One year ago, I wrote a piece here at GTM that argued the solar singularity is nigh.

The “solar singularity” is the point where solar becomes so cheap in a majority of countries around the world that it is established as the default new power source. At this point, solar will very likely go vertical in its growth curve.

During the Paris international climate talks at the end of last year, renewable energy and reduced climate emissions were catapulted briefly into the mainstream spotlight. Unfortunately, there is still a lot of misunderstanding and misinformation, on both the right and left, with respect to the ability of renewables like solar and wind to do the heavy lifting in mitigating climate change without harming economic growth. Hopefully this column will help clarify some of those misperceptions.

My key assertion is that under current cost trends for solar and wind power, and (less certainly) for other renewables and electric vehicles, we are well on our way down a path to dramatically reduced emissions.

Whether such emissions reductions will actually mitigate the worst impacts of climate change remains a very big question. But my hope is that observers and commentators alike will understand that cost declines for many technologies in the last decade have brought us to the point where renewables and EVs are poised to achieve ubiquity relatively quickly.

I made the solar singularity concept the centerpiece of my 2015 book, Solar: Why Our Energy Future Is So Bright. I offer here an update on the topics covered in my book, showing that we are perhaps even closer to the solar singularity than I previously dared to suggest.

I’ll cover not only solar, but also battery storage, electric vehicles and automated driving, which are the parallel and intertwined revolutions that are set to transform our energy system worldwide. With these four technologies developing steadily, we can reasonably expect to see, by 2035 to 2040, a world powered predominantly with renewable electricity -- not only for homes and businesses, but also for transportation and industrial processes.

How close is the solar singularity?

Solar panel prices dropped steadily in 2015. GTM Research calculated average total solar costs for a fixed-tilt utility-scale system at the end of the second quarter of 2015 at just $1.49 per watt DC, down from $1.58 per watt in the previous quarter.

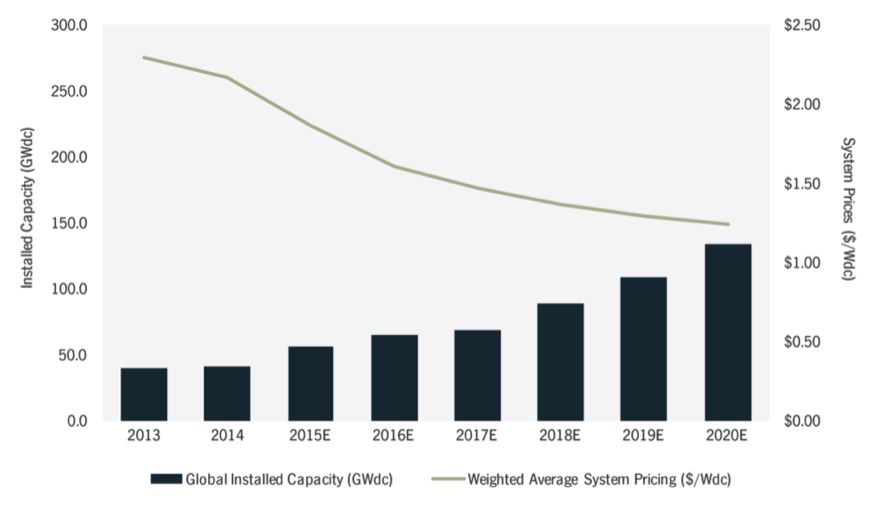

GTM Research forecasts solar prices falling steadily through 2020 and a global market of 135 gigawatts per year in the same year, up from 55 gigawatts installed in 2015. (That is enough to power approximately 10 million California homes.) This growth trend through 2020 constitutes about half (yes, half) of all projected new global electrical capacity in each year.

Even though solar panel prices are still falling steadily, the main area for continued cost declines is shifting to balance-of-system costs, which include equipment other than modules, installation, and the costs of customer acquisition (for the residential side of the business). Balance-of-system costs account for 55 percent of total system cost as of 2015. The chart below shows the projected evolution of costs and installations through 2020.

FIGURE: Utility-Scale Solar Installation and Cost Projections

Source: GTM Research

At $1.49 per watt and 25 percent net capacity factor, we get a levelized cost of electricity (the average cost over the 25-year life of the system) of about 7.3 cents per kilowatt-hour, which includes the 30 percent Investment Tax Credit and accelerated depreciation.

This cost of solar power is highly competitive with fossil fuel and nuclear electricity. The Energy Information Administration calculates in its 2015 analysis that the average U.S. levelized cost for new natural-gas advanced combined cycle plants is 7.3 cents per kilowatt-hour -- the same as solar.

However, to compare accurately, we have to add about 10 percent to the cost of solar to firm up this variable resource. So we’re close to cost parity, but not quite there.

At $1 per watt, the levelized cost falls to just 5.7 cents per kilowatt-hour, well below cost parity with new natural-gas plants. With two-axis trackers and the best solar resources, which increase the capacity factor to 32 percent, that cost falls to just 4.5 cents per kilowatt-hour. We’re headed to $1 per watt as an all-in cost in the next five to 10 years.

These are world-changing developments. Imagine 10 years ago that by 2015 we’d see solar -- solar! -- account for fully half of all new global generation. When we add wind and other renewables into the mix, it's clear that fossil fuels and nuclear are rapidly becoming endangered species.

Renewables provided almost half of all new power generation globally in 2014, according to the International Energy Agency. The agency's executive director, Fatih Birol, summed up the trend: “[Renewables are] no longer a niche. Renewable energy has become a mainstream fuel, as of now.”

Bloomberg New Energy Finance reported last summer that wind power was the cheapest source of power in the U.K. and Germany in 2015, even without subsidies. The article’s tagline reads: “It has never made less sense to build fossil fuel power plants.” The same article highlights the feedback loop that solar and wind power have in terms of reducing the cost-effectiveness of fossil fuel power plants due to the dispatch order of renewables versus fossil fuel plants.

The solar singularity is indeed near (here?) in the U.S. and increasingly around the world. I described previously that 1 percent of the market is halfway to solar ubiquity because 1 percent is halfway between nothing and 100 percent in terms of doublings (seven doublings from .01 percent to 1 percent and seven more from 1 percent to reach 100 percent). The U.S. will reach the 1 percent solar milestone in 2016. We’re halfway there. Buckle your seatbelts.

As always, we can never know with certainty what future years will hold in terms of solar growth rates. But we can be confident that as people realize that solar power is actually cheaper -- even with the additional cost of firming -- the 50 percent of new generation that GTM Research predicts for each year through 2020 will rise rapidly to 60, 70 percent and maybe even higher in each year after 2020.

Wind power is still quite a bit cheaper than solar power, but it’s nowhere near as modular as solar. It also has visual and wildlife impacts that solar doesn’t have. So as the cost curve for solar continues to fall closer to wind power, we can expect solar to increasingly place pressure on wind as well as traditional fossil and nuclear generation.

My expectation, however, is that wind power will grow strongly through 2030 due to ongoing improvements in the technology that are making it more geographically viable around the world.

How close is economically viable battery storage?

A new report from Lazard found that battery storage is currently economically viable for some applications (frequency regulation, for example) even without subsidies. More importantly, the storage industry is set for rapid cost declines in the next five years as various technologies ramp up around the world. The report’s lead author stated that “the energy storage industry appears to be at an inflection point, much like that experienced by the renewable energy industry” a few years ago.

This new report comes on the heels of Southern California Edison's first energy storage procurement in the Los Angeles area in 2014, which included accepted bids for 240 megawatts of projects that were selected based on economics alone (the utility was required to accept only 50 megawatts). We don’t know yet if these projects have been built at the costs bid (that data is not yet public), so we’ll need a bit more time to establish the cost viability of these technologies.

Another new report from Goldman Sachs projects a drop in price for storage technologies by almost two-thirds by 2020.

Energy storage is still a very new market, so my crystal ball is a bit murky when it comes to the future. Most analyses, like Lazard's, use industry-supplied data that hasn’t yet been checked by the market or third parties, largely because there isn't enough publicly available data for such fact-checking.

I agree, however, with Lazard’s conclusion that the storage market is set for rapid cost declines and rapid installation growth in the coming five to 10 years in both the stationary and vehicle domains. The above discussion establishes how rapidly solar is likely to grow around the world in the coming decades, giving some confidence in a steadily rising storage market.

How close are economically viable electric vehicles?

The good news with respect to electric vehicles (EVs) is that many models today are already economically viable with federal and state subsidies. The better news will arrive when costs have dropped low enough that subsidies aren’t required for viability.

The game-changer in this industry is the affordable EV ($35,000 or less seems to be the mark to beat) that has 200 miles or more of range, up from the 80 to 90 miles of range that today’s EVs offer. There are a few major contenders to be first to market: the Tesla Model 3; the Chevy Bolt; and a newer contender, the 2050 Motors all-carbon-fiber e-Go EV.

The Chevy Bolt looks set to beat the Model 3 to market, with the Bolt set for release in early 2017 and the Model 3 for late 2017 at the earliest. (What's more, Tesla has a track record of being a bit later than expected to market.) The e-Go may beat both of them since it’s apparently already in production, but is not yet being sold in the U.S.

The e-Go is revolutionary for another reason beyond being electric and affordable: it’s half the weight of existing small EVs because of its all-carbon-fiber body.

Halving the weight of a car adds about 100 percent to the range with the same battery capacity. So getting to the 200+ mile range category will require a mix of more efficient motors, higher battery capacity and lower overall weight. (An added bonus: the e-Go may be bulletproof.) A future e-Go model could have twice the battery capacity and enjoy 400+ miles of range.

Will affordable long-range EVs allow the market to truly take off?

Interestingly, EV sales are now also at about 1 percent in the U.S. and globally, so we are also halfway to ubiquity for EVs in terms of new sales (but not for fleet composition, as that metric tends to lag behind sales by a number of years). My crystal ball is again murkier for EVs than for solar because the market is still quite new and the game-changing products (affordable long-range EVs) aren’t actually here yet.

I’m not alone, however, in thinking that EVs are likely on a path toward ubiquity. Toyota recently announced its view that sales of traditional internal combustion cars will mostly be phased out by 2050.

How close are self-driving cars?

The big news in the field of self-driving cars comes from Tesla, which unveiled and installed (magically by wire) its autopilot technology last October. The reaction from Tesla owners seems to be generally positive, even though there have been some issues and a few negative reactions. Tesla made clear that its new feature is still in beta mode and is not a full autopilot. It’s not yet known when the full autopilot features will arrive.

Even with the current beta autopilot, however, the self-driving Tesla is highly functional. A recent cross-country test in a Model S took just 58 hours to drive the entire distance, and fully 96 percent of the 3,000 miles was driven by a non-human (i.e., the computer autopilot) at an average speed of 51.8 miles per hour.

Musk has said it will be a few years before full autopilot will be available. There are many technical kinks and regulatory issues that still need to be worked out before people can literally call up a car and arrive at their destination without driving themselves. This future seems assured. But the timing is still quite uncertain due to the difficulties in teaching software about unusual driving situations and adverse driving conditions.

Musk has also highlighted the importance of autopilot to him and to Tesla. "I will be interviewing people personally and Autopilot reports directly to me. This is super high priority,” Musk recently tweeted.

My best guess for the arrival of fully automated vehicles is between 2025 and 2030 -- but I’ll be happy to be proven wrong.

Driverless cars will usher in a revolution in fuel efficiency for a number of reasons, including: 1) computers are much better drivers than humans and will use less fuel; 2) automated car services will be able to substitute for regular car ownership for a significant number of car owners; 3) driverless cars can be actively driving for far more hours in the day through car-share services like Uber and Lyft, further increasing the efficiency of our entire transportation system.

A recent study found that driverless cars and car-sharing services could save up to 90 percent of the fuel we currently consume, mainly through “right-sizing” the vehicle required for each task. If a person needs a quick ride five miles from town, a single-person self-driving EV would pick that passenger up and take him or her to the desired destination. If a family needs an electric SUV for a beach excursion, that would be provided. By right-sizing each vehicle for each trip, the needless transportation of tons of steel would be dramatically reduced from today’s highly wasteful default driving situation.

Another recent study, from McKinsey & Company, found the potential for even more profoundly positive ramifications stemming from self-driving cars: up to a 90 percent reduction in driving fatalities, due to the fact that computers are so much better drivers than error- and distraction-prone humans.

In the U.S. alone, this would equate to about 30,000 lives saved each year and up to $190 billion in annual savings from healthcare costs associated with accidents. This translates to 10 million lives saved globally each decade. Even more importantly, self-driving cars will significantly reduce the need for parking.

The future is indeed bright.

***

Tam Hunt is a lawyer and owner of Community Renewable Solutions LLC, a renewable energy project development and policy advocacy firm based in Santa Barbara, California and Hilo, Hawaii, co-founder of Solar Trains LLC, and author of the new book, Solar: Why Our Energy Future Is So Bright.

41

41

15

15

9

9