California’s investor-owned utilities (IOUs) asked state regulators to approve small Return on Equity (ROE) decreases for the period 2013-2016 that will, according to the state’s Division of Ratepayer Advocates (DRA), redirect hundreds of millions of dollars too little from the utilities’ stockholders.

Interest rates and other capital costs are presently significantly lower than they were when the California Public Utilities Commission (CPUC) in 2007 put the Pacific Gas and Electric (PG&E) ROE at 11.35 percent, the Southern California Edison (SCE) ROE at 11.50 percent and the San Diego Gas and Electric (SDG&E) ROE at 11.1 percent. After extensions during the recession, those determinations expire December 31.

The PG&E requested ROE reduction to 11.0 percent, the SCE requested reduction to 11.1 percent, and the SDG&E requested reduction to 11.0 percent “far exceed the companies’ revenue needs and market standards,” according to Acting DRA Director Joe Como.

SCE’s request “is reasonable compared to other jurisdictions when adjusted for risk and leverage,” asserted SCE spokesperson Lauren Bartlett. “The proposal would lower requested customer rates by more than $120 million.”

DRA is asking the CPUC to limit the PG&E and SCE ROEs to 8.75 percent and the SDG&E ROE to 8.50 percent. The differences between the requested ROEs and the DRA recommended rates, according to DRA regulatory analyst Jerry Oh, are $377 million for PG&E, $211 million for SCE, and $50 million for SDG&E.

The IOUs, Como said, “should be passing those tens of millions of dollars in savings on to their customers.”

Setting the ROEs accurately requires determining how much above or below the return on alternative investments the IOUs should provide their shareholders. The higher the return they offer, the more capital investment they can attract.

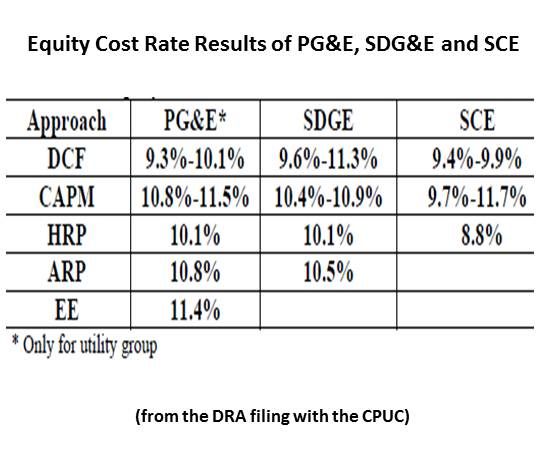

Setting the ROEs accurately begins, Oh said, with the sophisticated mathematics of three basic financial models, the Discounted Cash Flow (DCF) model, the Capital Asset Pricing (CAP) model and the Historical Risk Premium (HRP) model.

Those models make assumptions, Oh explained. Pivotally, assumptions are used in (1) selecting comparable groups of utilities, (2) calculating the anticipated growth of alternative investments and (3) estimating the risk associated utility investments versus the risk of alternative investments.

The DRA’s CPUC filing, authored by Pennsylvania State University Professor of Finance J. Randall Woolridge, found the utilities’ modeling flawed in three broad ways: They selected comparable groups of utilities with above average yields, they assumed overly optimistic growth from alternative investments, and they overestimated the degree of risk to their shareholders.

The IOUs’ filings with the CPUC to date do not deny Woolridge’s conclusions, though further rebuttals are expected by the end of August. Instead, they have argued, the larger factors are used because they need more money than other U.S. utilities and must therefore offer higher ROEs.

Optimistic projections for alternative investment returns were purposely chosen, for instance, because they increase what the IOUs can offer investors.

“We believe a return on equity of 11.0 percent is warranted under current market conditions,” PG&E External Communications Chief Jonathan Marshall emailed. “Our request would reduce our annual revenues by about $100 million (other things being equal). Although our proposed ROE is a little higher than for other comparable utilities across the country, that’s justified by the extra risk premium many investors see for doing business in California.”

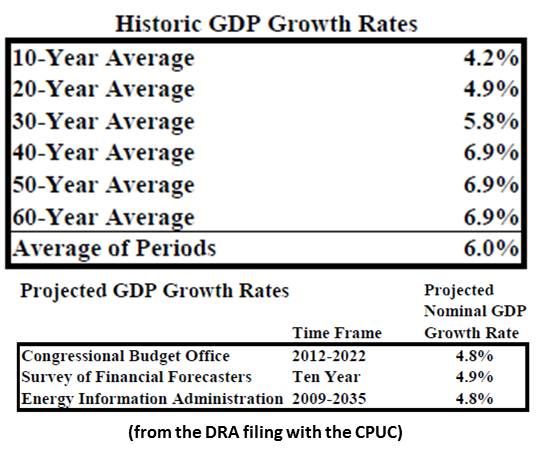

Historic long-run growth rates for GDP and the S&P 500 “are in the 5 percent to 7 percent range,” Professor Woolridge noted, whereas PG&E’s “long-run growth rate projection of 10.9 percent is vastly overstated.” Recent trends, Woolridge added, suggest economic growth “in the range of 4 percent to 5 percent.”

“SCE’s unprecedented capital investments to meet state and federal policy mandates and goals, replace aging infrastructure, modernize meters and support new renewable electric sources with vast new transmission projects have significantly increased SCE’s business risk,” explained the filing, which was authored by SCE Director of Regulatory Finance and Economics Dr. Paul T. Hunt. SCE’s long-term power contracts for conventional and renewable resources, he added, “are perceived by the financial community to be debt equivalents that must be supported by equity earning a compensatory return.”

“Our request actually protects customer interests,” PG&E’s Marshall added. “We are looking at raising about $8 billion in debt and equity markets from 2012-14 for infrastructure upgrades, repairs, and facilities to meet load growth. With a credit rating of only BBB, we have no cushion against negative surprises.”

All changes in economic markets, interest rates, and IOU infrastructure and capital needs will be considered by the CPUC in a process of hearings and counter-filings that will begin in September, Oh said. And the Commission will not only be limited to an evaluation of the numbers, but must also reconcile IOU needs, shareholder needs and ratepayer needs.

SCE is burdened, potentially severely, by the loss of the 2,300-megawatt San Onofre Nuclear Generating Station, of which it is a 78-percent owner. SDG&E, which owns 20 percent of San Onofre, has incurred the expense of hurrying the 1,000-megawatt-capacity Sunrise Powerlink transmission system on-line to help relieve the loss of the nuclear plant. And PG&E is still struggling to cope with liability losses and replacement costs associated with the 2010 San Bruno natural gas line explosion.

It may be that the question the CPUC must ultimately decide is whether the IOUs’ shareholders or ratepayers must bear those burdens.

41

41

15

15

9

9