Following in the footsteps of states like New Jersey, Pennsylvania, and Maryland, Massachusetts is about to implement a Renewable Portfolio Standard (RPS) solar requirement. Like other solar RPS states, Massachusetts will spark solar demand by creating a market for Solar Renewable Energy Credits (SRECs), each of which represents one megawatt-hour of solar electricity generation. And like other solar RPS states, Massachusetts will set a requirement that utilities source a certain amount of their electricity portfolios from solar power, either through ownership of solar generation or the purchase of SRECs from privately owned projects.

But that's more or less where the likeness ends. Outside these basic characteristics, the new Massachusetts program contains two elements that set it apart from other states. First, it creates a unique mechanism to enable long-term project financing based on SREC revenue, an issue which has been a thorn in the side of other RPS carve-out programs. And second, it contains a series of self-correcting adjustments to maintain a growing solar market without causing oversupply.

These elements make the Massachusetts program worth understanding in greater detail. If successful, the Massachusetts SREC market could provide an example for new state policies emerging over the next few years.

Program Basics and History

RPS solar carve-outs have been instrumental in driving demand for PV in most of the major state markets outside California, including Arizona, Colorado, and Nevada. On the East Coast, New Jersey, Pennsylvania, Delaware, New Hampshire, Washington, D.C. and Maryland all have solar RPS carve-outs. Most of the East Coast programs (particularly in New Jersey, Pennsylvania and Maryland) have high-value SRECs markets, with prices typically ranging from $100/MWh to $500/MWh.

Massachusetts passed its RPS solar carve-out in the Green Communities Act of 2008, which dictated that the state Department of Energy Resources (DOER) determine standards for the carve-out. The DOER went through a stakeholder review process and released final design guidelines in December 2009.

Basic requirements for projects:

- Projects must be located in Massachusetts

- Projects must be 2 MW dc or smaller

- Projects that have received substantial ARRA funding, other than the cash grant in lieu of ITC, are ineligible.

How Big Will the Market Be?

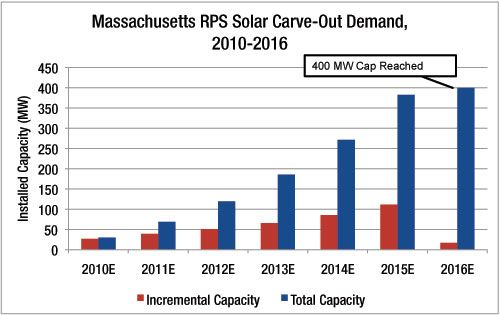

In contrast to most RPS carve-outs, which set a percentage of electricity sales to be sourced from solar power, the Massachusetts program identifies a total amount of solar generation in MWh and divides it among utilities according to their proportion of total state sales. This requirement is known as the Minimum Standard. The program begins with a Minimum Standard equivalent to 30 MW of capacity in 2010, and increases by 30 percent more each year than it did the previous year. For example, if the Minimum Standard jumps from 30 MW in 2010 to 70 MW in 2011 (a 40 MW jump), the 2012 Standard will increase by 130 percent of 40 MW, or 56 MW.

The Minimum Standard is capped at 455,520 MWh, which will enable around 400 MW of total capacity. After this point, new applications will be transferred to the general Massachusetts RPS program. See the chart below for our early projections of market growth.

Each year, the Minimum Standard is adjusted based on alternative compliance payment (ACP) volume from the previous year (indicating undersupply of SRECs) and banking volume from the previous year (indicating oversupply of SRECs). This is the first self-correcting mechanism to keep the market near equilibrium.

Alternative Compliance Payment (ACP)

The alternative compliance payment is essentially the penalty that a utility must pay if it does not meet its RPS obligation in a given year. In practice the ACP sets a ceiling price on SRECs, as utilities will find it more economically efficient to pay the ACP if SREC prices rise above it. The Massachusetts RPS carve-out has a 2010 ACP of $600/MWh, among the highest in the nation. The state has the ability to reduce the ACP each year, but never by more than 10 percent in a given year.

Bankability Through SREC Price Certainty

The most innovative element of the Massachusetts program is its mechanism to provide the option for long-term SREC price certainty for project investors while still allowing the market to determine most SREC pricing. It accomplishes this by setting up an Auction Account, into which any qualified solar project can place its SRECs. Here's how it works:

Auctions occur once a year. If SRECs are placed in the auction, they immediately become "extended-life" SRECs, which have a shelf life of two years rather than one. This creates an incentive for utilities to purchase SRECs from the auction. The auction is for a fixed price of $300/MWh, and utilities bid on volume rather than price. If a utility purchases a generator's SRECs, the generator receives the $300/MWh minus a $15/MWh Auction fee.

If the total bid volume doesn't clear all SRECs in the system, the remaining SRECs' shelf life is increased to three years and the auction is repeated. If bid volume still doesn't cover all SRECs, the utilities' Minimum Standard automatically increases by the same amount, essentially requiring utilities to purchase the remaining volume.

Projects are guaranteed the option to opt-in to the Auction for a set term of years following the beginning of the project's operation. This term begins at 10 years in 2010, but can be adjusted annually depending on whether the market is long or short. For each full 10 percent of the Minimum Standard met by the Auction, the Opt-in Term is reduced by a year, with a maximum reduction of 2 years annually. This term will not go below five years for the first seven years of the program.

There is also a short market adjustment such that, if more than 5 percent of the total obligation is met through ACP payments, the opt-in term is re-set to 10 years. Like built-in adjustments to the Minimum Standard, these mechanisms are designed to ensure that the market doesn't suffer from significant over- or under-capacity as it grows.

The auction mechanism gets a little bit confusing, but here is what matters. If you own and operate a solar project in Massachusetts, you'll be able to sell the project's SRECs through a long term contract or on the spot market, just as you can in other SREC states. But if a long-term contract is unavailable (as it usually is) and you still need revenue certainty in order to finance the project, you can opt-in to the Auction. If your project comes online in 2010, you'll have a virtually guaranteed 10-year revenue stream of $285/MWh, more than sufficient to enable project financing. And if this proves to be so attractive that the market shows explosive growth, later projects will be ensured fewer years of revenue.

The Outcome

In addition to the RPS program, Massachusetts has just re-launched its Commonwealth Solar Rebate program (now deemed Commonwealth Solar II), a valuable incentive that was closed in late 2009 due to full subscription. The Commonwealth Solar Rebate II will provide incentives for projects up to 5 kW through $4 million in ongoing annual state funding. There will also be a dedicated $8 million in funding from the ARRA for projects between 5 kW and 200 kW. This program will expire when the $8 million has been allocated, but the residential rebate is expected to continue "for the foreseeable future." These projects will qualify for the RPS as well as rebates.

As we predicted in the recent GTM Research report The United States PV Market: Project Economics, Policy, Demand and Strategy Through 2013, Massachusetts will never approach California's market size, but it will be an important secondary demand center for PV over the next few years. The success of the solar carve-out program remains to be seen, and it does carry the danger of being overly complex. But if I were a gambler, I would bet that the Massachusetts program will provide the model for future RPS solar carve-outs.

41

41

15

15

9

9