 percent return on equity (ROE). At the end of development, a geothermal project is assumed to secure permanent financing with a debt to equity (D/E) ratio of 70/30, an 11 percent ROE and a 6 percent interest rate. The weighted average return on equity from exploration to construction is 12.3 percent, and the weighted average D/E ratio is 59/41 [11].

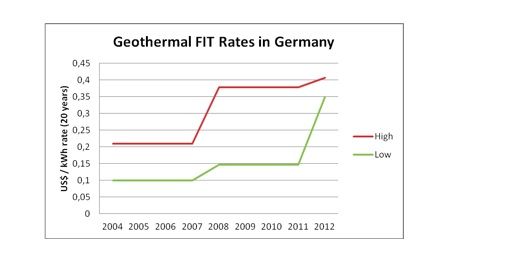

As can be seen in the graph below, Germany's FIT payment levels have evolved over time as the German government has revised the rate to reflect market conditions. Germany differentiates its rates based on different plant types, and the graph contains both the lowest rate available in any given year and the highest rate available. From 2008 to 2012, rates were differentiated by plant size, as well as by technology (e.g., plants that incorporated combined heat and power and EGS technologies). At the beginning of 2012, geothermal payments were simplified to include just two levels: a base rate of €0.25/kWh ($0.35/kWh) and a €0.04/kWh ($0.056/kWh) bonus payment for plants that use EGS. Starting in 2018, the available geothermal rates will decline by 5 percent each year.

As noted, FIT payments do not solve the underlying issues of development risk. But the promise of a secure and predetermined revenue stream may encourage acceptance of more development risk (especially when combined with the upfront grants and/or loans under the market incentive drilling program). Although the German market is not anticipated to grow dramatically because of these revised payment levels, the German Geothermal Association (GtV-Bundesverband Geothermie) believes that development activity does appear to be picking up in response [12].

Given that the United States has a much stronger geothermal resource than Germany, similarly high rates would not be required to drive geothermal development. However, the German approach of using policies to support the upfront cost and risk of well drilling, as well as a guaranteed contract for power plant output, could inform U.S. policymakers interested in supporting geothermal project exploration and development.

***

References:

[1] BMU. (December 2011). “Development of renewable energy sources in Germany 2010: Graphics and tables.” Berlin, Germany. Bundesministerium für Umwelt Naturschutz und Reaktorsicherheit, accessed May 22, 2012 at http://www.bmu.de/files/english/pdf/application/pdf/ee_in_deutschland_graf_tab_en.pdf

[2] BSW. (March 2012). Entwicklung des deutschen PV-Marktes 2010/2011: Auswertung und grafische Darstellung der (vorläufigen) Meldedaten der Bundesnetzagentur nach § 16 (2) EEG 2009 - Stand 22.03.2012. Berlin, Germany: Bundesverband Solarwirtschaft, accessed May 22, 2012 at http://www.solarwirtschaft.de/fileadmin/media/pdf/bnetza_2011_konsolidiert.pdf

[3] Schellschmidt, R., Sanner, B., Pester, S., & Schulz, R. (2010, April 25-29). Geothermal energy use in Germany. Paper presented at the World Geothermal Congress 2010, Bali, Indonesia, accessed May 22, 2012 at http://www.geotis.de/homepage/Ergebnisse/2010%20WGC_Germany.pdf

[4] Miethling, B. (2011). Different but similar: Geothermal energy and the role of politics in Germany, Iceland and the United States. Zeitschrift für Energiewirtschaft, 35(4), 287-296, accessed May 22, 2012 at http://www.springerlink.com/content/w31376444776h742/

[5] Federal Republic of Germany. (2010). National Renewable Energy Action Plan in accordance with Directive 2009/28/EC on the promotion of the use of energy from renewable sources. Berlin, Germany, accessed May 22, 2012 at http://www.buildup.eu/system/files/content/national_renewable_energy_action_plan_germany_en.pdf

[6] Cross, J., & Freeman, J. (2009). 2008 geothermal technologies market report (DOE/GO 102009 2864). Washington, DC: US Department of Energy, Office of Energy Efficiency and Renewable Energy, July, accessed May 1, 2012 at http://www.nrel.gov/analysis/pdfs/46022.pdf

[7] Deloitte. (2008). Geothermal risk mitigation strategies report. Washington, DC: US Department of Energy, Office of Energy Efficiency and Renewable Energy, Geothermal Program, February, accessed May 1, 2012 at http://www1.eere.energy.gov/geothermal/pdfs/geothermal_risk_mitigation.pdf

[8] Augustine, C., Young, K. R., & Anderson, A. (2010). Updated U.S. geothermal supply curve (NREL/ CP-6A2-47458). Golden, CO: National Renewable Energy Laboratory, February, accessed May 1, 2012 at http://www.nrel.gov/docs/fy10osti/47458.pdf

[9] Hance, C. N. (2005). Factors affecting costs of geothermal power development. Washington, DC: Geothermal Energy Association. Prepared for the U.S. Department of Energy, August, accessed May 1, 2012 at http://www.geo-energy.org/reports/Factors%20Affecting%20Cost%20of%20

Geothermal%20Power%20Development%20-%20August%202005.pdf

[10] BMU. (May 2011). Erfahrungsbericht 2011 zum Erneuerbare-Energien-Gesetz (EEG-Erfahrungsbericht) gemäß § 65 EEG vorzulegen dem Deutschen Bundestag durch die Bundesregierung (Entwurf, Stand 3.5.2011). Berlin, Germany: Bundesministerium für Umwelt Naturschutz und Reaktorsicherheit, accessed May 22, 2012 at http://www.bmu.de/files/pdfs/allgemein/application/pdf/eeg_erfahrungsbericht_2011_entwurf.pdf

[11] Weimann, T. (2011). Vorbereitung und Begleitung der Erstellung des Erfahrungsberichtes 2011 gemäß § 65 EEG im Auftrag des Bundesministeriums für Umwelt, Naturschutz und Reaktorsicherheit (No. Vorhaben IIb (Geothermie), Endbericht). Augsburg, Germany: Wirtschaftsforum Geothermie e.V., accessed May 22, 2012 at http://www.bmu.de/files/pdfs/allgemein/application/pdf/eeg_eb_2011_geothermie_bf.pdf

[12] GtV-BG (2012). Website of GtV-Bundesverband Geothermie, the German Geothermal Association, accessed June 4, 2012 at http://www.geothermie.de/

41

41

15

15

9

9