SunPower kept its spot as the top commercial solar installer in the United States last year, but saw SolarCity increase its own share to nip at its lead. It's a rivalry worthy of a lawsuit over allegedly stolen customer data.

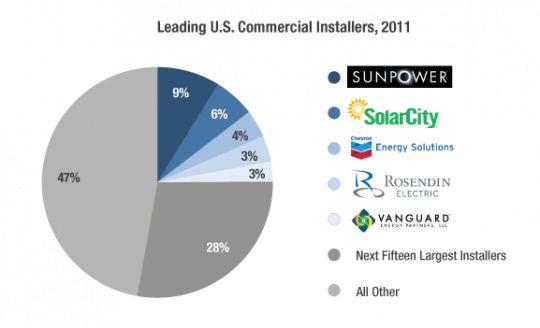

Over the course of 2010 and 2011, more than 1.1 gigawatts of commercial solar was installed in the U.S. Nearly 800 megawatts of that capacity came on-line in 2011, according to GTM Research. At the end of 2010, SunPower was far and away the largest commercial installer on the block, with an estimated 10.7 percent of national market share.

One year later, SunPower's share has slipped to 9 percent, while Solar City's has increased to 6 percent.

Source: GTM Research

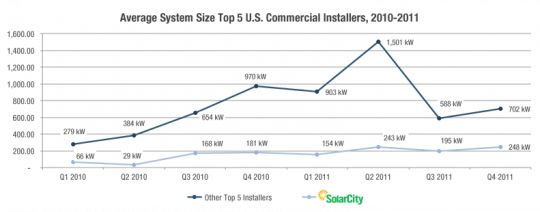

SunPower had a massive fourth quarter, installing nearly 20 megawatts of commercial projects in Arizona, California and New Jersey. This is nearly as much as the company installed in those states in all of 2010. Prominent in both the utility and commercial market segments, SunPower sticks to its core competency, which is installing large systems. In 2011, the average system size installed by the company was nearly 1.4 megawatts. In California, where the maximum system size allowed under the CSI program is 1 megawatt, SunPower’s average installation was 965 kilowatts. Go big or go home seems to be the commercial development team’s motto.

While SunPower focuses on larger systems, SolarCity has been quietly building its commercial business by focusing on smaller jobs. In California in 2010, SolarCity barely cracked the top-10 commercial developers with just 1.8 percent market share. Though the firm installed 44 systems under the CSI program, the average system size was just 36 kilowatts. Compare this to SPG Solar, the number one commercial installer in California in 2010, which averaged 650kW per installation. After honing its practices in the small-commercial market, and possibly with some help from strategic acquisitions, SolarCity has begun to push into the traditional commercial players’ arena. In Q4, SolarCity’s average commercial system size was approximately 250 kilowatts, a significant step up from the previous year.

Source: GTM Research

Rounding out the top-five commercial installers are Chevron Energy Solutions, Rosendin Electric and Vanguard Energy Partners. Chevron is well known in the U.S. solar industry, but the latter two may leave some readers, and even solar-industry veterans, scratching their heads. Rosendin has been involved in solar for some time, but generally as an EPC partner. In the last year, however, the firm has emerged as a legitimate developer both in the U.S. and Ontario. According to the company’s website, Rosendin has 100 megawatts in construction and more than 500 megawatts in development. Vanguard has existed as a pure-play developer for few years now, but it was not until 2011 that the company started to emerge a leader in the East Coast market. In Q4 alone, Vanguard installed 8.2 megawatts in New Jersey, second only to SunPower’s 11.1 megawatts' worth of projects. The company is also actively installing throughout New England and New York, including a project that will be the world’s highest elevated PV array on Deutsche Bank’s NYC headquarters.

One question many readers may have is, where are the traditional leaders SunEdison, Borrego, SPG, REC, and the like? They’re still in the top 20, but have either suffered from increased competition from new entrants like Rosendin or altered their business strategies. In the past year, many construction and large-electrical contracting firms, such as Swinerton Builders and Stellar Energy, have moved into commercial development. Most of these firms have previously acted as an EPC partner on large installations, but nothing more. By leveraging existing financial partnerships or substantial balance sheets, moving into project development was the next logical step to maximize revenue in the solar space and to help make up for a downturn in new construction.

As in the residential market, the commercial development space is seeing a fair bit of consolidation. Combined, the top-five firms held 25 percent of the market in 2011; the top 20 accounted for 53 percent. The latter figure is up from 45 percent in 2010. Moving forward, the top installers will only continue to grab more market share. With every passing quarter, project development practices are honed, helping to bring down soft costs. Investors, both traditional banking institutions and large corporations like Google, are becoming more comfortable with the well-known development firms, thus increasing their access to capital, even after the expiration of the 1603 Treasury Grant. Finally, proven success developing and installing projects allows these top firms to negotiate the best possible component prices from Tier-1 providers, which are aggressively pursuing supply agreements with top development firms.

***

GTM Research is now tracking top commercial and residential installers and module suppliers in the U.S. solar market. After collecting over 1.5 GW worth of project level data we have been able to produce the most comprehensive market share estimates available for the U.S. solar market. This product provides quarterly national market share estimates for installers and module suppliers, as well as state-by-state breakdowns to California, New Jersey, Arizona, Maryland, Massachusetts, Connecticut, New York, Ohio and New Mexico. Combined, the data from these states represents well over 60% of installed solar capacity in the U.S. GTM Research separately tracks state installatiion totals in the U.S. Solar Market Insight reports, which are published on conjunction with SEIA.

GTM Research also lists major customers of the top-10 module suppliers in the major state markets of California and New Jersey. This data represents more than 845 megawatts' worth of installations spanning both 2010 and 2011. For more information, please email our Research Sales Team.

41

41

15

15

9

9