The German renewables phenomenon is largely distributed generation.

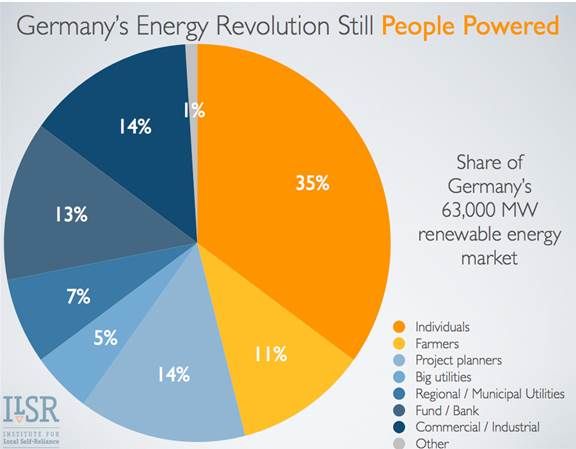

In 2012, Germany’s big four utilities -- EnBW, E.ON, RWE, and Vattenfall -- produced 75 percent of the country’s power, but were responsible for only 5 percent of renewables investments, as depicted by a graph from the Institute for Local Self-Reliance (ILSR). Regional and municipal utilities owned another 7 percent of German renewables. (The original graph is at the German Renewable Energies Agency Information Platform.)

Project planners, better known in the U.S. as developers, made 14 percent of renewables investments.

Over a third (35 percent) of German renewable capacity was owned by private individuals in 2012. The 11 percent of farmer-owned renewables included large ground-mounted solar arrays and sub-utility-scale wind. That is clearly distributed generation, as was the 14 percent categorized as commercial and industrial.

Unlike the U.S., where a huge portion of the residential rooftop market and an increasing part of the commercial and industrial solar installations are bank-owned, German bank ownership, at 13 percent, was mainly applied to renewables in the bank’s portfolio. But because funds are sold to individual investors, some of that was small-business-owned and private-citizen-owned renewables, according to German renewables advocate and journalist Craig Morris.

Bottom line: At least 60 percent of German renewable energy in 2012 was distributed generation.

According to the GTM Research/Solar Energy Industries Association U.S. Solar Market Insight 2012 report, the U.S. built 488 megawatts of residential PV solar in 2012, 1,043 megawatts of non-residential PV solar and 1,781 megawatts of utility-scale solar. Assuming all of the non-residential installations were distributed, that divides U.S. solar into 46 percent distributed generation and 54 percent centralized generation. Adding in 2012's 13 gigawatts of new wind leaves the U.S. with a tiny percentage of new distributed renewables.

Source: GTM Research/Solar Energy Industries Association U.S. Solar Market Insight 2012 report

“The Germans are ahead not because they have better sun, but because they set up a policy framework in which everybody can invest in renewables and come out ahead,” said ILSR’s John Farrell, one of the principal architects of the groundbreaking, just-passed Minnesota solar standard. “It was not tilted toward people who have tax liability or upfront capital. It made it easy to become a renewable energy investor, democratized ownership, and created strong and resilient political support for renewables.”

That kind of feed-in tariff policy has probably not been possible in the U.S. at the federal level, Farrell said. Instead, there have been federal tax credits and state renewables mandates. But a policy like Germany’s, he added, can work at the state level.

“When regulated utilities want to build a power plant, they go to the public utilities commission and get permission to charge ratepayers to build the plant. That is the same thing,” Farrell said. “The German renewables approach just let more people take advantage of it.”

Such a policy could be the right one to replace the federal investment tax credit and production tax credit when they expire, Farrell said.

“In Germany, it was the policy that got everything going. In the U.S., it will be how to keep the growth of renewables going when net metering no longer makes economic sense because the economics of small-scale renewables are too good relative to the retail price.”

41

41

15

15

9

9