[pagebreak:the-network-grid-150 1]

GTM Research is pleased to unveil our latest research report, The Networked Grid 150: The End-to-End Smart Grid Vendor Ecosystem Profiles and Rankings.

This report represents the culmination of a GTM Research effort to profile the leading players in the emerging smart grid market. This work was originally compiled solely for internal research purposes. Later, it was decided that a more finished “vendor bible” might be of use to the industry at large, and so efforts were made to polish the work for wider distribution.

In this 282-page report, we profile more than 150 vendors, providing key data and insights on the leading vendors and firms shaping the future of smart grid deployments around the globe.

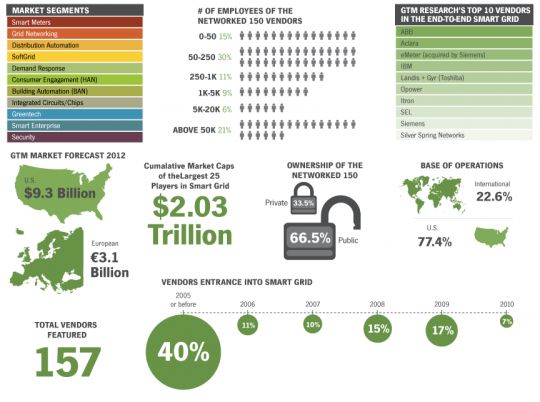

FIGURE: The Networked Grid 150 in Images

Note: Click on link above for larger version of image

Source: GTM Research

Along with profiles and analyst comments, in this report GTM Research also provides two separate Top 10 lists, The Networked Grid Top 10 Vendors in Smart Grid and The Top Ten Vendors to Watch List. Further, this report presents an updated version of our now well-known End-to-End Smart Grid Vendor Taxonomy for 2012, redesigned to include elements of the 'softgrid' space, such as network management, cloud-based solutions and enterprise-wide analytics. In this report we also provide a brief state-of-the-market update, discussing recent trends such as increased M&A activity (including unprecedented market appetite for software solutions), as well as detailing which vendors we view as “Big Fish” based on both market caps and current market positioning. Our Networked Grid 150 report also announces the best companies in the various submarkets of smart grid, including: smart meters, grid networking, distribution automation, software (across all applications), meter data management, consumer engagement technologies (such as home area networks and web portals), and smart utility enterprise systems.

The Networked Grid Top 10 Vendors in Smart Grid

The following list represents our Top Ten list across all of the submarkets of smart grid. While there were close to 25 companies that were in consideration for inclusion on this list, and while the process of whittling down the candidates was by no means easy, the finalists all share a number of key qualities, including: best-of-industry technologies; utility-scale contracts with the largest (and in many cases, the most technologically savvy) utility-actors on the global stage; influence that extends beyond their particular domain expertise; excellent brand recognition and astute product marketing; integrated solutions that maximize utility investment; and, lastly, but of upmost import, an understanding of the changing needs of utilities and the ability to anticipate and address these needs -- not just in 2012, but also in 2015, 2020 and beyond -- with a product-solution mix that supports this large-scale transition.

FIGURE: The Networked Grid Top 10 Vendors

_510_293_80.jpg)

We at GTM Research are continually being asked, “Who is the smart grid all-star team?" The companies on the following pages represent our answer to that question.

To purchase The Networked Grid 150: The End-to-End Smart Grid Vendor Ecosystem Report and Rankings today, click here. Please note: to ensure GTM provides a way to get a useful reference report such as this to a broader audience, we have priced this report substantially lower than our normal rates.

You can receive this report for FREE by registering for The Networked Grid 2012. The Networked Grid 2012 is Greentech Media's 4th annual two-day smart grid summit, held in Raleigh-Durham, North Carolina, April 4–5, 2012. Click here to learn more!

[pagebreak:the-network-grid-150 2]

![]()

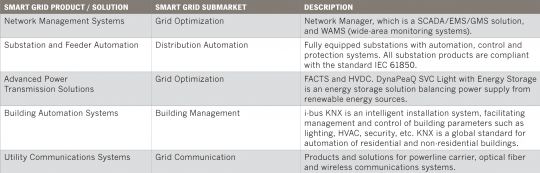

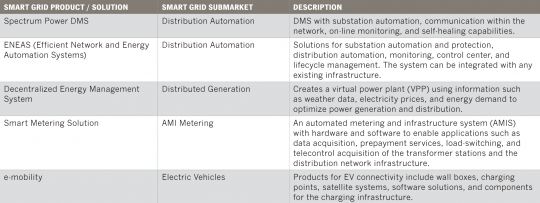

ABB is one of the industrial titans in power and automation technologies, enabling utility and industry customers to optimize their performance. It is very active in integrating distribution management systems into advanced utility control systems. The ABB Group of companies operates in around 100 countries and has been in operation for over 120 years. It claims to have invested over $10 billion in R&D in the last decade to develop a more reliable grid infrastructure, with a particular focus on energy storage. Having extensive knowledge in the technology that enables smart grids, especially power semiconductors, grid automation technologies, and grid communication standards, ABB will continue to be a leading presence in the evolving smart grid market. To date, the primary focus has been distribution automation, but the company is also expanding its solutions within energy storage, network management, distribution grid hardware, FACTS/HVDC, metering and communications, and enterprise software for demand management.

ABB recognizes that the next-generation grid will need to be reliable, efficient and sustainable. The solutions offered by the company to satisfy these needs are a mix of new innovations and conventional electric technology. Some of the smart grid applications that ABB provides include: unbalanced loadflow analysis, fault location, restoration and switching, SCADA/EMS/DMS/OMS/AMI (various systems) integration, Volt/VAR optimization and remote/automatic switching and restoration. These solutions are primarily located in between the distribution network and the utility control room. ABB also offers a variety of other components for smart grid deployments including technology for integration of wind and solar power, electric vehicles (EVs), smart meters, and demand response systems. In addition, the company has long been dedicated to developing interoperability standards for substation automation and protection projects, acting as a driving force in the verification of the IEC 61850 standard, which was announced by DOE Secretary Steven Chu to serve as the initial smart grid interoperability standard for substation automation and protection.

Primary competitors: SEL, Siemens, GE, Alstom, Schneider Electric

Analyst Note: ABB has been on a major buying spree in smart grid over the past few years. In its boldest move, the company made a strategic strike in acquiring major software, data and advisory provider Ventyx, Inc. in May 2010, paying more than $1 billion in cash. This moves ABB into the market for operational equipment and energy enterprise software and greatly expands its share of the global energy management market. Continuing to build on this portfolio, the company has since acquired three more software firms: Insert Key Solutions (IKS) at the end of 2010, Obvient Strategies Inc. in early 2011, and Australia-based Mincom in May 2011. In July 2011, the company made it clear that EVs won’t be left behind with the acquisition of Epyon B.V., a provider of EV charging infrastructure solutions. ABB also attained a controlling interest in Validus DC Systems, a firm that provides direct current (DC) power equipment for data centers. As with the other acquisitions mentioned, at the time of the deal, ABB was very enthusiastic about its new purchase. Continuing to put the pieces in place, ABB had previously taken a stake in Power Assure, a company that specializes in developing power management and optimization software for data centers, which suggests that a larger data center/energy efficiency/greentech offering may be in the cards.

Based on all of this activity, one has to imagine that somewhere at ABB’s central office there is a taxonomic chart on the wall with all of the conceivable submarkets and tangential markets of the smart grid space, and that ABB will continue to fill solution gaps one by one. In the overall march to a networked grid, the most obvious hole at the moment for ABB is in communication networking technologies. While the company has to ask itself whether this is an area where it can compete, we would wager to bet that ABB will make a play on either a pure-play networking company or a hardware company that has networking capabilities as part of the overall solution offerings. Lastly, while ABB sold off its metering business to Elster at the start of the decade, it’s possible that the firm could look to go after this part of the market again. AMI is where most of the smart grid action has been over the last five years in the North American market, and all indications are that the European, Asian and South American markets will heat up over the next five years.

To learn more about The Networked Grid 150 report in its entirety, visit http://www.greentechmedia.com/research/report/the-networked-grid-150

[pagebreak:the-network-grid-150 3]

Aclara, a subsidiary of engineering company ESCO Technologies, is one of the top meter data management (MDM) and consumer engagement solution providers in the world. The company also has significant expertise in advanced metering infrastructure and utility networks, as operational efficiency solutions. The company was founded in 1997 and was acquired by ESCO in 2005. Aclara continues to be operated as a standalone company. It serves over 500 utilities in nine countries.

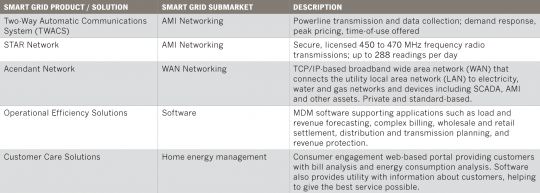

On the networking side of the business, Aclara is unusual in offering both powerline and RF mesh grid networking solutions. Aclara has a powerline data-capture platform called the Two-Way Automatic Communications System (TWACS), used to transmit data between electric meters and the utility. The company has also built out an RF mesh advanced metering infrastructure (AMI) network, called the Aclara STAR Network, using secure, licensed, long-range radio frequencies. Finally, Aclara offers a wide-area network (WAN) solution to connect diverse networks that a utility may have deployed, including AMI, DA, SCADA, HAN, workforce management, and substation automation.

On top of these networking solutions, the company offers a range of software products for applications such as meter data and AMI/meter device management, revenue management, distribution asset planning and analysis, customer care, and efficiency and demand management. Aclara has partnered with numerous major industry players, including GE, Oracle, Elster, Landis+Gyr, Infosys, Honeywell, and Itron.

Aclara is currently in production with Pennsylvania Power & Light to connect the utility’s 1.5 million customers, which includes hourly reads and bridging AMI data with customer billing, along with distribution planning and forecasting. Other recent news of note is that Mexico’s Federal Commission of Electricity chose Aclara powerline AMI networking on a project that will also feature in-home displays. (While outside the bounds of the electric power industry, the company is also involved in the largest AMI deal for gas with Southern California Gas Co.) In a recent independent study conducted by E Source, it was found that Aclara’s consumer-engagement solutions power 15 of the top 25 utility websites; the study also stated that Aclara’s solutions are used by 45 of the 100 utilities that were analyzed.

Primary competitors: eMeter, Itron, Opower, Oracle, Silver Spring Networks

Analyst Note: Aclara continues to be one of the most trusted companies in the smart grid space, offering a product portfolio to rival any company competing in the smart grid submarkets of networking/communications (including AMI), data management and hosting (including MDM) and customer energy information (including both CIS/utility billing and HAN portals). While its powerline networking solution may be a hard sell in the U.S. compared to RF mesh systems, we expect it to be very attractive in Western Europe and potentially China, where powerline continues to be the dominant method of grid communication. As noted, Aclara is one of the few companies in the world to currently offer both PLC and RF mesh networking solutions.

To learn more about The Networked Grid 150 report in its entirety, visit http://www.greentechmedia.com/research/report/the-networked-grid-150

[pagebreak:the-network-grid-150 4]

![]()

EMeter makes software that manages the large volume of data coming from smart meters, providing both meter data management (MDM) and advanced metering infrastructure (AMI) integration for utilities’ information systems. Its utility solutions include demand response and real-time monitoring. EMeter reports having over 25 million meters under contract; the firm was launched by the co-founders of wireless meter network provider CellNet Data Systems. The company was founded in 1999 and serves utilities across North America, Europe, and Australia.

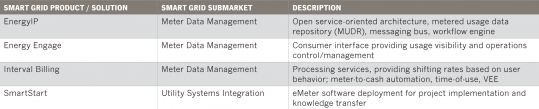

EMeter’s integrated MDM platform is called EnergyIP, which features vendorneutral integration, linking AMI systems to a utility’s information system. EnergyIP software can be installed and configured to a specific liking. EMeter also offers MDM consulting services to support MDMS implementation, as well as Energy Engage, a consumer portal to deliver mobile phone and email alerts, and Operations Management, designed specifically for AMI systems management (deployment planning, asset and outage management, and diagnostics). The company’s MDMS runs on Oracle’s database platform, bundled with an Oracle publish-and-subscribe message bus. EMeter’s solutions also offer SAP integration support, meter installation and tracking, and billing and settlement through its support of SAP Lighthouse meter data unification service (MDUS).

Recent news for eMeter includes its selection by the Long Island Power Authority (LIPA) and National Grid Electric Services LLC for both EnergyIP MDM and the Energy Engage consumer portal, as part of a new smart grid framework for 1.1 million customers. The company has also been expanding into the Asian market, helping integrate meters in a Taiwanese pilot program and inking a partnership with Korea’s Samsung SDS for systems integration and development. EMeter has also partnered with Verizon to deliver cloud-based meter data management, combining MDM with an IP network connected to 200 data centers worldwide. These contract announcements follow the news of the firm connecting 4.5 million meters for Ontario IESO, along with 2 million Itron meters it will provide for CenterPoint Energy in Texas, which include home area network (HAN) support, in a project slated to be complete by 2014.

Primary competitors: Aclara, Ecologic Analytics, Oracle (MDM), Itron

Analyst Note: EMeter is notable for its enterprise architecture perspective on meter data management. Its MDMS combines a data repository with integration software that includes an enterprise service bus and other enterprise information functionality like event processing. Early adoption of a broader suite of tools has positioned the company well for strategic expansion.

Indeed, the battle cry for eMeter can best be described as “beyond meter-to-cash” as the company pursues advanced integrated AMI applications such as integrated outage management, smart meter data analytics, and deep integration with SAP technology. At the same time, eMeter has been stringing together an impressive streak of new client wins and announcements, including: the Kansas City Board of Public Utilities (69,000 electric and 55,000 water meters), the City of Fort Collins, CPS Energy (1.1 million meters), NRGi Denmark (210,000 meters), and WPPI Energy (195,000 meters). Also notable is eMeter’s involvement in the Pepco PowerCents DC project, a dynamic pricing trial that validated the peak reduction potential of critical peak pricing programs. EMeter's professional services played a pivotal project management role in the effort, the result of which are available in a public report.

EMeter can definitely be considered a market leader in defining the MDMS segment. It will be interesting to see how the company's future unfolds as it aggressively pursues market leadership with a venture-capital-backed business model and plenty of strategic partnerships, to boot.

To learn more about The Networked Grid 150 report in its entirety, visit http://www.greentechmedia.com/research/report/the-networked-grid-150

[pagebreak:the-network-grid-150 5]

![]()

IBM is a technology and consulting firm founded in 1911 through the merger of four timekeeping and tabulation companies. Today, the company has expanded to consulting, hosting and infrastructure services, and, most notably, computer hardware and software. IBM is listed as the 33rd largest firm by Forbes and has been awarded the National Medal of Technology and Innovation award eight times.

To facilitate the transition into the smart grid space, IBM has developed a number of solutions to optimize energy use and power generation, and also to open up communications between customers and utilities. It provides communication networks and devices to utilities that help them better understand energy consumption and to view consumption patterns in real time. For example, IBM has provided CenterPoint Energy with an advanced meter system that reads meters every 15 minutes, as opposed to the one-month intervals the utility applied before. The Solution Architecture for Energy and Utilities Framework (SAFE) connects IT to business management and streamlines data collection to give utilities the business intelligence to compete in the smart grid market. IBM also has solutions that work to optimize power generation by installing sensors and communication devices to collect data and providing the proper applications to analyze the data.

Recently, analysts have indicated that IBM may play a large role in the smart grid field, but IBM has been making headlines for different aspects of its activities. It acquired the facility and real estate management software company TRIRIGA in April.

Primary competitors: Accenture, SAS, SAP, Oracle

Analyst Note: As a company, IBM has continued the meteoric rise it has been on over the past three years. Under its Smarter Planet initiative, IBM has extensively built out its ability to use digital technology solutions to modernize the U.S. infrastructure. This is a central reason why Warren Buffet, who in part is famous for avoiding any investment in the high-tech sector, recently obtained $10 billion in IBM stock.

Smart grids are a major component of IBM’s Smarter Planet efforts, and the company has been at the forefront of both software development and integration and, perhaps more importantly (at least for the industry at large) has functioned as a political and educational force to raise awareness for the smart grid’s value to society. All of this goodwill is likely to come back to IBM in the form of profits, as countries like China have extremely large-scale urbanization projects now in full swing and as a host of other markets -- many of which can no longer be referred to as ‘emerging’ -- look to upgrade their infrastructure.

As the race to improve data and business analytics continues to speed up in the smart grid space, it is likely that IBM will remain in the driver’s seat.

To learn more about The Networked Grid 150 report in its entirety, visit http://www.greentechmedia.com/research/report/the-networked-grid-150

[pagebreak:the-network-grid-150 6]

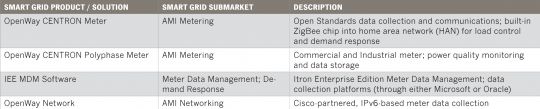

Itron is one of the top smart metering and advanced metering infrastructure (AMI) networking companies in the world. The company is dedicated to end-to-end smart grid and smart distribution solutions for electric, gas, and water around the globe. Itron’s smart metering data collection and software systems are used by nearly 8,000 utilities worldwide. The company has partnered with numerous names for its network solutions, such as Cisco for its open grid platform, along with Tendril, IBM, HP, EMC, Alstrom, Lockheed, Microsoft, and Oracle. A recent partnership with Landis+Gyr will result in the integration of the two companies’ communication technologies into their advanced meters.

Itron uses two-way, unlicensed RF mesh communication in its smart meters, dubbed the OpenWay CENTRON. The meter also includes a ZigBee chip for communication within the home area network (HAN). The company has landed a number of major smart meter deployments, including nearly 5 million meters for Southern California Edison, along with rollouts for Sempra (San Diego), CenterPoint in Houston, and Detroit Edison. Additionally, Itron earns nearly two-thirds of its revenue outside North America, with numerous international contracts held by Actaris, a company Itron purchased in 2008 for $1.6 billion. Actaris offers electric, gas, and water meters in Europe, Africa, South America, and Asia.

In recent news, Itron has been selected by Detroit Edison to provide 800,000 OpenWay smart meters using Tropos Networks networking. Itron scored an even bigger deal earlier this spring when BC Hydro selected the company to provide two million meters for its customers over the next two years. The BC Hydro deal (with networking provided by Cisco) is valued at $270 million. Itron also recently acquired the established French software company Asais, which specializes in energy data management, hoping to expand its end-to-end portfolio. The company has also newly expanded upon a partnership with SAP.

Primary competitors: GE, Landis+Gyr, Silver Spring Networks, Elster, Sensus

Analyst Note: While at first glance, the advent of the age of smart grid and ‘smart cities’ looks like the best thing that could possibly happen to this Spokane-based metering giant, over the long term, the question of ‘Will Itron survive smart grid?’ is an interesting one to pose.

While Itron has been the most dominant player in AMR (last-generation, drive-by style) meters, AMI has forced Itron to move into technologies that historically were outside the company’s core competencies, such as networking, software, data management and cybersecurity. In fact, increasingly, Itron has looked to partner with leaders from these other domains (most notably, Cisco) in the realm of grid communications. Further, and perhaps somewhat surprisingly, a recent partnership with Landis+Gyr (now owned by Toshiba), Itron’s primary competitor, has the company willing to split utility deals by offering different technology pieces of the overall AMI solution.

While all of this is actually very good news for the utility industry as it increases interoperability among the major players (and thereby, in effect, begins to establish a set of de facto standards), it’s unclear whether this is actually in the best interest of Itron. After all, there is a reason why companies, such as Itron, despite their best efforts on the marketing front, have basically resisted open standards. The current trend in metering hardware, i.e., using a system-on-chip (SoC) design and replacing discrete solutions (multiple chips) with a single board, will drive metering hardware closer to commoditization. Further, it highlights the question of what part of smart grid Itron is left holding, as metering profits narrow and as AMI increasingly becomes seen as simply an application of the smart grid, rather than the crown jewel (as perceived by many in the industry three to five years ago).

One area where Itron does appear to be getting it right is in meter data management (MDM). As evidence, the company provides its solution to utilities that use other vendor’s meters and networks (current customers include Southern Company and Nevada Energy [Sensus], Pepco Holdings, Powercor/CitiPower Australia and Florida Power & Light [Silver Spring], and Idaho Power and Bangor Hydro [Aclara]). The company is now attempting to parlay these efforts into the realm of data analytics – the next big growth area in smart grid, as predicted by GTM Research, but to be frank have been slow to enter the analytics game.

While these concerns may be most pertinent in the longer term (and, to be fair, could be asked of any of the legacy metering players), Wall Street has not been kind to Itron over the past three years; presently, its shares are trading around the $30 mark, way off the 2010 peak of $79 and its 2008 peak of $106, which was probably part of the reason why the company’s last CEO was recently shown the door (officially, he retired -- after a mere 20 months with the company). Former CEO LeRoy Nosbaum was then re-instated by the board.

If one of the big players of T&D, such as ABB or Siemens, wants to take control, we can’t help but point out that Itron is now “on sale” at more than 60% off last year’s price.

Despite it all, Itron currently continues to be the dominant player for both AMI, and last generation AMR, meter shipments in the U.S, which gives the company a breadth of utility relationships that most of the vendors in this report can only hope for.

To learn more about The Networked Grid 150 report in its entirety, visit http://www.greentechmedia.com/research/report/the-networked-grid-150

[pagebreak:the-network-grid-150 7]

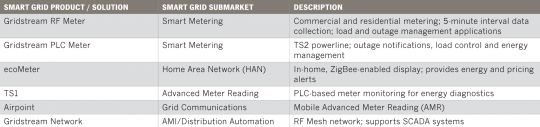

Landis+Gyr is one of the leading smart meter and advanced metering infrastructure (AMI) companies in the world. The company offers a broad portfolio of networking products and services. Landis+Gyr has installed over 300 million meters (this number includes both smart meters and older equipment), with operations in 30 countries. The company was recently acquired by Toshiba for $2.3 billion in cash.

Landis+Gyr calls its networking platform Gridstream. It is capable of being deployed over a variety of channels, including dynamic radio frequency (RF) mesh, ultra-narrow-bandwidth (UNB) powerline communication (PLC), GPRS (2G/3G), 3G, and WiMAX. The company has a substantial focus on distribution automation (DA) and has launched the SCADA Center software application suite in conjunction with DC Systems. Landis+Gyr also has a partnership with broadband communication software company Grid Net to resell their software for meters, switches, and other devices in Australia and New Zealand. (Landis+Gyr has an option to expand the relationship globally.) While RF mesh has been the most popular smart grid networking platform, Landis+Gyr’s capability to scale over various communication channels allows them to market a champion of WiMAX like Grid Net.

Recently, the company landed a grid contract for 10,000 smart meters with the State Grid Corporation of China (SGCC). While 10,000 may sound like a small number, the market in China has vast potential; SGCC covers 80% of the country’s mainland population. If this initial phase is a success, Landis+Gyr and Toshiba are primed to make a major impact on the Chinese market. Another recent announcement concerned a partnership with Itron, where the two companies will integrate each other’s communication technology into the other company’s advanced meters.

Primary competitors: GE, Itron, Silver Spring, Trilliant

Analyst Note: The news of Landis+Gyr being acquired by the Japanese electronics multinational Toshiba made big headlines this year, and not without reason. The acquisition was the largest out of all 226 acquisitions in cleantech in the first half of 2011; it also underscores Toshiba’s commitment to making a splash in the electric power sector, coming just a few short years after its $5.4 billion acquisition of the Westinghouse Electric Co. in 2006.

In this report, we have decided to profile Landis+Gyr, as the brand name will continue exist, and because to date, Toshiba has shown a very light touch with the business operations of its new entity.

Apart from the acquisition news, we have been very impressed by Landis+Gyr’s recent successes and product offerings over the past two years. Projects including Hydro Quebec, JAE, and Nashville Electric Service will utilize technologies in AMI, MDM, managed services, DA, and demand response/load management.

Further, the company has an advantage over several fellow vendors in that its networking platform can function over several different communication infrastructures: powerline carrier, cellular, and RF mesh. As such, the company is less dependent on which communication technology is selected by a given vendor. Landis+Gyr is also positioned at the forefront of the coming AMI/DA convergence, expanding grid communications to all critical devices on the distribution grid.

To learn more about The Networked Grid 150 report in its entirety, visit http://www.greentechmedia.com/research/report/the-networked-grid-150

[pagebreak:the-network-grid-150 8]

![]()

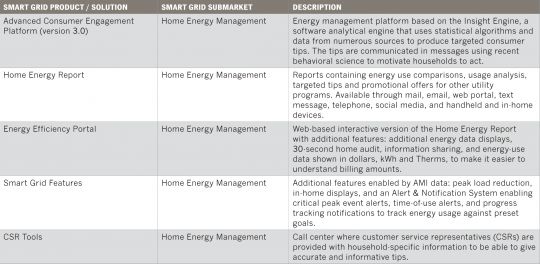

Opower is a relatively young energy management company that has experienced rapid market penetration and growth. It approaches home energy management in a different way than many other companies in the field, aiming to achieve small savings in many households, instead of aiming for larger savings in a targeted population. Its solution is to provide consumers with a framework for making strategic energy management decisions. The strategy used is to display fewer recommendations as more data is collected via increasingly targeted tips and advice. Opower’s strategy has clearly led to success: the company is already working with approximately three dozen utility clients and recent customer announcements include Connexus, AEP Ohio, Puget Sound Energy and Commonwealth Edison.

The primary customer touch point is the Opower web portal, which ameliorates the complexity of advanced metering infrastructure (AMI) consumption data and presents summary information and tailored power conservation recommendations in a user-friendly manner. Key features include an insight dashboard that analyzes usage data and provides actionable tips, an audit feature that gathers information from users via streamlined periodic questions, an efficiency community that users can participate in to share tips and advice, and a dynamic rate comparison tool that can be used to model consumption against different rates to make recommendations on the best plans. The software base for Opower’s products is a profiling engine that gathers, combines and cleans data from sources including tax assessor data, third-party demographic data, GIS data, and weather data to create customer profiles. The company reports that many of its deployments are in territories without AMI, but claims that the platform works even better with AMI data.

Being very focused on results, Opower constantly updates its impact on its website, represented in kWh saved, savings on energy bills, and lbs. of CO2 abated. According to the company, since the launch of the customer engagement portal in 2008, it has achieved more than 375 GWh of total saved energy, equivalent to $33 million. Opower claims its products have been shown to achieve 1.5% to 3.5% of energy savings across the user population and it was recently revealed that the company is considering introducing an automation device into its product suite to achieve even higher savings numbers (currently, its platform does not include any hardware). Opower is also currently working with utilities offering hourly meter reads to be able to start providing peak demand reduction.

Primary competitors: Tendril, Aclara (Consumer Portal), Calico Energy

Analyst Note: It can be argued that the genius of Opower is not technology innovation, but technology packaging. Company founders elected to enter the well-established and relatively static energy efficiency market but with a decidedly web-focused spin. In essence, Opower is an interactive marketing agency that went after a utility business problem: getting consumers to engage in energy consumption. Instead of driving targeted response, Opower drives targeted action, inducing people to adopt energy-efficient lighting, unplug dehumidifiers, and follow through on other tweaks and tips. As a whole, the utility industry has been a laggard in adopting web technology, creating a ripe opportunity for a company like Opower to step in.

At the same time that heavyweights like Microsoft (Hohm) and Google (PowerMeter) flopped with their attempts at consumer energy data management, Opower has taken off. To their detriment, Microsoft and Google tossed their technology into the public domain and figured their brands and clout could get utilities to cooperate by providing access to customer consumption data. This ended up being a deal-breaker, as utilities quickly raised concerns about consumer data privacy. Within weeks of each other, Google and Microsoft pulled out of the market.

To its credit, instead of tossing data management into the public domain, Opower decided to provide a program management solution to utilities that enabled utilities to keep control over their customer data. The stark contrast between the success of Opower and the abject failures of Microsoft and Google is ample fodder for business school case studies. Meanwhile, established utility software companies are left shaking their heads and wondering why and how they have been upstaged by a newcomer.

Whether Opower can retain and grow its existing client base and continue to win new clients remains to be seen, especially as the traditional energy efficiency community begins to scrutinize Opower’s claims (measuring the energy efficiency of various programs is a complex multivariate analytical exercise that is complicated by the number of overlapping programs and market forces at play at any given time). Also, companies like Tendril, EnergyHub and others are beginning to embrace more web-centric business models. Meanwhile, Aclara has also conducted its own independent research project that has achieved similar savings to what Opower claims to have garnered via its own consumer web portal.

Still, Opower has laid down the ante in what is clearly becoming a heavyweight marketing contest to engage consumers in energy management. The real winners in the end will be consumers, who will save money, and the environment, which will absorb less greenhouse gas. Opower lays rightful claim to being an innovator and catalyst successfully changing the way consumers relate to energy.

To learn more about The Networked Grid 150 report in its entirety, visit http://www.greentechmedia.com/research/report/the-networked-grid-150

[pagebreak:the-network-grid-150 9]

![]()

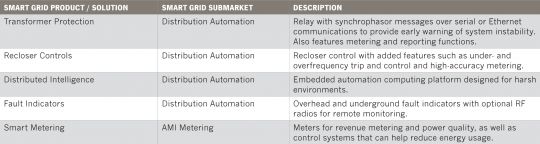

Schweitzer Engineering Laboratories, Inc. (SEL) designs and manufactures products and services for the protection, monitoring, control, automation and metering of electrical power systems. The company serves thousands of utilities worldwide, operating in 140 countries. SEL introduced the world’s first digital relay in 1984, which was a significant upgrade for the power protection industry, offering fault locating and other features at a reduced cost of earlier systems.

SEL’s smart grid portfolio includes monitoring, control and automation systems, resulting in a wide range of smart grid solutions within transmission and distribution, renewable energy, and communication. Many of SEL’s products already have the communications and control capabilities necessary to make the grid smarter and more secure, including transformers, reclosers, communication solutions. A wide range of the products also feature additional smart grid applications such as synchrophasors, interoperability, distribution fault location and integrated metering. SEL offers engineering services to implement its systems and the company expects this division to grow with the growth of the smart grid market.

SEL is one of the partners in Xcel Energy’s SmartGridCity project and has also delivered successful solutions to ComEd (improving distribution reliability for wireless networks) and the Mexican Comisión Federal de Electricidad (providing smart load shedding with synchrophasor solutions). During 2010, SEL cooperated with On-Ramp Wireless to conduct a field test, connecting wireless sensors throughout a 200-square-mile distribution grid, resulting in a comprehensive, real-time performance view of the grid.

Primary competitors: ABB, Schneider Electric, Siemens, GE, S&C Electric

Analyst Note: SEL focuses primarily on control and protection equipment in the substation and out on distribution lines. Few smart grid firms can rival SEL’s technology and commitment to innovation. Since its creation of the first digital relay in 1984, SEL has been on the leading edge. SEL thrives by cultivating and maintaining long-term utility relationships, relying on these close ties to focus research and development investment into clients’ needs.

Digital relaying remains the bread and butter of SEL’s product offering, but promising automated restoration systems enabled with the proprietary Mirrored BitsTM communications protocol have reached restoration speeds rivaled by few in the industry. Only Southern California Edison’s experimental Universal Remote Control Interrupters outclass SEL’s restoration technology by a significant margin, and it would not be surprising if SEL was a vendor partner in the SCE URCI pilot.

SEL believes strongly in the emergence of synchrophasors as a game-changing technology at both the transmission and distribution levels. They have equipped some of their distribution products with PMUs, including their relays and reclosers. A trend toward wide situational awareness on the distribution grid would represent a tremendous revenue boon for SEL.

SEL has expanded its reach by partnering with second-tier vendors to add flexibility to other vendor solutions with the addition of SEL products. For instance, G&W Electric has worked with SEL to enable its LAZER restoration system on SEL’s real-time automation controller. SEL’s private ownership, strong focus on developing advanced technology, and close relationships with utilities will allow the company to continue to produce valuable leading-edge technology that will promote continued growth.

To learn more about The Networked Grid 150 report in its entirety, visit http://www.greentechmedia.com/research/report/the-networked-grid-150

[pagebreak:the-network-grid-150 10]

![]()

Siemens AG is one of the world’s largest electronics and electrical engineering companies, with a worldwide presence spanning over 190 countries and annual revenues of over $70 billion. The company invests extensively in R&D, and smart grid is one of the main focuses of its environmental innovation portfolio. Since January 2008, the company has been divided into three sectors: industry, energy and health care (listed in order of size). The energy sector operates in fossil power generation, renewable energy, oil and gas, service rotating equipment, power transmission, and power distribution.

Siemens is one of the smart grid giants, along with ABB, GE and Alstom Grid. It started with a primary focus on distribution automation and grid optimization, but is spreading its presence into the majority of the other submarkets. It offers all the key products, components, software and automation solutions needed to operate smart grids, covering the entire medium-voltage distribution range up to 52 kilovolts, as well as the high-voltage transmission grid. In addition, Siemens develops electric vehicles (EVs) and their infrastructure, including the cars’ electric drives, battery recharge systems and vehicle-to-grid communication (V2G) technology. It also provides solutions for smart metering, demand response and the integration of renewable energy sources and distributed generation.

Being one of the few suppliers that can claim a complete smart grid solution portfolio, Siemens expects an expanding business in the near future. It is also sharpening its focus on non-European growth markets such as China, India and the U.S., aiming to play a major role in their expanding energy infrastructure. Recent acquisitions to strengthen its energy solution portfolio include eMeter in December 2011, power distribution manufacturer Tesla Power & Automation (not to be confused with the electric vehicle manufacturer) in March 2011 and energy management business Site Controls with affiliate company SureGrid in October 2010. Siemens recently announced that it will form a fourth sector -- Infrastructure & Cities -- integrating parts of the Industry sector and the most smart-grid-technology-intense division of the Energy sector, power distribution.

Primary competitors: ABB, GE, Alstom Grid

Analyst Note: Siemens is aggressively expanding its smart grid footprint to take advantage of growth opportunities in North America and elsewhere. Its acquisition of eMeter continues the consolidation trend underway in the sector. The eMeter acquisition makes good business sense, given the growth that Siemens’ Metering and Communications business unit has played in providing professional services to implement this meter data management software. We will be watching Siemens closely for further developments in this area.

A four-way battle for global domination of the smart grid is heating up between Siemens, GE, Alstom Grid and ABB. Of these, Siemens appears to have the upper hand in North American distribution automation, in addition to a strong European presence. Historically strong in distribution grid equipment -- Siemens sources claim some form of its distribution equipment is in use in most major utilities -- the eMeter acquisition is emblematic of its expansion into the AMI side of the business. We would not be surprised to see Siemens take steps to unify the AMI side of smart grid with the distribution automation side, offering a path for IT-OT convergence.

To learn more about The Networked Grid 150 report in its entirety, visit http://www.greentechmedia.com/research/report/the-networked-grid-150

[pagebreak:the-network-grid-150 11]

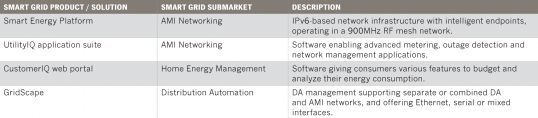

Silver Spring Networks is a leading advanced metering infrastructure (AMI) networking company focused on providing two-way real-time communication between the end-user’s smart meter and the utility’s control and management systems, through an Internet Protocol (IP)-based platform. The company’s solutions are used by many North American utilities, including successful deployments with PG&E, AEP and FPL, which together serve 20% of the nation’s consumers. Silver Spring Networks also serves utilities in Australia and Brazil. Silver Spring partners with a large number of the most prominent smart grid market operators, including Cisco, ABB, GE and Landis+Gyr, which allows the company to offer solutions within most smart grid submarkets. Recently, Silver Spring made the long-awaited announcement to go public, saying it will offer up to $150 million in shares to be traded on the New York Stock Exchange under the symbol SSNI. No initial trading date or opening share price was provided.

Silver Spring’s solutions include the hardware, software and services that connect every device on the smart grid, creating a secure and flexible network infrastructure through its unified IP-based Smart Energy Platform. The platform opens up the possibility for a number of smart grid applications to be deployed by utilities, such as smart metering, demand response, distribution automation and distributed storage. For these applications, the company provides the UtilityIQ application suite and the CustomerIQ web portal software. Silver Spring’s network infrastructure has the possibility of including millions of endpoints, operating in a 900MHz self-configurating RF mesh network. Data from endpoints are forwarded across a utility’s backhaul or WAN infrastructure to the back office, through Silver Spring’s Access Points (APs) and Relays.

Staying out in front of the smart grid market, Silver Spring has been active with EV deployments around the globe. Since 2010, Silver Spring has worked with ClipperCreek to enable the EV company’s charging stations to connect to the smart grid. It also moved into the home energy management space with the acquisition of Greenbox Technology in May 2010. Further, Silver Spring recently launched one of the first global educational programs to inform the public about the smart grid and its benefits, starting in high schools in California and Ohio.

Primary competitors: Cisco, Landis+Gyr, Itron, SmartSynch, Elster, Aclara

Analyst Note: Silver Spring Networks has to be considered the most successful pure-play company in the smart grid market to date. The company has had great success in winning utility-scale deals, as well as in demonstrating the value of their offerings. Even competitors speak highly of the company’s technology and recent successes. Silver Spring’s recent S-1 filing with the SEC revealed that revenues shot up from $58,000 in 2008 to $3.3 million in 2009 to $70.2 million in 2010 (with $115.5 million reported for the first half of 2011) -- impressive growth, to be sure.

However, the financials also revealed an accumulated deficit of $401.8 million, and at the moment, the conversation surrounding Silver Spring is primarily asking whether the company will go through with its planned IPO. Wall Street has not treated companies in the red very favorably in recent months (cf. Comverge and EnerNOC’s stock prices). As such, it seems that Silver Spring must make a compelling case that the road to profitability will be both clear and speedy. (Further, it is likely that the company will need to make the case that beyond communications infrastructure, its add-on revenues from future applications and services via the UtilityIQ applications business will support growing into a platform player). Potentially bolstering the company’s case is the fact that Silver Spring is now showing deferred revenue (for contracts signed but not yet fully performed) of $412.7 million, which could arguably cancel out the deficit concerns. Further, the company currently has more than 25 pilots in place in the U.S., Europe, Asia, and South America.

In light of Toshiba’s recent acquisition of Landis+Gyr, speculation that Silver Spring Network may look to be acquired has been commonplace among many industry observers. If Silver Spring does go forward with its IPO plans, the company will be listed on the NYSE under the ticker 'SSNI.'

In December 2011, Silver Spring Networks went back to its investors for an additional $30 million in debt and options financing, of which it claimed $24 million of the round, according to public filings.

To learn more about The Networked Grid 150 report in its entirety, visit http://www.greentechmedia.com/research/report/the-networked-grid-150

41

41

15

15

9

9