Reporting from the Intersolar show in San Francisco -- When last we spoke with Chris O'Brien of Oerlikon Solar in April of this year, Oerlikon was plugging away, selling amorphous silicon (a-Si) photovoltaics manufacturing equipment to a number of customers. The firm was working on improving efficiency and throughput against the backdrop of a rather high profile struggle by a-Si competitor Applied Materials, whose customers are declaring bankruptcy (Sunfilm) and backing out of factories (Signet).

Since then, Applied has de-emphasized its a-Si efforts and sent an a-Si team to China to work on a Chinese fab-to-farm project, while Oerlikon continues to make some headway with this technology. They're not the only one -- Sharp is absolutely committed to a-Si, Astroenergy in China is working on this, and we just heard from a stealth startup, also working in a-Si, that is boasting efficiency potentials in the low teens. We will be checking on that.

In fact, Oerlikon just announced a new customer, Baoding Tianwei, which is upgrading their factory from single junction to tandem junction and bumping their production capacity from 46 megawatts to 75 megawatts, via a big increase in panel efficiency. That firm is planning an additional 120 megawatts of production capacity in the next two years with a near-term market focus in Europe.

But Oerlikon's O'Brien has optimism for the U.S market, expecting it to grow to about 800 megawatts this year, up from 450 megawatts last year, with the biggest growth in utility-scale and commercial rooftops, as opposed to Europe's solar growth engine, residential roofs.

So how has Oerlikon been able to make a-Si manufacturing work with some marginal success while others have not?

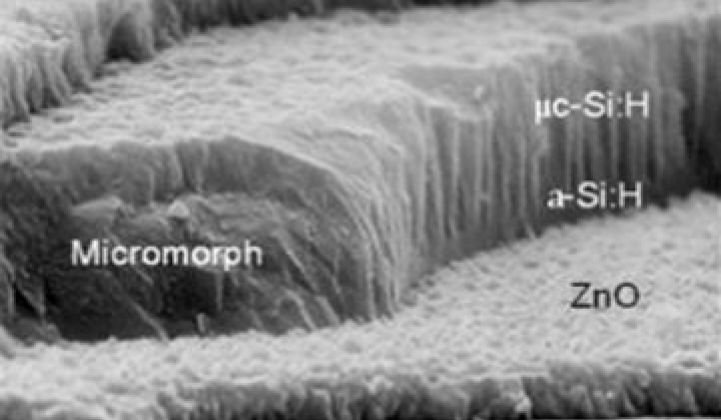

According to O'Brien, Oerlikon had some key first-mover advantages, such as a longer legacy in micromorph (tandem junction) and starting off with an efficiency advantage, that become more important when crystalline silicon (c-Si) joined First Solar as the cost leaders.

"Another first-mover advantage was our strength in TCO [transparent conductive oxide]. Our TCO provides almost a 1 percent boost in efficiency," said O'Brien. Oerlikon uses a zinc oxide material, while Applied uses a tin oxide in this important manufacturing step.

Oerlikon continues to makes improvements, such as attempting to reduce material costs of modules by 20 percent and using a new reflective coating from DuPont that allows thinner silicon layer thickness and reduces efficiency degradation.

Although O'Brien would not reveal a capex number, he did speak about module costs, and those numbers sound pretty good. Last year's cost was $1.30 per watt, this year is under a dollar, and 70 cents per watt is achievable by the end of the year, according to O'Brien.

O'Brien's not a newcomer to the field. He's worked at utility AES and Sharp Solar, and was also the chairman of SEIA (Solar Energy Industries Association).

Achieving low module cost-per-watt and low capex cost-per-watt is difficult with any solar technology and perhaps even more so with low efficiency a-Si. Competing against Applied Materials is also a challenge -- no one should underestimate the capabilities of that firm. But Applied is not the real competition here. Instead, it's First Solar and a score of low-cost c-Si companies. And Oerlikon is going to have to overachieve at execution and R&D to keep up with those pacesetters.

In the view of GTM Research Solar Analyst Shyam Mehta, "Amorphous silicon’s long-term future lies in the commercialization and adoption of tandem-junction technology. First movers in this space (Sharp, Oerlikon customers) have a distinct advantage." (See Mehta's recent report, Thin Film 2010, Market Outlook to 2015.) Mehta adds, "When it comes to single- and tandem-junction technologies, Oerlikon emerges as the clear efficiency leader in the field: four of the top six single-junction and five of the top seven tandem-junction firms use its manufacturing equipment."

41

41

15

15

9

9