[pagebreak: 1]

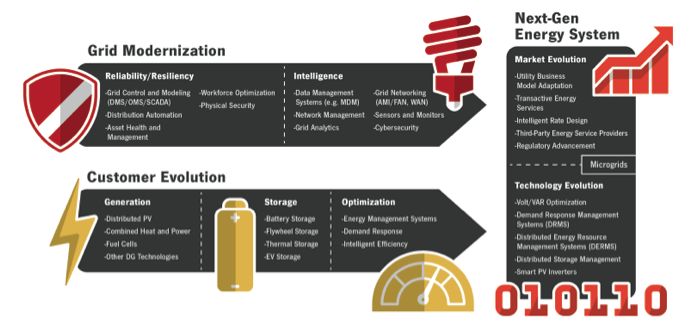

For nearly a century, electric utilities in the U.S. focused on delivering safe, reliable and affordable power. As power has become increasingly critical to every aspect of our lives, however, the business of making, delivering and consuming it is rapidly changing.

Today, that business is being turned on its head: a carmaker could also be a utility threat; an average homeowner may be able to cut ties with the larger electrical grid; a kilowatt not used is as valuable as a kilowatt produced; and reliability is increasingly being replaced by resiliency in the face of extreme weather events and potential security threats. Overall, the fossil-powered, centralized electrical system is being challenged by changes at the edge of the grid that will redefine the power industry in the short term.

Since launching the Grid Edge Executive Council in the fall of 2013, and leading up to the inaugural Grid Edge Live conference, Greentech Media felt it was important to identify companies that embody the tenets of grid edge industry transformation that are underway.

This led us to conceive of the Grid Edge 20, a selection of twenty technology vendors serving the electric power market that we believe have the potential to shape the market going forward with innovative products, sound market strategies and forward-looking vision.

Grid Edge 20 is a mix of companies that have significant existing market traction and are well positioned for the imminent technology and industry transformation, as well as potentially disruptive newcomers that we see as having the ability to impact the industry going forward. The companies are listed in alphabetical order.

Join us in San Diego on June 24-25 to hear from many of the companies below at the first Grid Edge Live conference.

ABB/Ventyx. Since buying Ventyx for more than $1 billion in 2010, industrial titan ABB has been a leader in integrating operational technologies and information technologies. Last year, ABB/Ventyx launched its Asset Health Center, with American Electric Power as its first customer.

Many large vendors claim to offer fully integrated asset health monitoring services, but ABB is one of the only firms to have its product operating in the market.

But asset health is just the beginning. Ventyx and ABB are also helping utilities with cutting-edge load forecasting and planning, network optimization and distribution operations solutions tailored for renewable management. ABB also picked up Power-One for $1 billion last year. “Ventyx took a leading position in the market last year, tackling the biggest IT challenges in the global utility industry,” said Ben Kellison, senior grid analyst with GTM Research.

The grid giant is certainly not the only big player with integrated IT solutions for OT problems, but it is certainly one of the furthest along in market development.

Aquion. Lithium-ion batteries are good for providing only a few hours of energy -- tapping and topping off their electrochemical capacity too often or too deeply wears them out faster than it’s worth.

Multi-hour energy storage, whether of the advanced lead-acid, vanadium redox flow, or air-water based hybrid varieties, could break that barrier, if longevity at the right price points can be proven.

Pittsburgh, Pa.-based Aquion Energy’s take on this long-lasting electrochemical alchemy involves an activated carbon anode, a sodium and magnesium-oxide cathode, and a water-based (i.e., aqueous) electrolyte.

Aquion has raised $100 million, which isn’t unusual for a battery startup at this stage of its development. But unlike many of its next-generation competitors, it has real-world deployments in off-grid, microgrid and substation-integrated configurations to test its propositions. Partners like Siemens don’t hurt either.

AutoGrid. Gone are the days of one-way demand response where utilities sent out signals, crossed their fingers, and hoped load was shed. From the Far East to Texas, big data analytics firm AutoGrid is chalking up partnerships with utilities that are looking for sophisticated demand-side optimization using high-performance computing.

The Palo Alto-based startup offers real-time visibility using data coming from the grid and beyond the meter. In the U.S., most demand response markets and utility programs don’t currently require real-time validation. But as demand-side management becomes a more integrated part of utility operations across the globe, big data applications will become increasingly important.

AutoGrid’s approach has earned the company partnerships with Schneider Electric, Silver Spring Networks, Japan’s NTT and strategic investment from E.ON, which led AutoGrid's $13 million series C earlier this year.

C3 Energy. Can the right big data architecture solve any number of the world’s energy-carbon-resource crises?

That’s the goal that Tom Siebel’s big-data-for-the-smart-grid startup C3 Energy has set for itself. From its original carbon-management concept, Siebel and his team have pivoted to energy efficiency, and then into grid data analytics, with the aplomb and confidence that befits an all-star board of directors and more than $105 million of VC funding.

Now the Redwood City, Calif.-based startup has a big, deep and wide data analytics project with Baltimore Gas & Electric to start converting its promises of billions of dollars in analytics cost savings and revenue potential into real-world results.

BGE owner Exelon is testing out C3’s platform in Chicago and Pennsylvania as well -- proof, said Siebel, of the value of building C3’s enterprise data analytics platform from the ground up.

Cisco. “Network the grid like we’ve networked the internet” has been Cisco’s (NASDAQ: CSCO) rallying cry since it jumped into the smart grid field in 2009.

Five years later, Cisco’s unified IPv6 network concept has been rolled out to hundreds of utilities in one way or another -- and its multi-million-customer smart meter/distribution automation project with BC Hydro is ready to move on to theft detection, outage restoration and other next-generation grid applications.

Cisco’s partnerships with dozens of other key grid vendors are also driving an important concept into the discussion around grid edge systems. That’s the idea of interoperability and intelligence, distributed into the network -- from transformer monitors and cap bank controllers to home energy and utility worker smartphones and tablets.

Cisco’s IOx platform, which opens up its grid routers to Linux-based applications from partners like Alstom, Itron and OSIsoft, is one example of how this new distributed intelligence concept is being applied today.

Enbala Power Networks. Enbala’s first big contract was with PJM, where it provided frequency regulation services by aggregating quick-respond load. The Toronto-based startup can take advantage of the higher payments for fast-responding resources that were required by FERC Order 755, but it is also helping vertically integrated utilities squeeze improved efficiency from their assets.

Whether it’s more cost-effective renewable balancing for utilities or just cutting generation costs by using assets more efficiently, Enbala’s demand-side management platform aims to do much more than just aggregate resources for frequency regulation.

Industrial and utility customers are seeing paybacks that are usually unheard of in the realm of energy efficiency: less than one year.

Enphase. Microinverters made up more than 40 percent of the U.S. residential solar market in 2013, and Enphase accounted for nearly that entire share. The company shipped more than 5 million microinverters from 2008 to 2013.

Microinverters allow solar installers to design solar arrays more easily and cheaply. Enphase’s market share is based not just on its technology, but also on its relationship with its customers. Any product that streamlines the sale and installation of solar PV is just one more mover at the edge of the grid that challenges the status quo.

“As the pioneer of solar microinverters and, to date, the only competitor of scale, Enphase's every step signals the potential growth -- or death -- of the microinverter insurgence,” said MJ Shiao, director of solar research for GTM Research.

FirstFuel. The software business for energy efficiency has boomed in recent years, but the more nimble players are already looking far beyond low-touch audits.

FirstFuel is best known for its virtual auditing tool, but earlier this year, it evolved into what it is calling a "demand-side SaaS [software-as-a-service] analytics company."

The Boston-based startup has moved from identifying efficiency opportunities, which scores of software suites can do, to helping projects move forward and meet measure and verification guidelines. “Analytics can’t change a light bulb,” said FirstFuel’s founder Swapnil Shah.

As utilities look beyond the low-hanging fruit they’ve already plucked for their energy efficiency platforms, FirstFuel thinks it can be the go-to M&V platform for those programs and for the likes of the GSA and efficiency firms. FirstFuel isn’t just focusing on the U.S., either; European utility giant E.ON led its series B venture round of $8.5 million.

Gridco Systems. Electricity is a harsh mistress, but it can be tamed -- either with the mechanical contraptions of Thomas Edison’s grid, or with power electronics that wrangle live grid voltage and current, as semiconductors might wrangle the flow of electrons that carry data.

The spread of power electronics to “digitally manage the electric waveform,” as GTM Analyst Ben Kellison puts it, is now spreading into the last mile of the grid, via companies like Gridco Systems.

Woburn, Mass.-based Gridco has raised about $30 million to design, build and deploy its own version of the grid power router: the In-Line Power Regulator, a series-connected voltage and current regulator, complete with a computer brain and communications network to connect back to the startup’s “emPower” distribution grid platform.

A number of top tier utilities are testing out the platform's ability to control voltages along individual distribution lines with devices that use no moving parts, need no regular maintenance, and keep running for decades, according to company claims.

Landis+Gyr. Switzerland-based Landis+Gyr was already a top-ranked global smart meter leader when Japanese giant Toshiba bought it for $2.3 billion in 2012.

Landis+Gyr has since absorbed Ecologic Analytics, the second-biggest independent meter data management software provider in the U.S., and has started pulling together a number of grid-edge linkages in projects ranging from Texas to Bavaria to Tokyo.

Toshiba’s microEMS device, being tested in Japan and Los Alamos, N.M., ties smart meters, storage and solar inverters and SCADA-connected grid gear and sensors into something grid operators can use to monitor, or even manage, this motley collection of grid-edge disruptions.

The communications backbone of a 27-million-unit smart meter project with Tokyo Electric Power Co. is a must-study for understanding how Japan intends its grid to run on standards secure enough to take on the deep, societal adjustment in electricity use (and self-sufficiency) needed to address the country’s post-Fukushima energy crisis.

[pagebreak: 2]

Nest Labs. Nest began selling its learning thermostat in 2011, and less than three years later Google scooped it up for $3.2 billion. “The firm is not a home energy network company,” Greentech Media’s Eric Wesoff wrote in 2011. “Nest builds thermostats. Beautiful, smart and expensive thermostats.”

Many in the energy efficiency industry hailed the high-priced exit as a win for cleantech. But Google was buying some of the top industrial designers in the business and a platform to get into the connected home market, not an energy product. Even so, energy efficiency is one part of smart home, and Nest has brought visibility and excitement to the world of home energy management.

It’s unclear what Nest will do beyond thermostats and smoke detectors, but the company could open up homes in new ways that could be leveraged by everyone from Google to local utilities. Nest certainly changed the game on how home efficiency should look and feel.

Opower. For years, Opower has amassed countless utility clients by offering behavior-based efficiency measures with a mailed home energy report as its flagship offering.

Now, the company is on the verge of an IPO that is expected to raise about $100 million.

The Washington, D.C.-based startup still sees plenty of growth opportunity in providing incremental savings to utilities, but in the future it’s looking to leverage its enterprise-level analytics to help utilities with everything from demand response to integrating solar and EVs.

Opower already crunches 100 billion meter reads a year on more than 30 million utility customers, which makes it a natural choice for utilities that are moving deeper into customer segmentation and energy services.

Power Analytics. Imagine a software simulation of the power grid, and then imagine running it quickly and accurately enough to keep up with real-world grid fluctuations -- or even to predict what's going to happen next. That’s one way of describing what San Diego, Calif.-based Power Analytics has been doing for grid systems for the past two decades.

Formerly known as EDSA, Power Analytics has also helped select clients like the U.S. Navy and the Federal Aviation Administration design and implement complex power systems.

It’s now branching into interconnected regional microgrids and solar-energy-storage systems, with an eye on helping create physics-based models and underlying control systems for managing the most complex two-way, distributed challenges on the grid edge.

S&C Electric Company. Before resiliency emerged as the watchword for infrastructure investment, EPB Chattanooga was reporting on how much money it was saving with its 1,200 S&C IntelliRupter automated switches.

Since then, the utility has repeatedly been able to show avoided outages and faster restoration time -- something that many other utility companies have had trouble illustrating after investing in distribution automation technologies.

Not only is S&C a leader in providing distribution solutions for reducing outage time, it is also one of the go-to leaders in storage integration for utilities, whether community or grid-scale. In particular, S&C is investigating the 25- to 250-kilowatt-hour battery size that can live behind the meter or at the grid’s edge.

As a leader in storage integration, S&C is also a member of Duke Energy’s Coalition of the Willing, a group aiming to connect grid assets into a distributed, intelligent grid control system.

Silver Spring Networks. Metering alone is so 2010. That is why Silver Spring Networks is networking far more than smart meters these days.

In one of its latest projects with Hawaiian Electric Co., Silver Spring will provide the AMI network, but also customer-facing and distribution optimization services.

And it’s not just large smart grid contracts that could drive Silver Spring’s business in the future. It has also pushed into networking LED street lights and smart city network-as-a-service offerings. Silver Spring is also integrating solar inverters with its networks, something that will be increasingly important for smart metering networks.

In January, it also launched its SilverLink Sensor Network to integrate various nodes on the grid network, including those behind the meter, into a single distributed intelligence platform. This platform provides partners and utilities with access to a vast data resource without the costly integration and consultants that form the foundation of almost any big data project, said GTM's Ben Kellison. Utility partners haven’t been announced yet, but Silver Spring says several will launch this year.

SMA. The kingpin of the solar inverter market, Germany’s SMA is staking claim to leadership status in the advanced inverter market.

SMA has earned its smart inverter credentials in the German solar market, which has required advanced features for years. With California now creating its own smart inverter requirements in advance of national standards, SMA is looking to bring its European experience to U.S. markets. It’s also pushing its own line of microinverters in an attempt to wrest market share from U.S. microinverter market leader Enphase.

SolarCity. As the company that pioneered third-party financing and management of rooftop solar PV, SolarCity has helped drive solar penetration to new heights -- and engendered a whole new crop of competitors.

Now SolarCity is pushing into a new frontier, energy-storage-backed solar, where it’s taking on challenging economics and utility pushback against the potential market disruption that its battery-solar systems represent.

Its relationship with Tesla Motors, which could radically expand its lithium-ion battery production, makes SolarCity an important player to watch on this front. The company also has recent acquisitions in solar balance-of-systems and is working on creating securitized solar notes, all of which could help drive even faster, cheaper adoption of distributed solar.

Stem. Linking batteries with building owners’ hard-to-manage utility bill costs is Stem’s specialty. The Silicon Valley-based startup has connected more than 6 megawatts of lithium-ion batteries with its energy management platform, designed to prevent the spikes in momentary building energy usage that trigger demand charges.

Demand charges can add up to more than half a commercial building’s overall utility bills in markets like California and New York, and mitigating them is one of the key economic drivers for customer-sited energy storage.

Stem was also one of the first batteries-for-buildings players to create a storage-as-a-service fund, which allows customers to get low- or no-cost installations that they can pay back via reductions in their utility bills over time.

While demand charges are the foot in the door, solar integration may well be the next hot spot for Stem’s battery-to-building energy management systems to tackle.

Tesla. As various state lawmakers try to lure Tesla to their turf to build its $5 billion Giga battery factory, the role of Elon Musk’s vehicle company has already proved it goes far beyond the road.

Tesla’s roadster and Model S are objects of beauty and power that have received acclaim not only from deep-pocketed EV enthusiasts, but also from the auto world at large. As Musk looks to drive down the cost of batteries enough to put an EV in every garage, he may disrupt far more than just the auto industry.

Whether Tesla is competing with incumbent automakers or utilities, “most of its current and future competitors have considerably less vision, less imagination, a lot more baggage, and less passion,” said Chet Lyons, founder of Energy Strategies Group.

Varentec. Fueled by venture capital investment and grants from the Department of Energy’s ARPA-E program, Varentec was the first of a growing number of digital power router companies to deliver product to utilities, in the form of its ENGO-V volt/VAR controller and underlying software management platform.

The ENGO-V platform is now being piloted by Duke Energy, Southern Co. and a number of rural electric cooperatives, with an eye on managing volt/VAR optimization and voltage disruptions that can be caused by the increasing amounts of distributed solar PV along distribution feeder lines.

In the meantime, Varentec’s ARPA-E work on dynamic power flow control technology could help create new architectures for managing distribution grids.

There are a few more companies that have either the market traction or the disruptive approach at the grid edge that makes them worth watching as well. Here are the honorable mentions in alphabetical order:

41

41

15

15

9

9