“How many people think we will see a 1-gigawatt merchant solar market in 2020?”

Shyam Mehta, senior analyst with GTM Research, posed that question to the crowd during a session at the 2013 Solar Market Insight conference in San Diego earlier this month. No one in the room raised a hand, but I was tempted to raise mine.

I understand the skepticism. Merchant power and solar development are two incredibly tough corners of the energy businesses to compete in. Combining them seems to aggravate their respective risks without raising their collective rewards.

But in one sunny corner of the world, that may be changing.

Latin America has a unique combination of attributes that make merchant solar viable today. Currently, 31 megawatts of merchant power are operational in Mexico and Chile, with a further 320 megawatts in the pipeline. These projects provide a case study for the largely untapped merchant power business model that may play a growing role in the global market.

Merchant power: A risky business

Traditionally, merchant power plants are those that sell power into competitive wholesale markets and are financed by investors. This is in contrast with either rate-base financed plants (which are paid off through utility bills over a long time horizon) or PPA-financed plants (which have a contract with an offtaker who agrees to pay a certain price for power over a period of time). As such, merchant plants are exposed to a different kind of risk than these other power plants, both in terms of the volume of electricity they sell (or demand) and the price of that electricity.

For the purposes of this article, the definition of “merchant power” will be broadened to include projects that face these same risks -- where the price of electricity is indexed to the spot market in some fashion, even if the mechanisms for that sale aren’t directly on the "competitive market.”

Merchant solar in Latin America

Two merchant plants are already operating in Latin America: the 1.2-megawatt Solairedirect project in Coquimbo, Chile and the 30-megawatt Aura I project in Baja California Sur, built by Martifer and Gauss. But given the risk profile of merchant power and the newness of solar development in the region, why are these developers pursuing this route?

To answer this question, let’s first rewind a little. Over the last year or so, as European markets were rocked by trade disputes and weakening incentives, many developers began looking for new markets to diversify their downstream portfolio. While Southeast Asia has stolen the headlines as the new center of global PV demand, many companies have quietly moved into Latin America -- lured by the strong insolation, growing economies, rising demand, and high electricity prices.

When these companies arrived, however, they discovered the region was not exactly rife with low-hanging fruit. Securing offtakers was difficult and there were no state incentives in place, meaning the strategy that often worked in Europe (using PPAs or incentives as a bankable revenue stream to finance the project) did not work in Latin America.

Although the outlook for securing offtakers has begun to improve as solar becomes better understood, many companies are looking to the merchant market as an alternative, or supplemental, strategy.

Let’s go back to the 30-megawatt Aura I project in Mexico, which is being financed by Nafin and the International Finance Corporation. A closer look at the Aura I project reveals the burgeoning value proposition of merchant solar.

The power plant has an offtaker contract with CFE, but the price of electricity under that contract is indexed to 98 percent of the node price where the project is connected. This arrangement, known as the Small Power Producers Program, is premised on the idea that if renewables can provide marginal power for a region at a cheaper going rate than what existing resources can provide, then renewables should have the option to compete in the market.

In years past, this program was only used by wind power. But as solar costs have fallen, and financing becomes more accessible, solar developers have rushed into the fray, with about 200 megawatts now under construction. Aura I is the first solar project operating under the scheme.

There are two numbers that help explain why Aura I is going the merchant solar route: 7.5 and 230.

First, 7.5 kWh/m2/day is how much insolation that Baja California Sur receives. This is about three times the average levels in Germany and 50 percent higher than southern California. Higher insolation levels translate to higher output for the power plant -- in this case, a capacity factor of about 31 percent.

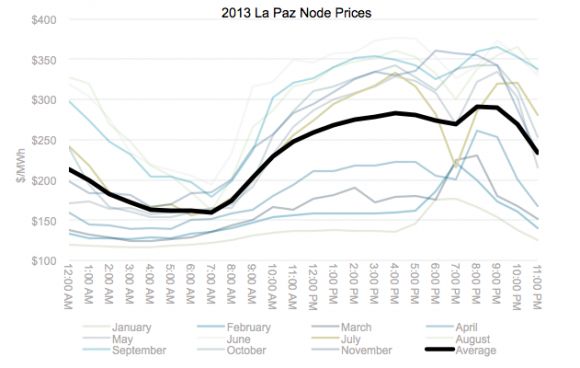

Second, $230/MWh is the average price of electricity in 2013 at the La Paz node in Baja California Sur, where the Aura I project is connecting. As the chart below shows, during peak hours in peak months, rates can be as high as $380/MWh. Given the insolation levels, that puts the back-of-the-envelope gross revenue from the plant between $13 million to $14 million in year one.

Net revenues will be much lower, of course, but that gives some sense of the value proposition of solar when the right node is selected (i.e., transmission-constrained, heavily dependent on diesel generation, high insolation, and strong demand).

Source: GTM Research

Farther south, in Chile, there are another 120 megawatts of merchant solar under construction.

The French company Total has teamed up with Etrion and Solventus to develop a 70-megawatt merchant power plant, Project Salvador, which will be built by SunPower and financed by OPIC. In addition, the 50-megawatt San Andres plant, being built by SunEdison, is currently under construction in the Atacama region.

The San Andres project has secured $100 million from OPIC and the International Finance Corporation. With marginal power prices between $150 to $200/MWh in the grid where the San Andres project will connect, and the project site receiving insolation levels around 7 kWh/m2/day, the case for merchant solar in Chile is clear. As long as marginal power prices stay high due to low rainfall (which appears to be in the cards), the San Andres project is also positioned to be profitable.

Latin America: A bellwether for the global merchant solar market?

Most solar developers have not had to think about the role of solar in competitive marketplaces, but there are some good reasons to consider it.

First, solar usually has priority in the dispatch stack because it has zero fuel costs and is non-dispatchable. This means that there is less concern about being priced out -- something that fossil fuel merchant plants have to worry about constantly.

Second, peak hours coincide with solar production, meaning solar has a natural synergy with the spot market. In terms of profits, it's important to remember that the back-of-the-envelope calculations noted above based on average power prices are likely low, because peak prices are higher.

Third, the risk of rising fossil fuel prices -- whether through carbon pricing, emissions caps, technology requirements -- paired with the promise of cost reductions for solar means that the value proposition is likely to improve as time goes on.

Fourth, in places where capacity markets also exist, there is the potential to bring in additional revenue for the capacity value solar provides and defray capital costs.

Merchant solar cannot work in every market. But, in coming years, expect more developers to look for that sweet spot where merchant solar plays -- and expect the number of sweet spots to grow with every passing year.

So will we reach a 1-gigawatt merchant market in 2020? I can’t say for sure, but it looks like we may be a third of the way there by 2015.

***

For an in-depth look at how Latin American solar markets are evolving, read GTM Research's newly released Latin America PV Playbook.

41

41

15

15

9

9