Massachusetts is known for many things: the first Thanksgiving, an unwavering dedication to Dunkin' Donuts coffee, Greentech Media’s global headquarters, Boston accents, and the best clam "chowdah" in the country. It might soon add another defining trait: solar energy.

According to the recently released U.S. Solar Market Insight report, Massachusetts installed 237 megawatts of solar PV in 2013, doubling its cumulative capacity. That puts the state in fourth place in the United States, ranking behind only California, Arizona, and North Carolina.

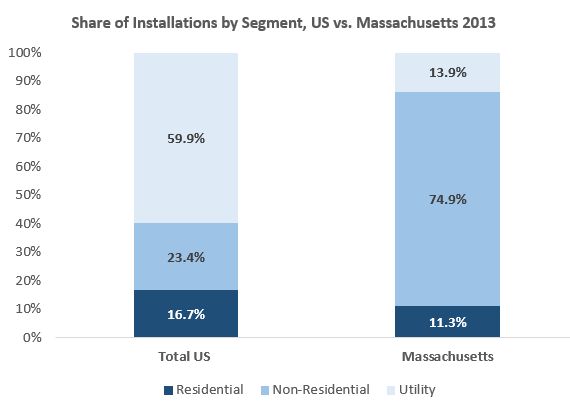

Half of all installations in Massachusetts occurred in the fourth quarter of the year, led by the non-residential (i.e., commercial) sector with 95 megawatts installed. In fact, Massachusetts installed more non-residential solar last quarter than did any other state in the U.S., driven in large part by the SREC I interconnection deadline of December 31, 2013.

Source: U.S. Solar Market Insight

According to the U.S. PV Leaderboard, Borrego Solar Systems, Citizens Energy, and Gehrlicher Solar America Corporation were the leading non-residential installers in the state through the first three quarters of the year. GTM Research is still crunching the installer share numbers from the record-breaking fourth quarter.

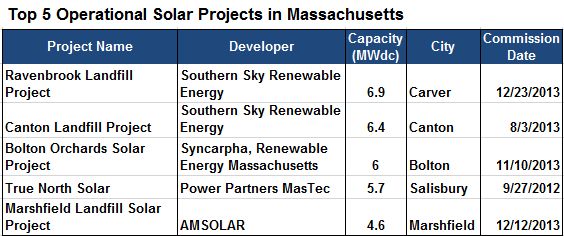

GTM Research’s Utility PV Market Tracker monitors solar projects from Pittsfield to Provincetown, and all municipalities in between. We tapped into the tool to pull out the top five operational solar projects in Massachusetts, all of which are commercial.

Source: GTM Research Utility PV Market Tracker

The U.S. Solar Market Insight report outlines three factors that will help Massachusetts maintain high installation numbers in the first half of 2014.

- Under the terms of SREC I, systems larger than 100 kilowatts that expended over 50 percent of project costs by December 31, 2013 were granted a six-month extension to complete construction and receive an authorization to interconnect by June 30, 2014.

- Out of the 672 megawatts of projects qualified for SREC I, just 410 megawatts came on-line by the end of 2013, leaving the potential for up to 262 megawatts to be completed in the first half of 2014.

- Large ground-mounted projects have an incentive to come on-line during the current program rather than hold off until SREC II, which favors smaller rooftop systems. The current draft proposal places an annual limit on the capacity that may come on-line in the ‘Managed Growth’ sector, designed to prevent SREC oversupply. This includes all ground-mounted projects over 650 kilowatts and ground-mounted projects between 25 kilowatts and 650 kilowatts that use less than 67 percent of annual electric output on-site. For Compliance Year 2014, this limit is expected to be just 26 megawatts.

“Ultimately, what Massachusetts is doing is putting in place a structure that is going to create a sustainable market moving forward,” said SEIA CEO Rhone Resch in last week’s Energy Gang podcast.

Cumulatively, Massachusetts now has 440 megawatts of PV capacity, three-quarters of which are non-residential. Almost everyone in the Bay State agrees: solar is wicked cool.

***

For more insight into Massachusetts and 29 other states’ solar markets, purchase the full U.S. Solar Market Insight report.

41

41

15

15

9

9