Texas is a highly desirable state for investing in renewable energy, topping the list for wind power development, but it is still quite a nascent market for solar power. But that may be about to change.

Ernst & Young’s Renewable Energy Country Attractiveness Index for late 2013 ranked Texas as the sixth most attractive state in the U.S. for solar power development, as well as ranking it first in wind power development. Texas is a highly market-driven environment for renewable energy, and subsidies and mandates are minimal at the state level. The only state mandate for renewables was exceeded many years ago by market forces alone, so it essentially has no impact today.

Municipal utilities seem to be the most promising market for solar power wholesale contracts in Texas. Specifically, the City of Austin’s new solar mandate is promising, with at least 100 megawatts of local wholesale contracts to be awarded, but full details are not yet available on this brand-new program just approved by the city council in late August.

The direct access/retail choice option for selling power directly to industrial customers is another attractive option. Under this approach, industrial and commercial customers may choose to buy their power directly from solar projects. This is a new market in Texas, made possible by the declining cost of solar. It is not clear how big this market is, but there are many large industrial customers that would likely be interested in discussing competitively priced solar options.

Texas is fairly new on the scene in terms of solar development, but it is the national leader in wind power and has been for a number of years.

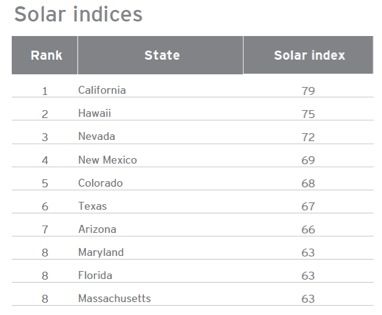

FIGURE: Ernst & Young Solar Index, 2013

Texas has faced transmission issues as a consequence of its large and rapid wind power buildout. However, its response has been to create a number of Competitive Renewable Energy Zones that include major new transmission facilities. Combined, these zones will be able to handle 18,500 megawatts of new wind and/or solar power.

Texas installed 75 megawatts of solar in 2013 (compared to more than 1,800 megawatts of wind), placing it eighth in the nation, according to the Solar Energy Industries Association (SEIA). Even though Texas has experienced modest solar power growth to date, its potential, according to E&Y, is the greatest in the nation by far due to its abundant land area, relatively easy permitting, and significant available transmission capacity for new projects.

Natural gas power is the default resource for new generation. While long-term contracts for natural gas power can be relatively expensive, the short-term “locational marginal price” for wholesale power on open markets is generally much cheaper, currently around $40 to $50 per megawatt-hour. This is the de facto competitive benchmark for solar power as well as wind power, with one important caveat: contractual prices for power are generally substantially higher than real-time market prices because of the inherent volatility in market prices that can be avoided with long-term contracts for solar and other renewables. This lack of pricing volatility is a major benefit of renewable energy and is made possible due to the fact that renewable energy facilities have zero fuel costs. Only the capital costs, financing costs, and operations and maintenance are factors in the end price of wind and solar power.

Wind power has been cost-competitive with natural gas in Texas for about a decade. Solar power, however, is only now becoming cost-competitive, because solar power costs have dropped dramatically in the last five years. This explains the state of the solar market today, as well as the big reason why solar power is set to take off in Texas. There is a growing discussion of a “solar boom” in west Texas as more and more companies option land for future solar projects in that area.

While it's still early for solar in Texas compared to states like California, New Jersey and Hawaii, the interconnection queue suggests that solar power development is ramping up quickly. The April 2014 interconnection queue report from the Electric Reliability Council of Texas (ERCOT), the entity that runs Texas’ electricity grid, shows that 3,457 megawatts of solar power projects are at various stages of interconnection. This information supports the conclusion that the Texas solar energy market is set to grow dramatically in the next couple of years.

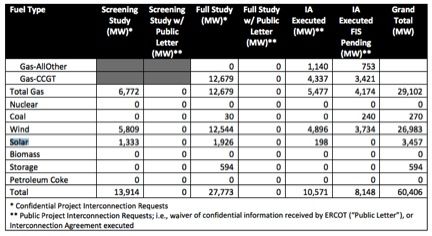

FIGURE: ERCOT Interconnection Queue

The Renewable Generation Requirement is the primary policy mechanism guiding renewable energy development in the state. However, its impact has been minimal because market forces alone have caused the huge boom in wind power in Texas for the majority of the time since this law was enacted in 1999. The law requires utilities to procure 5,880 megawatts of renewables by Jan. 1, 2015, but this requirement was met about a decade early, almost entirely with wind power. In 2014, Texas has more than 13,000 megawatts of wind power installed and leads the nation in wind power procurement (by a long shot).

The utility-scale solar market in Texas is at this time almost entirely based on municipal utility demand, rather than the more traditional investor-owned utility model that is in place in other states. For example, a 41-megawatt solar project (Alamo I) has been completed as the first phase of a larger 400-megawatt project. Power will be sold to the City of San Antonio’s municipal utility, CPS Energy. The City of Austin has also recently contracted for 150 megawatts of solar from Recurrent Energy.

The City of Austin has been a leader in renewable energy procurement and has enacted its own renewable energy requirement of 35 percent by 2020, with at least 200 megawatts of this from solar. Austin just doubled down on these policies when it approved a new law in late August that requires at least 65 percent renewables by 2025. The City Council approved a new resolution that will make solar power the default energy resource for procurement by the municipal utility. This change was prompted by a detailed analysis undertaken by a task force for the City of Austin, as well as by the recent completion of the contract for 150 megawatts of solar power with Recurrent Energy at a price of only $50 per megawatt-hour. This is a very aggressive price for solar power. While this contract price is impressive, it doesn’t mean much until the project is built, and, as is often the case, highly aggressive contractual prices often increase substantially by the time the projects are completed, or the projects often fail.

Austin’s new solar policies are expected to expand Austin’s solar market from 200 megawatts currently to at least 1,000 megawatts by around 2017, with 200 megawatts from local solar in the city and 600 megawatts of utility-scale solar outside of the city. At least 100 megawatts of the 200 megawatts of local solar must be behind the meter, which means that the other 100 megawatts will probably be small wholesale solar contracts. This new mandate also includes 200 megawatts of energy storage to help balance the grid as solar penetration increases.

The details of the new policies have not yet been released, so it is not clear how much of an opportunity this is for solar developers.

Similarly, the City of San Antonio has a requirement of 20 percent renewables by 2020 (about 1,500 megawatts), with at least 100 megawatts from solar, to be procured through its municipal utility, CPS Energy. It is likely that as the cost of solar power continues to decrease, utilities like CPS Energy will increasingly seek to procure solar power alongside or instead of wind power in order to have a more diversified and peak-friendly renewable energy portfolio.

Texas commercial utility customers enjoy the ability to choose their own power provider, which includes contracting with private parties to buy solar power. This is known in Texas as Retail Choice (see p. 18 of the linked document for a brief description of Texas’ programs). These commercial customers are still billed and serviced by the private utility, but the generation component of their power bill is paid to the third-party solar developer. This is another option for obtaining a long-term PPA for solar projects in the state.

The Texas solar market is still developing, but reliable evidence suggests that it is at the beginning of a boom period. And given Texas’ potential for solar power development, it is conceivable that Texas could surpass California as the nation’s biggest solar state, as it did with wind power a few years ago.

***

Tam Hunt, J.D., is owner of Community Renewable Solutions LLC, a renewable energy project development and policy advocacy firm based in Santa Barbara, California and Hilo, Hawaii.

41

41

15

15

9

9