Based on the latest data from the first half of 2012, as well as discussions with vendors, 2012 is on track to have fewer advanced metering infrastructure (AMI) and automated meter reading (AMR) shipments than 2011, according to the latest North American AMI Deployments & Market Share report. Deployments were down across the electric and gas sectors, and many vendors project that figures for the remainder of 2012 will drop even more sharply than the existing data indicates.

On the other hand, shipments to the water sector have increased by nearly 11 percent this quarter, or roughly 150,000 units. This upward water trend is expected to continue through 2012. However, the water marketplace is only 25 percent the size of electric plus gas, and the modest water growth will not compensate for the other losses.

FIGURE: Annual Shipments of AMI and AMR by Sector

Source: North American AMI Deployments & Market Share: Q2 2012

“This is a very lumpy industry, meaning that there are a few huge projects that dominate the numbers, and the many small projects can never overwhelm the large ones," says Howard A. Scott, author of the report. "When these large projects come to an end, suddenly that data isn’t there anymore. There are some big new upcoming projects that haven’t yet hit the major rollout stage, which should mostly compensate for projects that are currently coming to an end.”

Today, GTM Research and Howard A. Scott of Cognyst Advisors publish the North American AMI Deployments and Market Share: Q2 2012 report. This 29-page quarterly report is part of the GTM Scott AMI Market Tracker and provides the latest information on the AMI deployment and implementation trends of electric, gas and water utilities in North America.

Primary data on shipments in the report is collected directly from over 50 major vendors and analyzed by our team of experts to provide the most timely and strategic outlook available on the industry. The report features analyses of:

- North American AMI shipments

- North American AMI market share by vendor

- North American AMI market share by communications architecture

- AMI deployments for electric, gas and water utilities

- Total North American market size and remaining addressable market

“As large IOU deployments near completion, it will be critical for AMI and AMR vendors to provide solutions tailored to the specific needs of the municipal and cooperative utility markets,” said Zach Pollock, the Smart Grid Analyst for the report at GTM Research. “Furthermore, with GTM Research and Howard Scott forecasting flat growth for the market through 2013, we're unlikely to see the accelerated AMI and AMR deployment schedules we witnessed during the ARRA boom in 2009 and 2010.”

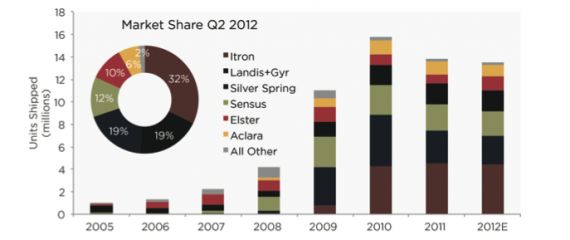

FIGURE: Quarterly and Annual Electric AMI Market Share by Vendor

Source: North American AMI Deployments & Market Share: Q2 2012

This report includes exclusive data and analysis on Aclara, Elster, Itron, Landis+Gyr, Sensus, Silver Spring Networks, and many other vendors.

The GTM Scott AMI Market Tracker is the smart grid industry’s most comprehensive subscription service, providing energy professionals with strategic data on North American utility AMI and AMR markets. To learn more about this quarter’s report, as well as the Tracker subscription, please visit http://www.greentechmedia.com/research/gtm-scott-ami/.

41

41

15

15

9

9