Natural gas is the Ron Burgundy of energy: kind of a big deal.

Natural gas extracted via hydraulic fracturing now constitutes about 40 percent of all natural gas produced in the U.S., up from almost nothing a decade ago. This is a remarkable increase, taking place mostly in the last four to five years, and made more remarkable when we consider that natural gas has now displaced King Coal as the largest source of fossil fuel primary energy in the U.S.

According to the Energy Information Administration (EIA), it now accounts for about 31 percent of U.S. primary energy production, our largest single source of energy. Natural gas has now surpassed coal production (about 26 percent), is more than the energy from oil production (about 17 percent), and is almost triple the energy we obtain from renewables (11 percent). The shale revolution has yet to reach countries outside of North America, with no other country producing more than 1 percent of its total gas from shale.

Despite this surge, natural gas prices are now at four-year highs above $6/mmbtu, due largely to cold weather snaps and depleting reserves. This highlights both the volatility of natural gas, which was below $2 a few years ago and as high as $13 in 2008, and the fact that those who have been projecting a new era of perpetually cheap natural gas may be wrong.

However, even though this new unconventional gas production has expanded rapidly, we’ve seen a concurrent and rapid decline in conventional natural gas production. As with conventional oil production, it seems that conventional natural gas production peaked in the U.S. back in the mid-1990s. Why does this matter if the total amount of gas production is still increasing? It matters because of the higher costs associated with newer extraction methods -- and because it indicates that the readily available fuel supplies are being exhausted.

There’s a reason companies are increasingly drilling for oil in deep waters or other far-flung locations, and using more expensive and environmentally damaging techniques to extract natural gas. The easily available oil and gas is disappearing.

The reality behind the “shale gale” -- the revolution in shale oil and gas production -- is complex. It’s undeniable that shale gas has ramped up very quickly in the U.S., but it’s far less clear how much more shale gas will ramp up in the future in America or around the world.

There has been a lot of hype around shale gas. It’s important to distinguish between this hype and reliable forecasts from less partial sources. This article will go through the numbers in some detail, in an attempt to get a better feel for the future of energy as it pertains to natural gas production, particularly here in the U.S., which is by far the biggest producer of natural gas from fracking.

Natural gas by the numbers

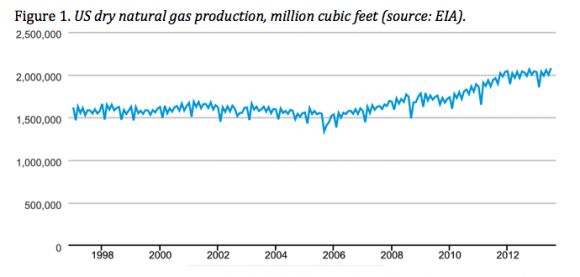

As the figure below shows, natural gas has increased from its recent lows in 2006 by about 33 percent. This is an important number: while very significant, the revolution in shale gas and other extraction techniques has only resulted in a one-third increase in total natural gas production.

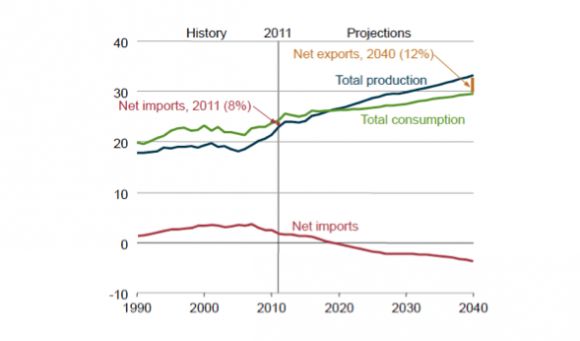

The U.S. Energy Information Administration (EIA) projects no increase in America's natural gas production through 2014 due to current low prices for natural gas. In the longer term, production will rise substantially as prices rise. EIA projects that gas production will rise from about 24 quads to 33 quads by 2040, a 38 percent increase.

Figure 2: EIA projections of natural gas production through 2040, quads (2013 Annual Energy Outlook).

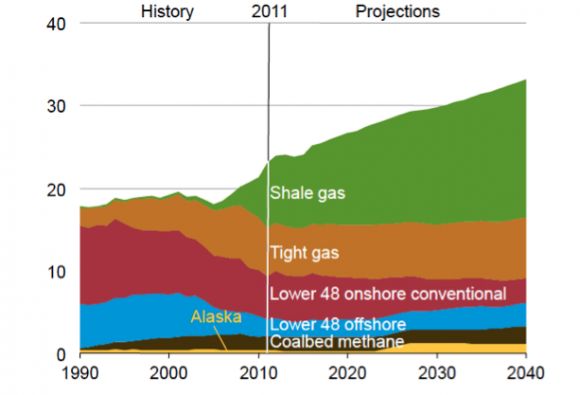

Shale gas and tight gas production has more than doubled in the last four years, due in large part to the fracking revolution and horizontal drilling. Fracking is a technique that uses a mix of pressurized water and various chemicals to free gas from shale and other porous rock formations. It’s a controversial technique, for various reasons, and it is increasingly coming under scrutiny by state and federal regulators.

Figure 3: US natural gas production, in quads, 1990-2040 (EIA Annual Energy Outlook 2013).

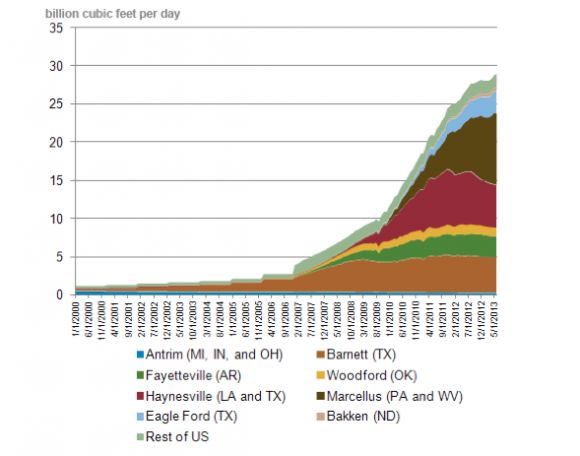

Where does our shale gas come from? Two key formations produce most of the shale gas: the Marcellus Shale in Pennsylvania and West Virginia and the Haynesville Shale in Texas and Louisiana.

The Haynesville formation has reached a clear peak, in 2011, and is declining sharply -- about 40 percent from its peak by the end of 2013. The Marcellus shale continues to see increased production and constitutes the large majority of increased gas production in the last couple of years. The Barnett formation in Texas is third, and this field also seems to have peaked, probably in 2012. The Barnett is where fracking was first developed by local extraction firms and was the biggest field for some time. The fact that a number of major shale gas fields have already peaked is itself pretty telling.

Figure 4: US shale gas production by location (EIA).

EIA’s natural gas forecasts

Forecasting natural gas production, because it is such a large source of our energy now, is an ongoing controversy at the EIA. A New York Times investigation in 2011 obtained internal communications expressing doubt about EIA’s projections for natural gas production. Numerous internal emails and other documents decried undue influence by the natural gas industry in EIA’s forecasts. A sample quote from the article is revealing:

“In the e-mails, energy executives, industry lawyers, state geologists and market analysts voice skepticism about lofty forecasts and question whether companies are intentionally, and even illegally, overstating the productivity of their wells and the size of their reserves. Many of these e-mails also suggest a view that is in stark contrast to more bullish public comments made by the industry, in much the same way that insiders have raised doubts about previous financial bubbles.”

A similar conclusion was reached by Deborah Rogers, former advisory council member of the Dallas Federal Reserve, who has published a report online warning that the shale gas revolution is just another investor-driven bubble.

The EIA is ostensibly independent, since no other agency reviews its reports prior to publication. But as with many government agencies, it seems that the industries that are analyzed or overseen can end up exerting undue influence over the agency through concerted lobbying efforts. Time will tell if this is the case with EIA, though the existing documents revealed by the New York Times suggest strongly that undue industry influence may have been a factor.

There is also some debate about how to calculate current production. One critic has raised the point that EIA’s method is actually a sample of total production, not a comprehensive accounting, and that this sampling method, at least in the case of Texas, has resulted in significant overestimates of actual production.

The controversy around natural gas production forecasting seems to revolve primarily around the projected price of natural gas, due to the fact that the economic viability of shale gas production is thin to non-existent at current prices, and the degree to which existing wells in producing fields are indicative of the ability of new wells in those fields to produce new gas. The next section delves into these issues.

Doubts about the staying power of shale gas

Geologist Art Berman is perhaps the most outspoken critic of the shale gas revolution. Based on EIA’s own data on shale gas resources in the U.S., Berman concludes that there is only about eight years worth of supply left in the ground -- far less than forecast by EIA, which projects dramatic increases in production at least through 2040, the furthest that EIA’s forecasts extend at this point.

According to an article on Berman’s contrarian claims, he “recently studied one area that has been actively drilled for several years and found that 25 percent to 30 percent of the wells drilled that are five to seven years old are already sub-commercial.” Industry typically claims up to a forty-year lifespan for new wells, highlighting a very large potential discrepancy. Many of today’s wells don’t, according to Berman, even cover lease and operating expenses because their production has already fallen too low.

And this is the rub: production in shale gas wells declines extremely rapidly. The average annual decline in the first five years for shale gas is 30 percent to 40 percent, compared to about 20 percent per year for conventional wells. This means that every three years, the entire shale gas production resource needs to be replaced.

Berman also concludes that the commercially viable area of most natural gas fields is about 10 percent to 20 percent of the geographic area. If Berman is even close to being right, the very crude model that EIA uses to project natural gas production will be well wide of the mark. This is the case because EIA projects future production based on geographic area and well density in that area. But if historical production data comes from the 10 percent to 20 percent of the area that is the best producing area, the “sweet spots” as it were, it will not lead to accurate extrapolations for the entire area. EIA attempts to adjust for this effect (as discussed in the 2012 Annual Energy Outlook Issue in Focus #11).

Berman adds that shale gas plays are often unprofitable even when they’re producing at high levels because it costs a lot more to produce shale gas than it does to do so in conventional plays. He has good company in this assessment. Exxon CEO Rex Tillerson has said that “we are all losing our shirts” on shale gas, though he made this statement when natural gas prices were far lower than today.

Berman sums up his view thusly: "We are spending more and more to get less and less." Berman is certainly the loudest critic, and also the source of many other critics’ information about EIA forecasts. As such, it’s important to recognize that his is a minority view and may not be right. The continued increases in production from Marcellus and Eagle Ford formations suggests he may be a bit pessimistic when it comes to the profitability of today’s shale plays.

Time will tell whether EIA’s current forecasts are far too rosy or not. My feeling, on balance, is that EIA’s projections are likely to be on the very rosy side, particularly in years beyond 2020.

EIA’s own track record supports the conclusion that its current forecasts are too rosy. EIA publishes a retrospective study of its own forecasts each year. EIA found that it had, in its “reference case” scenarios, overestimated crude oil production 60 percent of the time. EIA also overestimated natural gas production 66 percent of the time. So EIA’s bias, for whatever reason, seems to be in favor of higher production than has been the case historically.

I’ve not focused in this piece on the environmental issues associated with natural gas production. They are considerable; however, and it may be the case that states become increasingly aggressive in regulating natural gas production. If this does happen, this will impose further downward pressure on future production.

In sum, it looks like we’re likely to see far less natural gas production in the U.S. than EIA and many others are currently forecasting, particularly for years beyond 2020. The good news is that a sustained and sustainable technological revolution is in fact underway in a similar industry: the solar industry.

Solar energy can substitute in many ways for natural gas-fired electricity, particularly when combined with vigorous efficiency and demand response programs. and with the advent of cost-effective energy storage technologies like molten salt thermal storage and batteries. Two recent reports found that various storage technologies in many different configurations will likely be cost-effective by 2015, particularly when the full array of grid services that storage can provide is considered.

Solar combined with storage is a game-changer, and we are on track to reach a substantial portion of our electricity from these technologies by the middle of the next decade if we continue anywhere near the growth rates we’ve seen over the last five years. As with natural gas, there are plausible reasons to believe that solar growth may also slow. But solar installations are only now reaching scale, whereas natural gas production has been at scale for decades, suggesting that the solar phenomenon has a long way to go before it reaches any natural limits.

No one’s crystal ball works that well when we look far out into the future, so I fully acknowledge that this outlook could be off, or wrong. But we need to pay close attention to these issues instead of blindly assuming we have endless natural gas.

Some thoughts on forecasting

I try to be objective in these articles. I’m obviously biased in that I work in the renewable energy industry and I believe strongly that we need to transition quickly away from fossil fuels. At the same time, I believe one can be objective by recognizing one’s innate biases and being fair with the data.

Philip Tetlock, a psychologist at the University of Pennsylvania, has studied expert forecasts and political judgments in detail. He’s found in over two decades of study that most experts aren’t much better than chance in their forecasts. He has found, however, that the experts who are open-minded and draw from a wide variety of sources – a “fox” rather than a hedgehog in his parlance – generally do better than “hedgehogs,” those who are driven by ideology and one or a few “big ideas.”

Tetlock has looked in detail at expert judgment in my primary field, energy, in his book, Expert Political Judgment. An excellent article by Andrew Nikiforuk, a columnist in British Columbia, summarized well Tetlock’s findings regarding energy forecasting:

-- First and foremost, regard all energy forecasts, whether boom or gloom, with radical skepticism. Recognize that many are paid for by dominant energy players in a world where fewer and fewer corporations now control energy flows.

-- Search out humble foxes. They draw their information from a diversity of sources and are accountable for their actions. They tend to be geologists and physicists and not economists.

-- Accept that our energy future will not only be uncertain but largely unpredictable. Unanticipated surprises will shock a highly complex system into unforeseen directions.

I’m taking part in Tetlock’s Good Judgment Project, an exercise in crowdsourcing world affairs political forecasting (my team is currently 1 of 25 teams). As part of this process, participants like me undergo numerous tests. Tetlock’s tests found me to be more fox-like than hedgehog-like, with a score of 2 on a scale of 1 to 7. They also measured “actively open-minded thinking,” and I was a 6.44 on a scale of 1 to 7, with 7 being the most open-minded. Anyway, this is far from definitive proof of my lack of bias, but it should help convince readers that I’m capable of being objective.

***

Tam Hunt is owner of Community Renewable Solutions, a consultancy and law firm specializing in community-scale renewables. Community Renewable Solutions can help developers navigate this complicated field and provide other development advice relating to interconnection, net metering, procurement and land use.

41

41

15

15

9

9