GTM Research and SRECTrade today publish the SREC Market Monitor: Q3 2012 report; this quarterly report series is the industry's best source of strategic data and analysis on SREC market in the U.S. To learn more, click here.

Solar Renewable Energy Certificate (SREC) programs first appeared in New Jersey in 2005. Today, there are seven U.S. states with active, open SREC markets: Delaware, Maryland, Massachusetts, New Jersey, Ohio, Pennsylvania and Washington, D.C. Since then, these seven states have seen significant solar development activity. In early 2012, driven by its SREC program, New Jersey surpassed California as the largest retail solar market in the U.S.

No two markets are the same. Most SREC states have a solar carve-out within renewable portfolio standard (RPS) laws that requires that a percentage of electricity in the state be derived from solar. SRECs are purchased by utilities to meet these compliance obligations. In most states, the RPS adheres to a schedule set several years into the future that defines the demand for SRECs. In Massachusetts, the requirement each year is set by a formula designed to adapt to market conditions. It also has a price support mechanism in place that promotes spot market trading.

FIGURE: SREC Info Map, Q3 2012

Source: SREC Market Monitor: Q3 2012

Other states like Delaware and, to a lesser extent, New Jersey have moved toward long-term SREC procurement programs. These programs can reduce the cost of capital in solar by providing long-term guaranteed SREC revenues, which in turn can reduce the cost of solar to the ratepayers. Delaware has developed a statewide program that competitively sets long-term SREC contracts, while New Jersey has taken a similar approach with a portion of the market. Finally, a few states utilize SRECs to help utilities meet their requirements, but those programs are not covered in this report due to a lack of an open market mechanism.

Over the past few years, the expansion of SREC markets into new states across the eastern U.S. has subsided, mostly due to unfavorable legislative conditions. Despite this trend, many states that have already implemented SREC programs have found ways to provide continued support through legislative improvements. Combined with the significant growth driven by these programs, it is clear that the SREC model as a mechanism to promote solar growth has become a major part of solar finance in the United States and will continue to have a significant impact on development in the years to come.

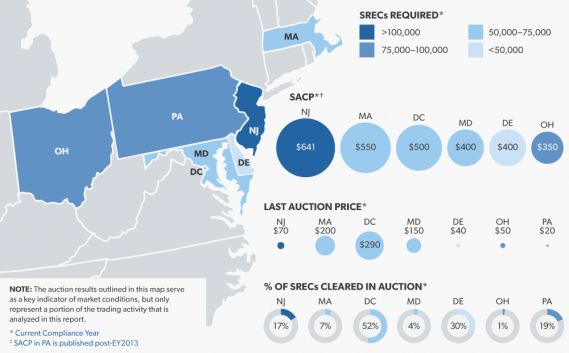

FIGURE: SREC Market Status Overview

Source: SREC Market Monitor: Q3 2012

New Jersey pricing continues to decline

- Following the passage of legislation in July, New Jersey SREC prices for the 2012 and 2013 vintage periods continued to decline, falling below $100 per SREC. The decline in price has been a result of substantial oversupply for both the 2012 and 2013 compliance periods. Forward contracts have declined in price as a result of the expectations that current oversupply and install rates will further impact 2014 and future periods.

Massachusetts 2012 oversupplied, 2013 requirements announced

- Massachusetts 2012 vintage SRECs continued to trade in the low $200s. Although traded volumes have been limited, buyers have not been actively bidding price up as there is plenty of time left in the compliance period until obligations have to be finalized in June 2013. At the end of August, the Department of Energy Resources (DOER) announced the 2013 SREC requirement. While the existing formula derived the number of SRECs needed in 2013, the DOER also announced its intention to make an adjustment to the equation that will increase the 2013 SREC target.

Maryland 2012 pricing slips as large projects come on-line

- The quarter started off steady with the 2012 vintage pricing at $200 per SREC. Constellation’s 16.1-megawatt project came on-line in August, causing a dip in pricing for the current year vintage, which recently traded at $150. Although the 2012 market will see oversupply, the long-term outlook is positive given the renewable portfolio standard (RPS) amendment passed in Q2 2012.

Delaware sees minimal activity as the market waits for next solicitation

- Minimal transaction activity took place for the DE2012 vintage. SRECTrade’s September auction saw some volume trade at $40 per SREC. Development has been minimal as market participants are waiting in anticipation of the next DE Sustainable Energy Utility solicitation program; it is currently expected in early 2013.

D.C. market continues to see undersupply

- The Washington, D.C. market continues to see undersupply in the current compliance period. Pricing remains around $300 with the expectation that there may be an increase as obligations are finalized towards the end of 2012 and beginning of 2013. Project development continues at a slow rate given the geographic constraints of the District.

Pennsylvania sees no light at the end of the tunnel

- SRECs continue to trade in the $20s, with older vintages trading lower. There has been no movement from the legislature on the possibility of an amendment to the state’s Solar RPS goals and installation rates have slowed significantly. System owners should expect low SREC values for the next few years.

Ohio sees little demand for both sited and adjacent markets

-

Both the over-the-counter market and the SRECTrade auction have seen little demand for the 2012 vintage. A lack of demand has put downward pressure on pricing throughout the quarter. Given oversupply in the current vintage and the expectation that some of the state’s largest natural buyers have filled their SREC needs, it is likely the market continues to see little activity for the rest of the year. FirstEnergy issued a request for proposal (RFP) for 7,500 OH-eligible SRECs at the end of the quarter.

Want to hear more on SREC markets in the U.S.? Get GTM Research and SRECTrade's latest research at www.greentechmedia.com/research/srec-market-monitor.

41

41

15

15

9

9