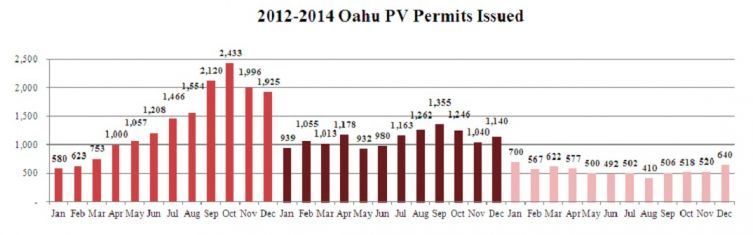

After going up precipitous inclines and hurtling down scary drop-offs, a rollercoaster ride typically ends as it comes to a flat part of the track and friction and braking take over. Oahu’s photovoltaic industry experienced the peak of the ride in October 2012, as far as the number of solar electric system permits issued by the City and County of Honolulu (C&C), with a steep drop-off coming in 2013 and some minor hills making an appearance through the remainder of the year. In 2014, the industry has definitely hit the flat part of the ride, with very few bumps in the fall. The last four or five months of the year is typically when PV businesses rack up sales to be able to make it through the leaner first months of the new year. If there’s a significant drop-off from the already modest permit numbers from this past quarter, there won’t be much in terms of accumulated sales and cash reserves to fall back on.

In 2012, the C&C processed and approved 16,715 PV permits. In 2013, 13,303 permits were issued, a decrease of 20 percent. In 2014, 6,554 solar electric permits were issued, a decline of 50 percent over 2013 and a drop of 60 percent from 2012.

Even more painful was the decrease in the total stated value of these projects. In 2013, the island’s PV industry obtained permits showing a total value of $453,652,576. Last year that figure was $200,720,113, or a drop of 55 percent.

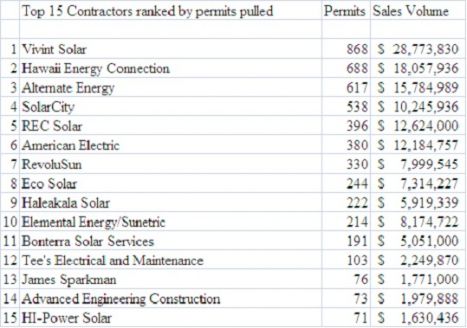

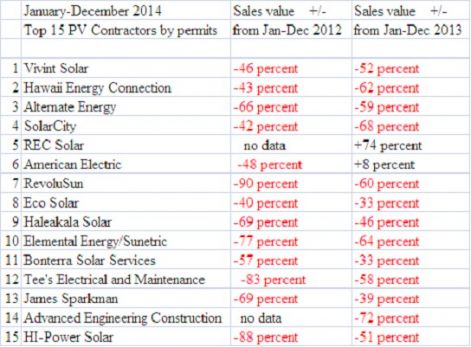

For some companies in the top fifteen, the decrease in business volume was even more dramatic, first from 2012 to 2013 and then again from 2013 to 2014. Only two companies, REC Solar and American Electric, were able to buck the trend, with both of them relying very heavily on third-party financing to close sales.

The ride ahead

What can be expected in 2015 for a local rooftop PV industry that has tallied up more than a billion dollars of economic activity in the past several years? Six factors will heavily influence whether the train continues down a track of steady, and possibly terminal, decline or starts again in an upward direction.

- Consumer demand

- Grid penetration challengers

- Net energy metering

- Tax credits

- Energy storage

- Oil prices and liquefied natural gas

Consumer demand

As has been widely reported, there are more households in the state on a percentage basis that have PV systems -- as well as solar thermal systems -- than anywhere else in the nation, by far. Approximately one in ten homes in Hawaii enjoys the benefits of producing some or even all of their own power, which has led some commentators to note that that leaves 90 percent of homes in need of solar electric systems. However, aspiring to achieve 100 percent solar adoption is not realistic. So how many more homes and businesses are likely to go PV that haven’t already done so? The case can be made that the low-hanging fruit has already been picked, and that the homes and businesses that were inclined to go solar have already done so. It’s a given that some consumers will never go solar because they just don’t care enough to do so, despite the zero-down, nothing out of pocket, and other creative public and private financing options available. So what can be expected in the coming year? A sustainable increase in consumer demand does not seem to be in the cards in the near term if 2014 serves as any guide.

Grid penetration challenges

According to Hawaiian Electric, about half of its 416 circuits on the island are of concern as far as the level of PV penetration and the effects on circuit and system-wide stability and reliability. The net effect of these challenges on potential buyers of rooftop PV systems is to delay and, in some cases, deny, for an indefinite period of time, their ability to install and interconnect a solar electric system to the grid. There have been ongoing discussions between HECO engineers and inverter manufacturers as far as making programming changes to both already installed inverters and new systems going in, with the goal of modifying ride-through capabilities of existing and new PV systems to improve grid stability and to allow for even higher levels of rooftop PV penetration.

But the answer to a fundamental question still remains elusive: how much more distributed generation PV capacity can the current grid accommodate? Five or six years ago, when grid-tied PV was still in its infancy, utility engineers did not likely foresee that their systems would have as much PV as we have now in 2015 and that the grid could safely and reliably handle that much distributed generation. That said, we in Hawaii are truly living in the new frontier of what’s possible, with current technologies, and what’s not, as far as the grid’s ability to handle surplus power produced by hundreds or thousands of small rooftop power plants on a circuit-by-circuit basis and for all those systems to handle grid faults and anomalies. In 2015, there is not likely to be a magic-bullet programming change or the miraculous emergence of vastly smarter inverters that will allow for the Hawaiian Electric companies’ breakthrough ability to accept dramatically higher percentages of rooftop PV penetration.

Net energy metering

Available in Hawaii since July 2001, net energy metering has allowed around 50,000 electric utility customers across the state to get the maximum value for their solar kilowatt-hours. NEM customers receive full retail credit for all the power that their PV systems produce. While a significant benefit to NEM customers, and to all those contractors who provided these turnkey systems, there have been fewer benefits for the nine or so out of ten non-NEM ratepayers who have been effectively subsidizing those utility customers who have added solar PV. From the perspectives of a number of PV industry executives, NEM’s days are numbered in Hawaii, whether we like it or not. In their submissions to the Public Utilities Commission last August, Hawaiian Electric proposed a road map that would phase out NEM 1.0 in favor of an interconnect agreement that is less advantageous to the end user, something that Kauai Island Utility Co-Op already implemented several years ago, with nary a peep when the mandated percentage of NEM systems was reached in its service territory.

The successor to the current NEM agreement could impose a monthly surcharge to NEM system owners. Another possibility is that while new NEM 2.0 customers would enjoy full retail value for power produced and consumed on site, any surplus power fed back into the grid would be paid for at the avoided-cost (i.e., wholesale) rate for power. Any such changes to the current NEM program in the HECO, MECO and HELCO service territories will come after considerable debate and impassioned lobbying from interested parties far and wide and would be subject to PUC approval. And that will take time, leading to the conclusion that any successor to NEM 1.0 will not likely go into effect in 2015.

Tax credits

The federal Investment Tax Credit is scheduled to reduce from the current 30 percent to 10 percent for businesses as of January 1, 2017, while going down from 30 percent to zero for homeowners. Congress may act to extend the tax credit, but we won’t likely know whether the serious support needed to make this happen exists until the latter part of next year. So, the fate of the ITC in the latter half of 2016 will not have much bearing on rooftop PV sales in 2015, though utility-scale projects, given their considerably longer start-to-finish timeframes, will face a greater sense of urgency to get details, approvals and permits nailed down this year.

Regarding the state Renewable Energy Investment Tax Credit (REITC), rather amazingly, there’s still no sunset date for the program, an illustrative example of the power and influence of the solar industry and its local and mainland friends and allies. And it would appear that there will be no appetite this coming legislative session in Honolulu to tinker with the solar tax credit. In 2012, the last year for which the state Department of Taxation has complete records, something close to $170 million was claimed by homes, businesses and mainland finance companies for the REITC, with about half of that going out of state. Despite that formidable hit on the state’s general fund and a similar sum likely for 2013, there appears to be little concern that will lead to changes in the current law, making for little impact on PV sales in 2015.

Energy storage

A growing number of those working in the PV field are coming to believe that affordable, cost-effective and readily available energy storage, specifically batteries, represent something of the promised land, a release from the confines and perceived obstructionism of the utilities. A number of contractors are working on designs that incorporate battery storage and which would allow surplus PV power to be stored at the site rather than being fed to the grid, a model known as "non-export." While sub-optimal from a number of perspectives, this type of PV system could be a workaround to allow homeowners and business owners to avoid grid penetration constraints and delays and allow them to install their systems sooner rather than waiting for utility approval.

With the introduction of newer battery technologies to store renewable power -- such as lithium-ion, lithium-iron and aqueous hybrid ion -- there’s also hope for greater energy density and price reductions that will lead to completely off-grid living as a viable option in the not-so-distant future. As far as the near-term impact of site-located battery storage in Hawaii acting as a significant offsetting boost to the cooled consumer demand and grid penetration challenges, it’s unlikely that this coming year will see this form of storage making much of a difference.

Oil prices and liquefied natural gas

With the expanded use of hydraulic fracturing ("fracking" for short) in a growing number of states on the mainland, the prices for oil and natural gas have trended downward. This has the effect of lowering energy costs in the state, both at the pump and on monthly electric bills. Considering the volatility of oil prices, few would have predicted a year ago that the price for a barrel of oil would hover at $50 at the beginning of 2015. Furthermore, in light of the long-stated goal of reducing our dependence on imported oil, it’s unlikely that many would advocate reversing course and importing more of it, no matter how low the price dips temporarily.

Similarly, the availability of cheaper natural gas, which has to be cooled to -260 degrees F in order to be liquefied for transport across oceans, has sparked a vigorous debate as to whether to import a lot more liquefied natural gas (LNG) to act as a cleaner, perhaps more versatile bridge fuel to a more renewable-energy-based future. Even assuming that considerably more LNG were to flow into Hawaii and that the price paid for that fuel source were to stay relatively low, the net effect on the PV industry in the state would be marginal. Whether the price per kilowatt-hour of utility power is 40, 30 or even 20 cents, the other incentives that support having a solar electric system installed on one’s home or business would still be compelling. So look for the variable costs of oil and gas to have little effect on the state’s PV industry in 2015.

Prognosis

After experiencing phenomenal growth from 2007 to 2012, the state’s solar electric industry has experienced a substantial and painful slowing of the ride over the past two years. As both an owner of a PV contracting company, which has a direct stake in the continued viability of this line of business, and an academic who also takes the macro, bird's-eye view of the field, I would like nothing better than for someone to present a persuasive and credible case for our improved fortunes in 2015.

The case for the wonders of the smart grid, smart inverters and breakthroughs in battery technologies can be seductive, but they are unlikely to come to fruition in the near term of 2015. Throw in the possible sale of Hawaiian Electric Industries to a company almost 5,000 miles away and both the CEOs of NextEra Energy and Hawaiian Electric stating that there should less of an emphasis (read: value) put on rooftop PV, and it’s hard to envision an optimistic scenario unfolding in the coming year for the hundreds of companies here that live and breathe this trade.

***

Marco Mangelsdorf is president of ProVision Solar, founder of the Hawaii PV Coalition, and a lecturer on energy politics at University of Hawaii, Hilo and University of California, Santa Cruz.

41

41

15

15

9

9