The United States continues to slumber while a catastrophe lies in wait. Increasing numbers of analysts and policymakers are warning of another super price spike for oil and the likelihood of “peak oil” more generally.

Peak oil is the point at which global oil production reaches a maximum and then declines. The speed of the decline is a key unknown and if it is relatively fast, the results could be truly dire for economies around the world.

We saw prices as high as $147 a barrel in mid-2008 (the dominant factor for gasoline prices well over $4 a gallon), which played a strong role, perhaps the dominant role, in the global Great Recession -- as high oil prices have in most recessions over the last fifty years. Once the recession hit, oil demand dropped and prices plummeted as low as $33 a barrel.

Prices steadily recovered since their low in early 2009 and are back to dangerous levels in early 2011 (about $90 a barrel). We can expect far higher prices as the global recovery continues. An increasing number of analysts are projecting prices as high or higher than the 2008 peak in the next couple of years.

More importantly, global net exports of oil continue to drop as major oil exporters increase their own consumption at the same time as their production is stagnant or falling. As a major oil-importing nation (about two-thirds of our oil is imported, by far the largest import dependency in the world), net oil exports are far more important to the U.S. than total oil production. Even if global oil production increases in the coming years, if there is less available for oil-thirsty nations like ours, the situation will be far worse than total oil production figures would otherwise suggest (more on this below).

It is time for public discussion of this issue to reach the same prominence as climate change. Indeed, many solutions to these “twin crises” are the same because reducing petroleum dependence will ameliorate peak oil and climate change.

This article is an update on the peak oil situation at the beginning of 2011 and a follow-up to my many previous pieces on peak oil (one with Nobel Prize winner Walter Kohn). First, some facts.

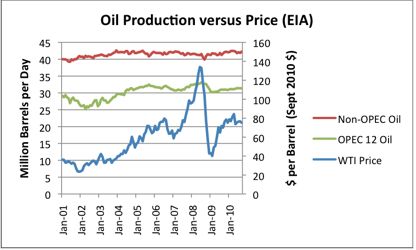

Global oil production has plateaued since 2004, despite the fact that oil prices have risen dramatically. Figure 1 shows this history, demonstrating that oil production has not been very responsive to market forces, suggesting strongly that we are at a global peak.

Figure 1. Global oil production and oil price 2004-2010. (Source: EIA, chart courtesy of www.TheOilDrum.com).

Bloomberg reported a summary of oil price forecasts for 2011, selecting for their summary those forecasters who have the most accurate track records. The dominant view was that average oil prices will rise almost as high in 2011 as seen in 2008 -- to $87 a barrel for the year as a whole (the average price for 2008 was $99). It’s likely, however, that the actual average 2011 price will be significantly higher because we are already over this price (at about $90 a barrel in early January) and the large majority of economic forecasts project a robust global recovery this year, with attendant increases in oil demand.

More anecdotally, but with perhaps more impact because of its source, Shell’s recent ex-president John Hofmeister predicts $5 gas by 2012 due to the global economic recovery and very tight supply.

A number of comprehensive reviews of the global oil supply situation have appeared in the last year.

· Lloyds and Chatham House: “We are heading towards a global oil supply crunch and price spike.” “A supply crunch appears likely around 2013… given recent price experience, a spike in excess of $200 per barrel is not infeasible.”

· The U.S. Department of Defense issued a stark warning in its 2010 Joint Operating Environment (JOE) report, including discussion of “peak oil”: "By 2012, surplus oil production capacity could entirely disappear, and as early as 2015, the shortfall in output could reach nearly 10 million barrels per day.”

· Similarly, the German military is taking peak oil very seriously, made clear by a report leaked to Der Spiegel in 2010: “[The report] warns of shifts in the global balance of power, of the formation of new relationships based on interdependency, of a decline in importance of the western industrial nations, of the ‘total collapse of the markets’ and of serious political and economic crises.”

· The same article reports on secret British government planning for peak oil: “The leak has parallels with recent reports from the U.K. Only last week the Guardian newspaper reported that the British Department of Energy and Climate Change (DECC) is keeping documents secret which show the U.K. government is far more concerned about an impending supply crisis than it cares to admit. According to the Guardian, the DECC, the Bank of England and the British Ministry of Defence are working alongside industry representatives to develop a crisis plan to deal with possible shortfalls in energy supply.”

· The U.K.’s Industry Task Force on Peak Oil and Energy Security (a non-governmental group) issued its second major report on peak oil in late 2010, concluding: “[W]e face a situation during the [next few years] where fuel price unrest could lead to shortages in consumer products and the U.K.’s energy security will be significantly compromised. This has the potential to hit U.K. business and commerce as well as the most disadvantaged in society with yet another crisis.”

In August 2009, the International Energy Agency (IEA), the official energy watchdog for the Western world, was even more strident in its warnings. The U.K.’s Independent newspaper reported:

The world is heading for a catastrophic energy crunch that could cripple a global economic recovery, because most of the major oil fields in the world have passed their peak production, a leading energy economist has warned.

Higher oil prices brought on by a rapid increase in demand and a stagnation, or even decline, in supply could blow any recovery off course, said Dr. Fatih Birol, the chief economist at the respected International Energy Agency in Paris, which is charged with the task of assessing future energy supplies by OECD countries.

Later in 2009, two IEA whistleblowers went public and claimed that the situation was even worse than the IEA was stating publicly. The U.K.’s Guardian newspaper reported in November of 2009: “A … senior IEA source, who has now left but was … unwilling to give his name, said a key rule at the organization was that it was ‘imperative not to anger the Americans,’ but the fact was that there was not as much oil in the world as has been admitted. ‘We have [already] entered the ‘peak oil’ zone. I think that the situation is really bad,’ he added.”

IEA has changed its public tune yet again, however. IEA’s 2010 World Energy Outlook (WEO), a major forecast released each year, apparently ignored the IEA’s own previous analysis by reverting to its previous policy of simply assuming -- literally -- that projected petroleum demand will be met with the needed supply. IEA states in WEO 2010: “Energy prices ensure that projected supply and demand are in balance throughout the Outlook period in each scenario.” In other words, IEA simply assumes that supply will meet demand due to market forces. This is obviously true at a very basic level: supply will always match demand if we define demand as that which is actually consumed. But if we define demand instead as the desired oil consumption, all else being equal, we reach a very different conclusion -- far more in line with the U.S. JOE report that projects a possible 10 million barrel per day shortfall by 2015.

WEO 2010 does, however, include some discussion of peak oil and it projects that the 2006 peak in global conventional oil production will never be exceeded (p. 8 of the Exec. Summary). That is, IEA has officially concluded that 2006 was the annual peak for conventional oil production. We are, accordingly, past the point of peak oil if we define this term to include only conventional oil.

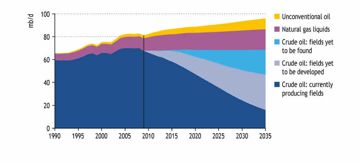

Even based on official IEA projections (which are likely far too rosy considering the whistleblower claims), we have a major problem facing us, made clear by the below chart. The key point from this chart is that IEA thinks we’ve already passed the peak for global conventional oil production, as just mentioned. As a consequence, a huge amount of new oil must be found to replace declining conventional oil production -- a deficit of about 75 million barrels per day by 2035. This is equivalent to nine new Saudi Arabias coming online by 2035 (Saudi Arabia currently produces about 8 million barrels per day).

IEA projects (Figure 2) that this new oil will come from a combination of new conventional oil production, from known fields yet to be developed and fields not even found yet; from natural gas liquids; and from unconventional oil like tar sands and oil shale.

Figure 2. IEA projections for oil supply through 2035 (Source: IEA WEO 2010.)

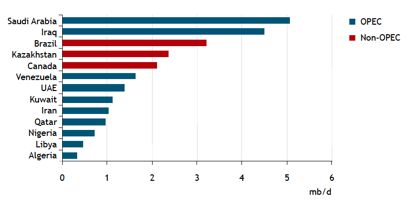

For those who worry about national security and energy dependence, the report offers an even more worrying conclusion: the large majority of new oil will come from OPEC nations, with only Brazil, Canada and Kazakhstan as non-OPEC nations projected to have significant new production (Figure 3).

Figure 3. Sources of new oil by 2035 (Source: IEA WEO 2010).

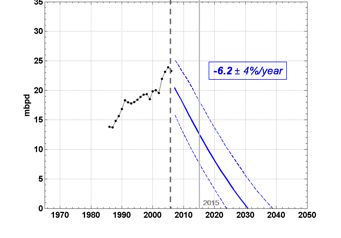

We must keep in mind, however, that these new production figures don’t take into account the growing petroleum demand in these producing nations. The key issue, from a U.S. national security and energy dependence perspective, is not oil production itself but “net oil exports.” The public version of the 2010 WEO does not discuss net oil exports, but private analysts Jeffrey Brown and Samuel Foucher have produced forecasts of net oil exports, concluding that the top five oil exporters will have literally zero oil for export by 2030. Even if, for some reason, their model is substantially off the mark (it’s not been peer-reviewed, to my knowledge), we must consider the net export issue in our analysis because any analysis that ignores rapidly growing consumption in oil-producing nations will be highly inaccurate.

Figure 4. Brown and Foucher’s 2008 projections for top five oil exporting nations’ net oil exports by 2030, in millions of barrels per day (mbpd).

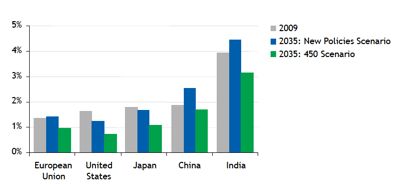

It’s not all bad, however. A more encouraging forecast from the IEA report can be found in their cost savings projections. They conclude that the “new policies scenario” (what used to be called the “reference scenario,” which codifies existing policies) and the 450 parts per million of carbon dioxide equivalent scenario (which codifies new policies required to prevent atmospheric emissions from reaching this level) result in very substantial net cost savings on a global basis and, in particular, for oil importing nations. This is the case because fossil fuel demand is dramatically reduced in these scenarios. This reduction in demand lowers both average prices for fossil fuels and the amount of fossil fuel that needs to be purchased.

Figure 5. Oil-import bills as share of gross domestic product in selected countries (Source: IEA WEO 2010).

It is time to get very serious about managing a reduction in petroleum demand in the U.S. and around the world. I write “managing,” because it is my view that this reduction in demand will happen whether we want it to or not due to declining oil supplies. The question, then, is how we best manage this decline. A high quality analysis of the possible scenarios for an oil-constrained world, by Oxford University professor Jörg Friedrichs, appeared in 2010. Friedrichs examines three possible trajectories: “Predatory militarism,” “totalitarian retrenchment,” and “socioeconomic adaptation.”

At least two rigorous policy solutions have been offered in recent years. The Rocky Mountain Institute completed Winning the Oil Endgame in 2007, suggesting a suite of policy and technology solutions that can get the U.S. off oil, “led by business for profit.” Richard Heinberg offered his own book-length solution, The Oil Depletion Protocol, in 2008, suggesting how the U.S. and other nations could manage declining oil supplies by achieving a three percent per year reduction in demand through various policies.

As we continue a global economic recovery in 2011, higher oil prices are inevitable, super price spikes are a strong possibility, and even shortages are not out of the question. We must ask ourselves: should we manage the decline in a way that avoids economic catastrophe or do we continue our generally laissez faire attitude toward this major problem?

***

Tam Hunt is president of Community Renewable Solutions, LLC, a renewable energy consulting and project development company. He is also a Lecturer in climate change law and policy at UC Santa Barbara’s Bren School of Environmental Science & Management. His blog, Thought, Spirit, Politik, is at www.tamhunt.blogspot.com.

41

41

15

15

9

9