PV manufacturers are in a mad dash to determine their strategies to serve the U.S. utility PV market. Despite the fact that there is less than 300 MW of cumulative capacity connected on the utility side of the meter today, the market is widely recognized as representing an enormous growth opportunity over the next five years.

Suppliers have two fundamental options through which to take advantage. They can either sell their product (be it modules, inverters, systems, racks, etc.) to third-party developers, or they can develop their own plants. A few suppliers (SunPower, First Solar) do both -- a thorny strategy that requires careful avoidance of competing with one’s own customers. Still, let’s look at each strategy individually.

Selling Products

In order to gain share, many suppliers have created and introduced new products tailored for large-scale projects. The figure below contains a sample of the most prominent of these products that have been introduced in the U.S. to date. In general, supplier strategies tend to fall into one of two categories:

· Large-scale modules/inverters: At a minimum, most suppliers have introduced a larger series of modules and/or inverters to serve the utility market. The larger size of these products is intended to drive down installation time and materials costs. Larger inverter products also often contain additional features that are attractive to utilities and grid operators such as control of reactive power and voltage ride-through.

· Pre-designed modular systems: A few suppliers have elected to create integrated systems for sale as a single package. These systems are often shipped to the installation site pre-assembled in order to cut down installation time and are pre-designed in order to drive down system design and engineering costs. SunPower claims that the pre-engineered nature of its Oasis Power Plant enables installation of up to 1 MW per day.

_540_390_80.jpg)

Source: GTM Research

The difference between these two supplier strategies is best exemplified by a comparison of SunPower and First Solar’s strategies, both within the utility segment and in general. First Solar has always relied on a small number of relationships with well-established developers, primarily in Europe. In 2009, the company’s top five module purchasers each accounted for more than 10% of First Solar’s total sales, and were all based in Germany or France. This approach enables First Solar to focus purely on being cost-competitive with regard to modules. The company’s customers are then tasked with procurement of BOS components, as well as with system design and engineering. This results in more work for the developer but greater opportunity to tailor each project to the needs of the site and power purchaser.

In contrast, SunPower has always placed its focus on providing a full-service solution to customers. In the residential/small commercial segments, SunPower acts through its dealer network, for which it provides logistics support, financing options, branding, training, supply chain management and lead generation. SunPower has also introduced a series of integrated systems intended to increase ease of installation for customers. Following this logic into the utility segment, SunPower introduced its Oasis Power Plant, a 1 MW modular system that the company claims can drive down BOS costs by up to 25% through materials savings, field labor and standardization of procurement. Project developers using SunPower’s Oasis product have less work to do in terms of procurement and system design, but have less ability to tailor procurement according to the individual project.

In general, the two product types will appeal to different developers. More experienced, larger developers will likely prefer to conduct their own procurement of BOS components and will lean toward suppliers with First Solar’s model. In particular, developers with large pipelines that can procure components at scale will benefit from volume discounts on individual components that will exceed those provided by integrated system suppliers. Developers with smaller pipelines and less system design experience will likely see great value in the integrated system purchase, which reduces their workload while aiding in the bankability of the project. The open question remains whether utilities prefer pre-engineered systems and will procure accordingly. Thus far utilities seem indifferent, but there is no telling what the future will hold.

In the short term, the problem for most top- and second-tier suppliers is not finding projects for which they can provide modules, but rather determining which projects are likely to be completed. Given the abundance of contracted and early-stage projects in the market today, suppliers must be selective with regard to their developer relationships. In the absence of good due diligence on developers, suppliers can easily find themselves spending substantial time on projects that were never likely to succeed in the first place. Worse, suppliers could end up in a situation where project failure forces them to re-allocate modules in a hurry. Like utilities and power purchasers, developers must conduct a rigorous analysis of each project and project proponent prior to signing any contract.

Downstream Integration

It is no secret that many upstream players have completed, or have at least considered, downstream integration. SunPower, First Solar, and SOLON were among the initial few manufacturers with downstream operations; however, companies such as MEMC, Sharp and Suntech have not been far behind. There are a number of ways to develop a downstream operation, ranging from organic growth (i.e., hiring a team) to the acquisition of a developer. The figure below displays downstream integration mechanisms for suppliers to date. First Solar has been the only supplier so far to have acquired a pipeline without the developer itself (from Edison Mission), and has done so only after building a strong internal team. In contrast, at least five suppliers have chosen to acquire developers, including the most recent acquisition: Sharp’s $305 million purchase of Recurrent Energy.

_540_398_80.jpg)

Source: GTM Research

Based on recent conversations with developers, I’ve developed a slightly more nuanced view of downstream integration, particularly in cases where a supplier acquires a developer. In reality, there are two kinds of downstream integration:

· Full Integration, in which the developer is absorbed into the supplier and exclusively uses the supplier’s product in its projects (see First Solar and SunPower).

· Semi-Integration, in which the developer maintains its own brand and has the option to source outside components, although its parent company’s products maintain an inherent advantage -- see MEMC (SunEdison) and Sharp (Recurrent Energy).

For module suppliers with a local presence in strong markets (Germany, Italy, U.S., Canada), downstream integration could be an important strategy by which to stay competitive with Asian suppliers, as the loss in margins on expensive components can be made up by margins on project development (a practice that has worked successfully so far for SunPower). This is also a strategy by which sales channels can be created in markets where other options have proven to be unsuccessful.

In particular, downstream integration may make sense for amorphous silicon manufacturers with large corporate parents, as the balance sheet of the parent can go a long way towards securing low-cost capital, as well as potential EPC services (Mitsubishi, Sharp, Hyundai, Chint, QS Group). Additionally, the negative public perception of amorphous silicon may be difficult to counter in the near term, meaning that a producer’s best option may be to become its own customer and leverage the performance benefit themselves. In addition to these benefits, downstream integration carries the advantages of pipeline visibility and module allocation, both elements that First Solar has frequently noted.

Downstream integration obviously carries a fair amount of risk. The acquisition of a pipeline offers no guarantee that the projects will ultimately be completed. As we have noted a number of times, the fact that developers have been able to sell their companies and/or pipelines to suppliers at a premium has led some developers to believe that pipeline acquisition, at any cost, is their most important goal. Projects with untenable PPAs are just as likely to fail for a manufacturer as for a developer.

In addition to the risk of failure, there is an extent to which developing a downstream business forces module suppliers into competition with their customers. If the vertically integrated manufacturer is bidding on the same projects that potential module purchasers are, the purchasers may be wary of considering the same modules in the future. There are a number of ways to deal with this. First Solar maintains only a few module supply agreements in the U.S. and focuses mostly on its own projects, although it has developed a reputation for being willing to compete with its customers. SunPower is reportedly more explicit and sometimes informs potential customers whether it plans to bid on a particular project. Suntech has elected essentially to cut off its project development operations in order to focus on module sales, although it uses its internal team from the EI Solutions acquisition to aid customers in attaining project finance and developing their own projects.

Watch for more action over the next year. In particular, expect further developer acquisitions by large, corporate-backed manufacturers and more aggressive supply strategies from top- and mid-tier Asian c-Si manufacturers.

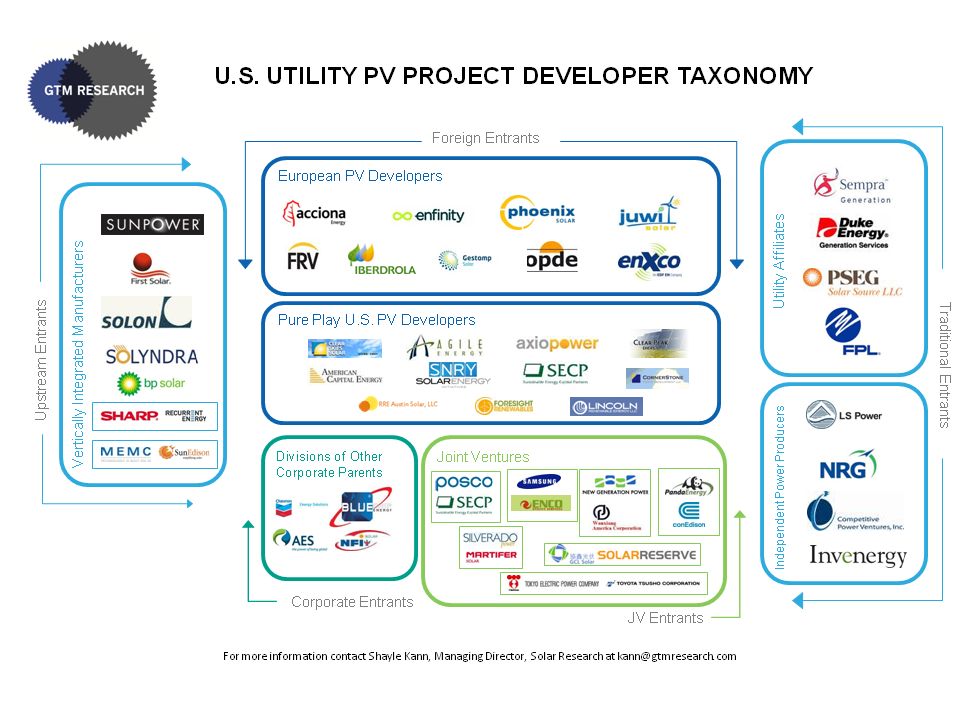

See the updated GTM Research Utility PV Project Developer Taxonomy here.

***

This is an excerpt from GTM Research's recently published comprehensive U.S. Utility PV Market report, The U.S. Utility PV Market: Demand, Players, Strategy and Project Economics Through 2015. For more on the report, go here.

41

41

15

15

9

9

{kind=link}