For the past year or so, utility-scale solar has taken a back seat to the residential market.

With a flurry of M&A activity, a decreased reliance on state incentives, and steady growth in the residential solar market, utility-scale solar has gotten far less attention. Perhaps this has been appropriate, given the 2013 slowdown in the procurement of utility-scale solar.

Although the days of California utilities buying centralized solar at bloated PPA prices are long past, the first half of 2014 marks a new chapter for the market, thus warranting a second look at its potential.

The market’s rebirth is due to an increasingly diversified demand landscape as utility-scale solar proves to be competitive with natural gas alternatives.

According to GTM Research’s recently rolled-out U.S. Utility PPA Price Tracker, the first half of 2014 has seen utility-scale solar fetch PPA prices between $50 per megawatt-hour and $75 per megawatt-hour.

Amidst this low-priced PPA environment, many opportunities have emerged for project developers, equipment suppliers and project buyers. After poring over the most recent project-level data and RFP announcements listed in GTM Research’s U.S. Utility PV Market Tracker, here’s how developers, suppliers and buyers all stand to gain from the current state of utility-scale solar in 2014.

Project developers

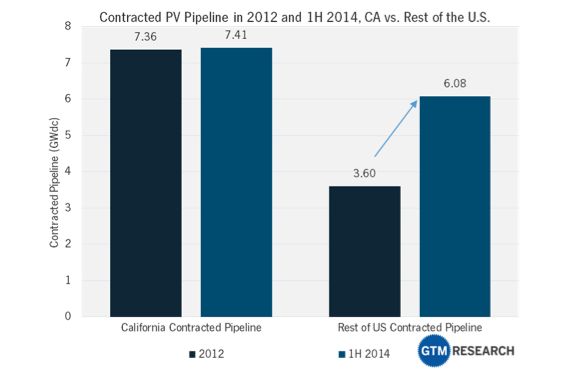

Over the last twelve months, utilities have procured or announced plans to procure nearly 3 gigawatts of centralized solar in some surprising states (i.e., not California).

Source: U.S. Utility PV Market Tracker

As the figure above reveals, at the end of 2012, California accounted for two-thirds of utility-scale solar projects with a PPA in place. Fast-forward to August 2014, and California’s contracted pipeline has grown by only 1 percent, while the rest of the U.S. has grown by a whopping 69 percent.

Successful project developers are cornering new state markets with utilities that are relatively new to solar procurement, some of which had zero utility-scale solar procured through the end of last year.

One example is First Wind in Utah. By offering solar projects to Rocky Mountain Power at prices below that of natural gas generation, the utility snatched up four 80-megawatt PPAs without even conducting an RFP to consider alternative solar projects.

Numerous other utilities outside of California have lined up for large-scale solar projects. Louisville Gas and Electric in Kentucky recently issued an RFP for 10 megawatts of utility-scale solar; Xcel Energy in Minnesota procured 100 megawatts of utility-scale solar in an integrated resource plan; and Nevada Energy proposed owning more than 200 megawatts of utility-scale solar outright.

The list of utilities signing contracts for big solar projects outside of RPS obligations goes on. Here's why:

1. Utility-scale solar is often cheaper than building a new natural gas plant.

2. Utility-scale solar serves as a hedge against natural-gas price volatility.

3. There's been a strategic shift to remove coal from the generation mix.

4. EPA’s coal ash rule is requiring early retirements of certain utilities’ coal fleets.

As evidenced by project-level data found in the U.S. Utility PV Market Tracker, here are the top nine developers to watch in 2014 with aggressive geographic diversification strategies.

Source: U.S. Utility PV Market Tracker

Equipment suppliers

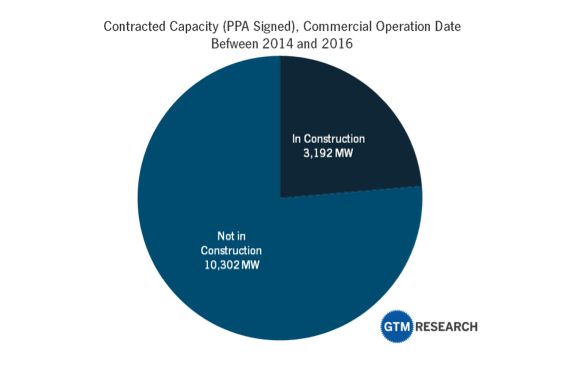

There are now 10 gigawatts of contracted utility-scale solar projects that have yet to begin construction and will soon need equipment supply agreements.

Source: U.S. Utility PV Market Tracker

As mentioned in previous articles, developers are signing a growing number of PPAs with commercial operation dates after the federal Investment Tax Credit is scheduled to drop at the end of 2016. In order to qualify these projects for the 30 percent ITC, developers plan to bring these projects on-line ahead of schedule by signing second PPAs or are considering selling power for one to three years into wholesale power markets before the PPA takes effect.

Coupled with the new wave of utility procurement outside of California, the next three years should be a boom time for inverter and module suppliers targeting the above project developers, which are benefiting from an influx of capacity contracted in secondary state markets.

Project buyers

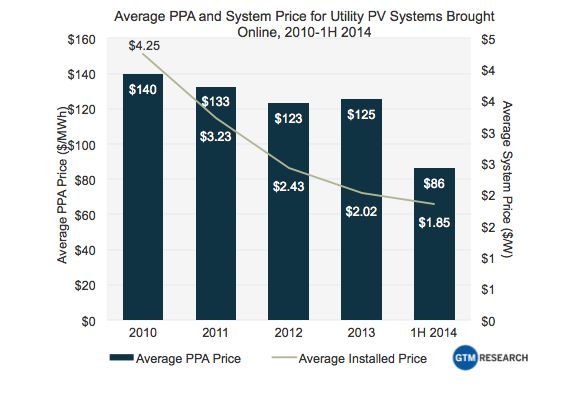

There are also more than 4 gigawatts of operating projects that have PPA prices above $80 per megawatt-hour, while less than 1 gigawatt of projects in development have PPA prices above this price. This indicates that the time to acquire is now.

Source: U.S. Utility PV Market Tracker

As mentioned in previous articles, developers are signing a growing number of PPAs with commercial operation dates after the federal Investment Tax Credit is scheduled to drop at the end of 2016. In order to qualify these projects for the 30 percent ITC, developers plan to bring these projects on-line ahead of schedule by signing second PPAs or are considering selling power for one to three years into wholesale power markets before the PPA takes effect.

Coupled with the new wave of utility procurement outside of California, the next three years should be a boom time for inverter and module suppliers targeting the above project developers, which are benefiting from an influx of capacity contracted in secondary state markets.

Project buyers

There are also more than 4 gigawatts of operating projects that have PPA prices above $80 per megawatt-hour, while less than 1 gigawatt of projects in development have PPA prices above this price. This indicates that the time to acquire is now.

Source: U.S. Utility PV Market Tracker

When a utility-scale solar project secures a PPA, the contract price accounts for expected costs to develop a system that are partly based on the project’s commercial operation date. While each project’s PPA price factors in unique cost assumptions depending on location, offtaker and developer, the above figure reveals that a notable number of systems brought on-line in 2012 and 2013 fetched PPA prices with installation costs below what utilities expected over the last two years. In fact, national average PPA prices for systems brought on-line in 2013 increased slightly over 2012.

As the 4-gigawatt pool of operating utility-scale solar assets with PPA prices above $80 per megawatt-hour dwindles, the time is now for SunEdison, NextEra, NRG Energy, Berkshire Hathaway Energy and other active buyers to look for more acquisitions, since only 1 gigawatt of additional capacity in development offers equally attractive PPA prices.

As the second half of 2014 unfolds, the utility-scale solar market will continue to offer new opportunities for project procurement, supply and acquisition. The top ten developers own 53 percent of contracted capacity for now, but the long-term winners will be those developers who understand the need to enter unchartered state markets, come prepared with efficient cost structures and offer PPA prices competitive with natural gas.

***

Cory Honeyman is a Solar Analyst at GTM Research, where he covers the U.S. downstream solar market with a focus on the commercial and utility scale solar markets. For more information on trends and individual projects in the U.S. utility scale market, see the GTM Research U.S. Utility PV Market Tracker.

41

41

15

15

9

9