Today, SEIA® and GTM Research released the third quarter version of U.S. Solar Market Insight™, our quarterly deep-dive into the U.S. solar market. The executive summary can be downloaded here. A few highlights from the PV section (state-level detail contained in the full report):

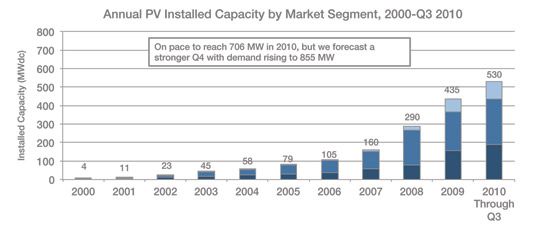

As of the end of the third quarter, the U.S. had already achieved a record year for PV installations. 188 MW were installed in the third quarter, resulting in a total of 530 MW for the year to date. Already, this represents 22% growth over the 435 MW installed in 2009, and the fourth quarter will only add to this total. At a broad level, demand remains driven by the Section 1603 Treasury Cash Grant program, state-level incentives, and improved project economics following a 2009 module price crash amidst the global financial crisis.

If the installation rate through the third quarter were annualized, the U.S. would install a total of 706 MW in 2010, up 62% over 2009. Early fourth-quarter data suggests, however, that there will be a late-year surge in installations resulting in total 2010 demand of 855 MW, well above the current pace.

State-Level Trends

Installations in the U.S. remain relatively concentrated in a few key markets. The top five state markets in Q3 were California, New Jersey, Florida, Arizona, and Colorado. Together, these states represented 74% of total national demand.

Q3 2010 PV Installations by Market Segment by State

_542_407_80.jpg)

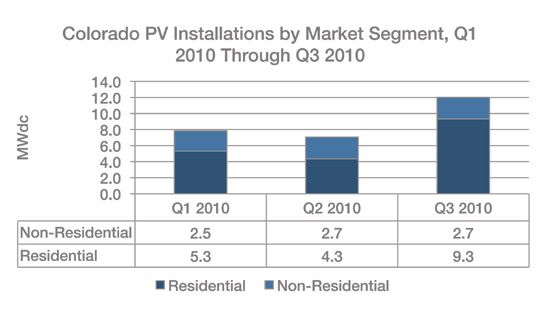

State Focus – Colorado

Residential installations in Colorado doubled in Q3 to 9.3 MW. This is due largely to the Governor’s Energy Office, which offers ARRA-funded rebates of up to $1.50/W for non-Xcel Energy and non-Black Hills Energy customers that previously had no available rebates. This program, which began in April 2010, is still running, and will continue until the end of 2011 (or until ARRA funding runs dry). We anticipate continued residential market strength in Colorado in the meantime, followed by a likely drop after the program expires.

Market Segmentation

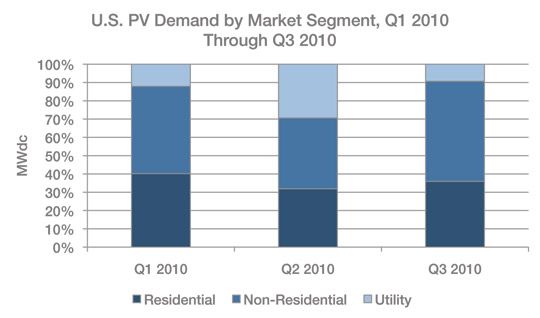

Total installations fell slightly in the third quarter of 2010 from 192 MW to 188 MW. However, this is not indicative of a decline in overall market strength. The figure below displays demand trends by market segment in the first three quarters of 2010. Clearly, each market segment (residential, non-residential, and utility) has experienced different growth patterns throughout the year.

· Utility installations fell substantially in the third quarter. Only one large project was connected to the grid during that period. However, utility installations will undoubtedly recover in the fourth quarter. Over 75 MW of utility PV have already been connected in Q4 and more is expected by year's end.

· Non-Residential installations (which includes commercial, public sector, non-profit, and school district) were the main growth driver in the third quarter, growing 38% quarter-over-quarter thanks largely to an improving financing environment and incentive step-downs in California. Extension of the Treasury Cash Grant will be crucial in enabling continued growth.

· Residential installations have seen the most stability of any market segment in 2010, growing slightly each quarter. The residential market is still experiencing the benefits of funding pockets provided by the American Recovery and Reinvestment Act (ARRA), and the 2008 removal of the cap on the Federal Residential Investment Tax Credit (ITC) remains the primary enabler of residential demand.

Other Key PV Findings:

· Oversupply of SRECs may cause a market crash in Pennsylvania in 2011

· Residential third-party ownership continues to gain share in California, rising above 25% of installations in Q3

· Average installed system prices have declined 8.5% over the course of 2010

· U.S. PV module production grew 5% in Q3, while inverter production more than doubled

· Component pricing remains relatively stable across the value chain in Q3, but expect a resumed decline in 2011

Find more details at www.gtmresearch.com/solarinsight

41

41

15

15

9

9