With solar module prices dropping by over 50 percent in the past year, thin-film PV manufacturers are in a fight for survival. In 2011, the technology’s global market share eroded to 11 percent from its peak of nearly 20 percent in 2009 -- a year when thin film’s cost advantages in relation to rival crystalline silicon (c-Si) technologies made it the darling of the solar industry. Today however, thin film is trapped in a fiercely competitive photovoltaics (PV) supply market, as oversupply has brought sub-$1 per watt c-Si to global markets.

“With Tier One c-Si PV prices dropping to averages of $0.87 per watt in 2012, thin film manufacturers must now be more frugal, technologically aggressive, and creative in implementing downstream strategies that will help them survive current competition and develop secure markets down the road,” said MJ Shiao, Senior Analyst at GTM Research and the report’s lead author.

At 321 pages, Thin Film 2012–2016: Technologies, Markets and Strategies for Survival is the fourth edition of GTM Research's annual update on the thin-film PV space. With detailed, accurate data, a granular examination of manufacturing costs, technology analysis, recommendations for supplier strategies, and competitive intelligence on the top 80 firms in the space, it is the most comprehensive, data-driven and objective assessment of the market available to date.

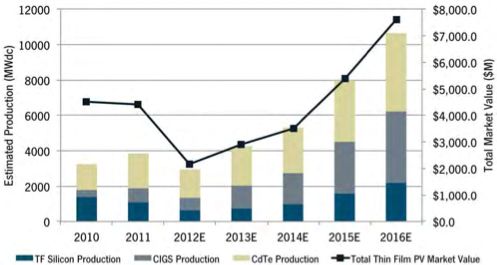

While GTM Research forecasts global thin film production and total market value to dip below $3 billion in 2012, the report projects an uptick in thin film demand in 2015 to 2016, when the total market recovers to $7.6 billion. The industry’s rebound will be predicated on the continued, though muted, success of First Solar (NASDAQ:FSLR) and the execution of efficiency, yield and scale road maps from other thin film manufacturers.

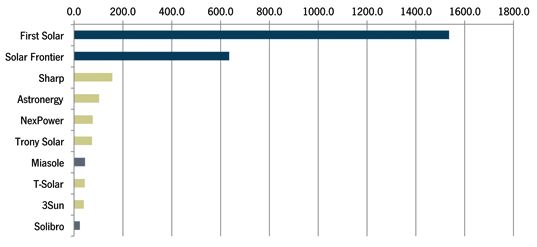

Figure: Top Thin Film Suppliers by Production, 2012 (MW, Est.)

Source: Thin Film 2012–2016: Technologies, Markets and Strategies for Survival

In particular, the report forecasts strong growth in the copper-indium-gallium-diselenide (CIGS) technology segment, forecasting production at 4 gigawatts in 2016. In 2011, Solar Frontier established itself as a dominant supplier with roughly 400 megawatts of CIGS PV shipments, but companies like MiaSolé and TSMC (NYSE:TSM) could emerge in the next few years as top thin film suppliers with the cost of manufacturing approaching $0.50 per watt. Venture investments in CIGS surpassed $305 million in the past two quarters, albeit at depressed valuations. Coupled with increased interest from global industrial conglomerates on the sidelines, GTM Research predicts major acquisitions in the near future.

Figure: Thin-Film PV Base Forecast, 2010–2016E

Source: Thin Film 2012–2016: Technologies, Markets and Strategies for Survival

“Thin-film PV has historically been led by a few manufacturers and a long tail of aspirants, because thin film manufacturing IP is heavily guarded,” said Shiao. “Only those that have the delicate recipe that balances high yields and efficiencies, cash preservation in a bitter demand market, a pinch of downstream integration, and a corporate balance sheet to soften bankability doubts will taste the sweetness of market success.”

For more information on Thin Film 2012–2016: Technologies, Markets and Strategies for Survival and GTM Research's complete solar market analysis, visit www.gtmresearch.com.

41

41

15

15

9

9