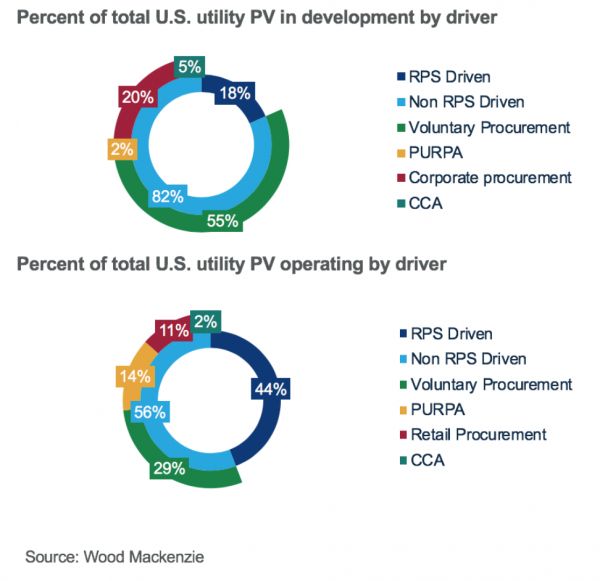

Voluntary procurement of utility solar remains the top driver of U.S. utility PV in development, according to Wood Mackenzie.

WoodMac defines voluntary procurement as procurement based solely on the economic competitiveness of renewables against other energy sources of electricity generation.

The procurement of utility solar by corporate offtakers currently ranks second overall. However, the share of solar purchases driven by renewable portfolio standards to help utilities meet zero-carbon or renewable energy mandates has also grown, representing 28 percent of power-purchase agreement contracts signed in the first half of 2020.

While there is substantive risk of the COVID-19 pandemic affecting the cost of capital for new utility solar projects, utility PV is likely to remain the most economically competitive electricity source in the U.S.

As a result, and despite the stepdown of the federal Investment Tax Credit, voluntary procurement will remain the utility-scale solar industry's largest driver. In other words, Wood Mackenzie still expect utilities to continue signing new utility solar PPAs.

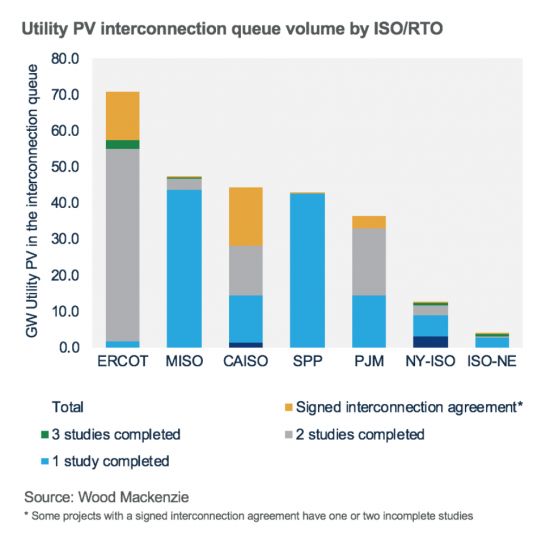

Despite the economic uncertainty caused by the pandemic, the precontract pipeline currently sits at 258.2 gigawatts (DC), with 34 gigawatts' worth of projects already having a signed interconnection agreement in place.

Wood Mackenzie notes that Q1 saw 5 gigawatts of new projects procured in the U.S., a slowdown from 2019 procurement levels but still one of the biggest quarters on record.

Q1 2020 was the strongest Q1 on record in terms of achieving the highest level of megawatts of new utility PV capacity installed in the U.S., according to Wood Mackenzie's Solar Data Hub tool. A total of 2.3 GW came online the first quarter of this year, representing 16 percent of Wood Mackenzie’s 2020 U.S. utility PV forecast.

While there have been a few reported cases of projects being delayed due to factors related to the coronavirus pandemic, developers have, by and large, reported delays are not significant. The pandemic could, however, pose a risk to future projects that have yet to be contracted.

***

Colin Smith is a senior solar analyst at Wood Mackenzie and contributor to the Solar Data Hub.

41

41

15

15

9

9