We all know that the 2009 American Recovery and Reinvestment Act (ARRA) has handed out billions of dollars to smart grid projects around the country, with smart meters, or advanced metering infrastructure (AMI) deployments, getting the biggest share. That's been a boon to AMI vendors like Itron, Silver Spring Networks, Elster, Trilliant, Sensus and Landis+Gyr, and has helped put about 12.3 million digital, two-way communicating electricity meters into the field, out of a nationwide total of some 35 million and counting.

But AMI is about more than simple, standalone automated billing devices attached to every home. To achieve full value, smart meters will have to integrate to lots of utility back-office software systems, grid operations control centers, customer service and workforce management platforms, and many other parts of the utility enterprise. That's a goal of many stimulus-backed AMI deployments -- but how far along are they in the integration task?

To shed light on that subject, we turn to two sets of data out this week. The first comes from research firm Zpryme, which reported Tuesday that, out of $8 billion in Department of Energy grants and matching expenditures across 99 stimulus-backed projects, about $5.1 billion has been spent as of mid-May.

That’s up from about $3 billion as of March 2012, and accounts for just less than two-thirds of a one-time capital infusion that has boosted the smart grid industry’s fortunes over the past few years. And, of the total spent so far, about 63 percent of it, or $3.2 billion, has gone to smart meters. We've been covering the effects of ARRA funding on the U.S. AMI market, as well as the slowdown that has come in its wake.

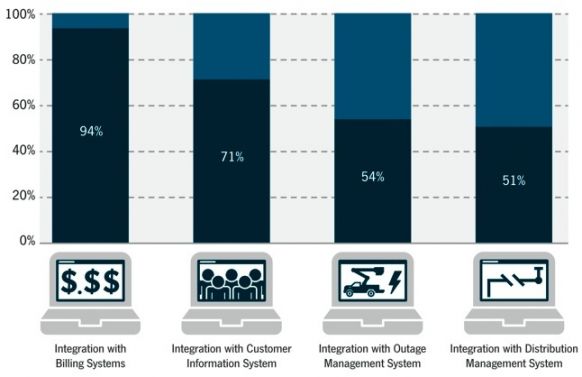

The second set of data comes from GTM Research’s upcoming report, AMI Analytics: Vendors, Applications and Markets, and takes a look at the core question of AMI integration. According to these findings, utilities still have a ways to go in realizing the potential of their smart meters to do more than just collect bills.

So far, utilities are pretty good at that core function, with 94 percent saying they’ve integrated AMI into their billing systems. (The remaining 6 percent could be early-stage projects that haven’t gone live yet or have been delayed, since without billing, meters are of little use.)

But only 71 percent of stimulus-backed AMI projects have integrated with utility customer information systems (CIS), which would seem like the next logical place to extend smart meter functionality. Seemingly simple tasks, like giving utility phone center operators the data to tell customers whether their smart meters are on or off during a power outage, require this kind of integration to be successful.

Even fewer utilities (54 percent) have integrated AMI with their outage management systems (OMS), which again is a place where knowing whether the meter is on or off could be very useful. And only 51 percent have integrated their AMI with their distribution management systems (DMS) to do things like feed data into volt/VAR optimization schemes, or alert grid operators of grid instability in real time, to name two examples.

It’s important to remember that these figures should climb over time, as more and more utilities move further along in their long-range AMI plans. Oracle surveyed 150 U.S. utility executives in 2012, and found that a good number have begun collecting data for AMI integrations they haven’t carried out yet. For instance, while 78 percent of respondents said their utilities were collecting outage detection data from their smart meters, only 59 percent were actually using it for business processes and decision-making.

Similar gaps were revealed in voltage data, with 73 percent collecting it vs. 57 percent using it; tamper detection data (63 percent collecting it vs. 47 percent using it); and diagnostic data (56 percent collecting it vs. 33 percent using it). Of course, discrepancies like these make some sense, considering that many of these deployments are trying to combine different utility technologies for the first time.

Perhaps the better question is whether all this data collection will support spending more money on full-scale AMI integration. While the urgency of getting smart meters and billing systems working smoothly is obvious, there may be fewer business imperatives pushing the integration of smart meters into all the other platforms that make up the utility enterprise.

Finding these imperatives will be critical for AMI vendors and the smart grid industry in this post-stimulus environment. DOE’s proposed 2014 fiscal year budget calls for only about $450 million in smart grid investment, much of it on the R&D side. As GTM Research senior smart grid analyst David Groarke pointed out in an article this month, this may not be enough to maintain domestic growth in smart meters, both in terms of utilities installing them and vendors supplying them.

41

41

15

15

9

9