This is the second piece in a series of analyst perspectives related to GTM Research's recently released Thin Film 2012 report. To learn more about this report, click here. To read the first analyst perspective piece, click here.

We can chalk up First Solar as another victim of consolidation in the solar shakeout. After last week's announcement, the industry-leading thin film manufacturer reduced its global workforce by 30 percent and shut down 30 percent of its global production capacity, including planning for the permanent closure of its Germany facilities. Furthermore, in addition to the “indefinite suspension” of 280 megawatts of production capacity in its low-cost plant in Malaysia, the company will selectively idle lines throughout the year to retool for higher efficiencies and yields. Coupled with SunPower’s capacity reductions, First Solar’s woes indicate that the Chinese commodity crystalline pain train continues to wreak havoc on even industry-leading differentiated PV products. Thin-film PV in general is stuck on a precarious precipice; according to GTM Research's latest report on thin-film PV, total market value of thin film shipments could bottom out to near $2 billion in 2012 after reaching heights of $4.4 billion in 2011.

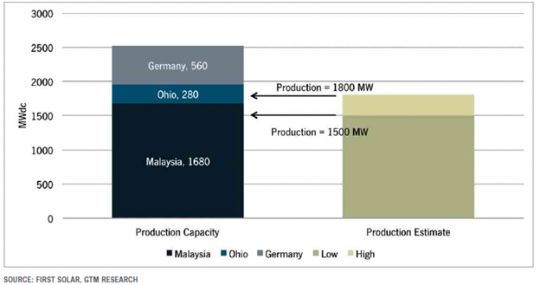

First Solar's move should be unsurprising even to those cursorily following the market. Two trends dominated 2011: the fall of crystalline silicon PV pricing by 50 percent over the course of 2011 and the diffusion of demand out of Europe toward more cost-competitive emerging markets. These trends undermined the value proposition of thin film’s low-efficiency-but-low-cost PV. First Solar Germany’s facility closure was written all over First Solar’s fourth quarter earnings (and continued) production guidance of 1.5 to 1.8 gigawatts in 2012. With Malaysia at nearly 1.7 gigawatts and a healthy North American pipeline to soak up Ohio production, First Solar’s Germany production lines were the odd man out.

FIGURE: First Solar 2012 Annual Production Capacity (Pre-Capacity Closures)

Source: Thin Film 2012–2016: Technologies, Markets and Strategies for Survival (GTM Research)

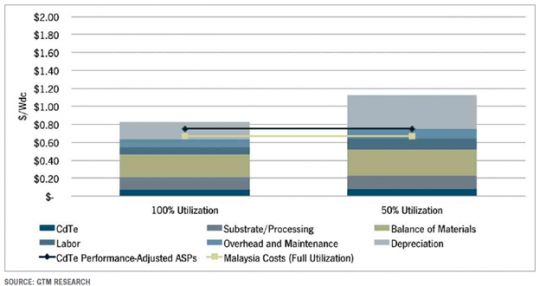

In early February, First Solar idled half of the German plant’s production capacity in a wait-and-see move as German and Italian incentive structures were being debated. With a bleaker outlook on European markets, there’s little justification for continued manufacturing in Germany, especially if First Solar expects underutilization at its cost-leading Malaysia production facility. GTM Research estimates that there’s a 25 percent manufacturing cost difference between the two regions -- and at 50 percent utilization, the fully loaded costs would spiral out of competitiveness.

FIGURE: First Solar Average Production Costs Versus Utilization at Germany Facility, 2012

Source: Thin Film 2012–2016: Technologies, Markets and Strategies for Survival (GTM Research)

However, the bigger question is what do the recent plant closures say about First Solar’s -- and for that matter, thin-film PV’s -- long-term competitive prospects? On one hand, the drop in crystalline silicon prices means that the short-term prospects for First Solar and many thin film companies on the cusp of market competitiveness have evaporated. Reduced demand from falling incentives and a crystalline silicon oversupply environment means that utilization rates for thin-film PV will fall below the already low 52 percent level for 2011. Thin film manufacturers that had their coming out party last year (we’re looking at you, Solar Frontier) will struggle to repeat early commercial success, especially as most of this year’s growth looks to happen in the de facto cloistered Chinese market.

But that doesn’t mean the gig is up for thin film. First Solar’s Malaysia facility still carries the industry’s lowest commercially operating manufacturing costs. Recent efficiency announcements, including First Solar’s 17.3 percent cell and 14.4 percent module as well as Solar Frontier’s 17.8 percent CIGS cell and 13.3 percent champion module (amongst many others) indicate a rising ceiling for technology improvements, even if the records are only at the cell-level or for champion modules. Furthermore, investments in thin film haven’t stopped either; venture capital in thin film has reached $584 million in the past year, signaling continued interest (or rather, not-so-quiet desperation) in thin film, particularly CIGS technology. And since you’re wondering, roughly $300 million came post-Solyndra. Yes, some thin film companies have closed for good, including Odersun and Uni-Solar, and others are in dire straits (see: Solibro tied to an insolvent Q-Cells), but the long-term promise of thin film continues to exist. One side effect of the current supply uncertainty has been reduced valuations on thin film companies, which may increase the attractiveness of a potential buyout and consequently the backing of a strong corporate parent.

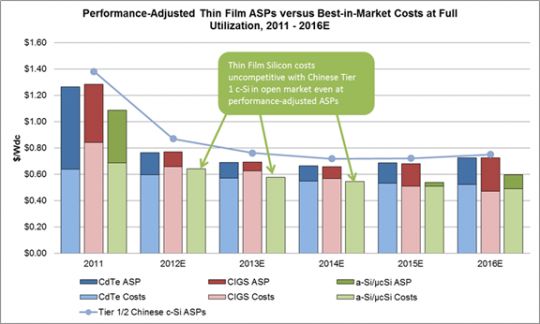

Even after adjusting for lower efficiency (though also for higher kWh/kW performance), best-in-market thin-film PV costs have the potential to be competitive with Chinese Tier 1 crystalline PV in the open market in the next few years. Even if thin film doesn’t take over the market like the industry once imagined it would, there’s still space for thin film manufacturing without having to resort to niche markets, at least for cost leaders. However, until global demand improves, thin-film PV companies will have to creatively jump the bankability hurdle. The road certainly won’t be easy -- thin film firms have much less room for error in hitting important yield and efficiency targets -- but don’t count First Solar, or thin film in general, out yet.

FIGURE: Best-in-Market Thin Film Production Costs at Full Utilization Versus Performance-Adjusted ASPs, 2011–2016E

Source: Thin Film 2012–2016: Technologies, Markets and Strategies for Survival (GTM Research)

41

41

15

15

9

9