The White House just released a rigorous review of the controversial Department of Energy loan guarantee program, which was completed by an independent consultant.

The Report of the Independent Consultant’s Review with Respect to the Department of Energy Loan and Loan Guarantee Portfolio was led by Republican Herb Allison, whose conservative credentials include a stint as national finance chairman for then-presidential-candidate Senator John McCain (R-AZ), as well as time at the Treasury Department and with Merrill Lynch. He was appointed to lead the review by President Obama.

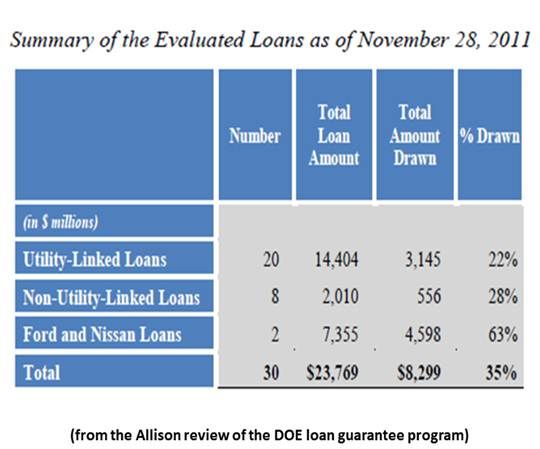

The review assessed the 30 U.S. Department of Energy (DOE) “Evaluated Loans” as of November 28, 2011, in “three broad categories,” each with “a distinctive project type and loan structure.” The total amount involved, the review found, was $23.77 billion. But the loans “were structured as funding commitments, with limited or, in many cases, no funds drawn under the loans at closing.” Only 35 percent of the total amount was actually drawn.

The important point about the drawn amount, the review pointed out, is that it shows how carefully the taxpayer was protected when the loan programs were set up. “DOE will,” the review pointed out, have further opportunities “to protect itself against taking on elective risk” as the projects to which the money was committed unfold.

Twenty “Utility-Linked Loans” supported “projects for the generation or transmission” of renewable (solar, wind and geothermal) energy sources and came to $14.4 billion. Only 22 percent of this amount was drawn down.

Eight “Non-Utility-Linked Loans” supported “cellulosic ethanol projects, solar manufacturing companies, and small, startup automotive manufacturing companies.” These were smaller-amount, higher-risk loans which came to just over $2 billion. A total of 28 percent of this was drawn.

Solyndra Inc. and Beacon Power Corporation fell into this second category. These two firms are in bankruptcy and represent a total of $567 million.

Two loans totaling $7.35 billion went to Ford Motor Company and Nissan North America, both of which had established corporate credit and got “structures typical of traditional secured corporate loans.” A total of 63 percent of this money was drawn.

The review found the overall “creditworthiness” of the loans in the first category to be modestly lower than did the DOE, the overall “creditworthiness” of the loans in the second category to be lower than did the DOE, and the overall “creditworthiness” of the loans in the third category, which accounted for a third of the total amount, to be higher than did the DOE.

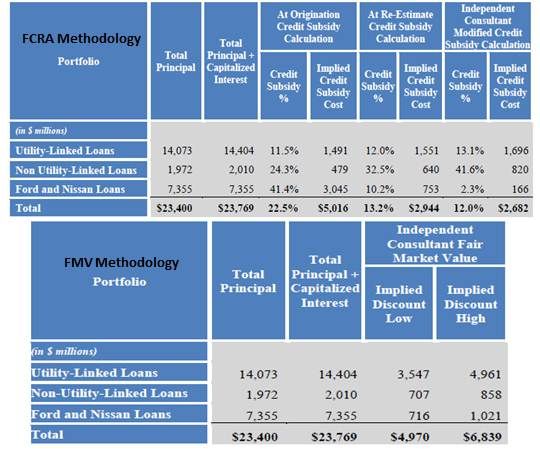

Controversy about this review of the loan guarantees may eventually settle on the fact that it used two methodologies with “distinctly different purposes” and, therefore, came up with some divergent impressions.

An “FCRA Methodology” came from the Federal Credit Reform Act (FCRA) of 1990. With it, a “Credit Subsidy Cost” was estimated by the DOE for each loan that reflected the DOE’s assessment of that loan’s credit quality.

The review’s “FMV Methodology” is used by capital markets to estimate the “fair market value” of the loan, the price at which investors would get an acceptable rate of return. It is based on market data for the most comparable bonds and loans. But it considers market risks that do not necessarily apply to government investments.

Both methods, the review noted, are useful, and neither predicts the future more effectively than the other.

According to the review, the DOE’s latest estimate of the subsidy provided is $2.9 billion, down from what a number of sources report was an initial $5 billion estimate by the DOE. The review, using the FCRA Method, found the subsidy to be $2.7 billion. That is a distinctly lower risk to the taxpayer and undercuts some of the criticisms that have been advanced by opponents of the program.

The FMV Method, which considers risk that probably does not apply for government loans, found the subsidy to have an “aggregate par value ranging from $5.0 billion to $6.8 billion.” Because that range exceeds the DOE’s initial estimate of risk, it could be used to criticize the program.

The review did not judge future performance, and the bulk of it consists of suggestions for improved management. “The ultimate performance of the Portfolio,” the review noted, depends on the “DOE’s management of it going forward.” It called on the department to “be an active manager continuously monitoring the projects, their market environments, and other identified risks” and to seize “opportunities to contain taxpayers’ exposure to loss.”

In its neutrality, the review left itself open to interpretation -- and those interpretations have started coming in.

“This is less a report than an umbrella to deflect the criticism that’s pouring down on the administration,” Rep. James Sensenbrenner Jr. (R-Wis.) was quoted as saying in The Hill.

“The report is a repudiation of the partisan attack on the program by congressional Republicans and the oil and coal industries,” said Rep. Henry Waxman (D-Calif.), Ranking Member on the House Energy Committee, according to The Hill.

"DOE's loan program is generating $40 billion in private investment in America’s economy that is supporting 60,000 direct jobs and many thousands more up and down the supply chain,” DOE Secretary Steven Chu’s statement said. "We have always known that there were inherent risks in backing innovative technologies at full commercial scale, and it is very likely that there will be other companies in the portfolio that won’t succeed, but the vast majority of companies are expected to pay the loans back in full, on time, and with about $8 billion in interest.”

41

41

15

15

9

9