Santa Clara, Calif. -- What is the secret sauce behind Miasole, the maker of copper indium gallium selenide (CIGS) solar modules?

The heart of the company's technology is a large, hexagonal manufacturing machine festooned with valves and rollers that looks like a cross between a particle accelerator and a prop from a science fiction movie. A miles-long metal foil sheet goes in one end, gets turned 90 degrees so that it's vertical, and, in succession, is coated with molybendium, molybdenum, cadmium, indium, selenide and other materials.

It is like watching a multimillion-dollar spin-art machine.

"It produces a module every 90 seconds," said Joseph Laia, Miasole's CEO, during a tour earlier in June.

While solar cells are semiconductors, and many of the processes for making solar cells are similar to those used in chipmaking, the tour reminded me once again that the two industries share distinct characteristics.

The differences:

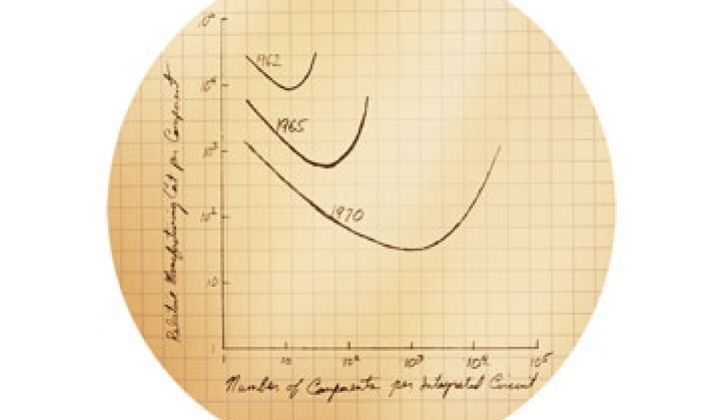

1. Moore's Law Doesn't Exactly Map to Solar. Moore's Law -- the observation made by Intel co-founder Gordon Moore in 1966 that the number of transistors that can be placed on a chip can be doubled every 24 months -- became the foundation of the tech industry, because it laid out a forecast for growth. With Moore's Law, chip makers could feel comfortable plunking down $1 billion or more for a new fab while software developers could sleep without worrying if enough bandwidth would ever exist for swapping movies.

Unfortunately, it also doesn't translate well beyond the realm of computer chips. Why? Moore's Law is all about getting small. Transistors exist to ferry electrons from point A to point B. Thus, smaller transistors mean better performance. They also mean lower costs, because more chips can be popped out of the same finitely sized wafer. Alternatively, designers could add more transistors to a single chip to give it more oomph.

But the "smaller, cheaper, better" concept doesn't work everywhere. If the car industry followed Moore's Law, a Rolls Royce would cost less than a dollar and be as fast as a plane. However, it would also be only a few millimeters high and could barely accommodate a few fleas. In fact, not everything about the dictum works in chips: Moore predicted silicon wafers that would be six feet in diameter by now. The current generation actually measures more in the range of 300 millimeters. (Moore told me in a casual interview in 2003 that Moore's Law has continued to be applicable in part because we "got lucky" with silicon and the way its crystalline structure works.)

With solar, shrinkage doesn't work well. Shrinking a solar cell reduces the surface area exposed to the sun, which directly reduces the amount of power it can generate. In the solar space, at least, smaller is the enemy of better.

"This is not the chip industry. The rate of change is completely different," said Laia. "I don't have Moore's Law...I don't have shrink."

2. It's About Process, Not Products. Although modules might be ornate devices, the fact that they all perform similar functions means that they will ultimately get bought, sold and priced as commodities. Thus, the intellectual property doesn't largely reside in the cells or modules: it relies in the manufacturing equipment and processes, according to Laia. Miasole designs its cell manufacturing hardware itself.

"We make our own coaters," he said. "Between your design and the variety of equipment makers, Intel can differentiate its process from Samsung and TSMC. Their factories can sing and dance at different levels."

Miasole has 105 patents and patent applications and has 50 more coming soon. The company's goal is to file around 100 applications per year.

The opposite situation exists in the semiconductor space: chip makers gave up producing their own equipment years ago.

The "process or product" debate about equipment in solar is contentious and not everyone agrees. The first generation of CIGS manufacturers -- Solyndra, Miasole, Nanosolar, HelioVolt, SoloPower -- spent hundreds of millions of dollars creating their own equipment. Effectively, they had to become Applied Material in order to serve a single, captive customer: themselves.

AQT Technologies built a 15-megawatt CIGS facility for under $15 million with second-hand parts from the disk industry. Telio Solar and NuvoSun are trying something similar.

Then again, look at the SunFab debacle at Applied Materials. It sold similar equipment sets to Signet Solar, Masdar PV and others. The experiment is now winding down.

"The only differentiator is the cost of electricity, and maybe water or labor" among solar manufacturers with the same equipment, asserts Laia.

"Process is indeed everything," writes Travis Bradford of the Prometheus Institute. "Process-tech will determine if you have cheap-enough-but-still-profitable selling prices and [whether you] can continue to deliver those in an ever-falling price market."

Whether this is sustainable-or whether solar manufacturers can "bake" more variety into their cells-- remains to be seen.

3. Diversity. Or, more precisely, a lack thereof. The chip industry started by producing transistors and then integrated circuits. Since then, semiconductor designers have fashioned these basic building blocks into processors, signal processors, amplifiers, FPGAs, converters, actuators, sensors, accelerometers, and a whole range of memory devices.

Solar companies likely won't achieve that sort of diversity. Solar cells and modules ultimately do one thing: convert light into electricity. Different manufacturers will conjure up different types of modules optimized for flexibility, weight, or different light conditions, but all of them will essentially perform the same task.

In that sense, solar ultimately might become something like PCs, a functional tool that can be sold independently or can be integrated with other devices. That's a great future, but the solar industry may not be able to support as many independent manufacturers. Count the number of chip makers and the number of PC makers.

The Similarities:

1. Cost Cuts by Any Means Necessary. Shrinkage is the only driver in the chip industry: Flash memory performance and price declines occurred twice as fast as normal during the last decade because of structural changes in how chip makers introduced new lines of flash. The rise of chip makers in South Korea, Taiwan and China accelerated price declines in unanticipated ways.

The same process takes place in solar, moving from $300 per watt in 1956, to $50 per watt in the 1970s, to $10 per watt in the 1990s, to under $2 per watt today through cell improvements, but also through changes in silicon demand, racking and other aspects of installation.

Even unglamorous things like packaging will be a big deal: Miasole wraps its cells in Lego-like packages that cut the cost of module assembly.

The price declines achieved through these means allows the industry to achieve a rough approximation of Moore's Law, according to SunPower CEO Tom Werner.

2. A Social Set. Why will solar leave wind, biofuels, fuel cells and most other segments of the green industry in the dust? The sheer number of people flowing into the industry give it a collective intelligence that will be difficult to stop. Thousands work in the industry and it has expanded from a base in Japan and Europe to encompass the U.S., China and India. You even see the same confrontational chucklehead personality so familiar in the chip industry in the solar space now. Half of the solar execs these days, after all, hail from chip-industry roots.

Intellectual heft can also determine intra-industry debates. Germanium chips provided better performance, but were relegated to the sidelines. Hard drives inevitably will lose ground to solid-state flash memory. Never bet against silicon. Does this mean thin film is dead? The circumstances aren't completely parallel: in chips, silicon was cheaper than germanium while some types of thin film are cheaper than silicon. Still, it bears watching.

3. A Horizontal Horizon. In the middle of the last decade, many solar manufacturers thought the future lay in creating vertically integrated companies that managed every step of production. The ultimate case was OptiSolar, which wanted to perform and control every task from making silicon to managing power plants.

It burned through more than $320 million before cratering.

Don't expect to see that movie again.

41

41

15

15

9

9