The amount of money a company needs to spend in order to sell a residential solar system continues to be a major challenge for the solar industry.

In fact, the cost for an installer to acquire a residential customer in the U.S. has actually risen, even while the cost of every other component in the cost stack has plunged. Customer acquisition includes all costs to obtain leads, as well as all sales and marketing costs related to closing a sale.

GTM Research expects a 27 percent drop in average global project prices by 2022. The fall will come from declining module costs, as well as reductions in inverter, tracker and even labor costs.

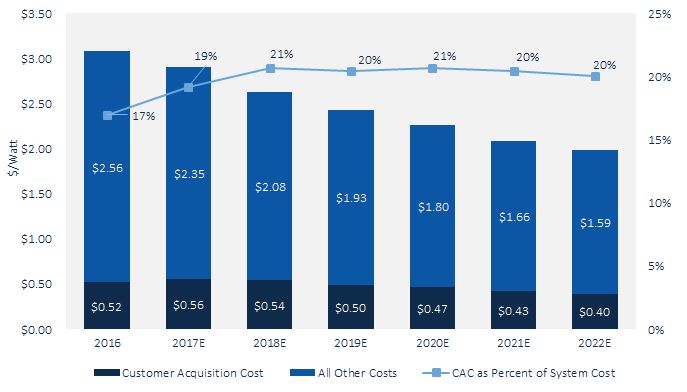

Meanwhile, customer acquisition costs have grown over the past few years -- increasing from $0.41 per watt in 2013 (or $2,870 per customer based for a 7-kilowatt system) to $0.52 per watt in 2016 ($3,668 per customer). Costs are expected to rise again this year (to a total of $3,898 per customer).

These stats are from a recently published report written by GTM Research Solar Analyst Allison Mond, the author of U.S. Residential Solar PV Customer Acquisition 2017: Current and Projected Costs and Channel Strategies.

By Mond's calculation, the average cost of acquiring a solar customer currently represents a disproportionate 17 percent of the total system cost. Furthermore, while customer acquisition costs are set to fall to $0.40 cents per watt in the forecast's out years, this slice will actually grow to 20 percent of the residential system's $2.00-per-watt cost.

How do these numbers stack up against customer acquisition costs in another industry? Only 4 percent of the purchase price of a car is used to cover sales and marketing, according to a recent article from Attila Toth, the CEO of PowerScout.

Current and Projected Customer Acquisition and Total System Costs, 2016-2022E

Source: GTM Research (the percentages on this chart have been updated)

How do you trim customer acquisition costs?

Mond attributes some of the rise in customer acquisition costs to the intense competition that makes installers "spend more money to win a bid." Other contributors include higher wages for salespeople, increased hiring in marketing departments, "and a decrease in close rates for popular strategies such as purchased leads and canvassing."

Two big factors are at work here.

First of all, the revenge of the long tail is real. Smaller installers rely more on referrals and spend less on gaining customers. At the same time, they tend to benefit from the marketing efforts of the larger players.

The GTM Research report finds that leading installers SolarCity, Vivint Solar and Sunrun average $0.70 per watt versus $0.28 to $0.36 per watt for smaller local players. In the first quarter of 2016, SolarCity and Sunrun saw their customer acquisition costs rise to 90 cents per watt.

Secondly, the industry is undergoing a shift in lead generation strategies -- with a move away from purchased leads, less reliance on door-to-door sales, and even a decrease in the percentage of customers coming from referrals.

Mond sees installers being "forced to pursue other sales tactics."

Tesla is starting to sell its solar systems in Tesla vehicle stores, and its success (or failure) in doing so will be a model for other companies to follow, according to Mond. Vivint Solar, while still primarily selling door-to-door, will soon begin to sell systems at retail locations.

With Tesla and other firms backing away from their canvassing efforts, Mond observes "the adoption of less aggressive sales tactics." The report suggests that online bidding platforms such as PowerScout and EnergySage will continue to grow as costs drop and consumers become more comfortable shopping for solar on the internet.

It costs a lot to run a public, multi-state installer, marketing, permitting, regulatory and finance operation. Can the big public solar installers ever get their customer acquisition costs down? Or is that cost piece destined to polarize -- with Tesla, Sunrun and Vivint stuck at high rates, while the smaller installers gain a cost advantage based on cheaper acquisition costs?

A group of early-stage and VC-backed solar software companies are confronting the largely American problem of disproportionate solar soft costs, or at least attempting to. Here's a list of companies GTM has covered in the past:

- Folsom Labs, a solar design and optimization startup directed at process flow in commercial solar projects. Investors include Sheldon Kimber, former COO of Recurrent Energy, and Tim Ball, founder of REC Solar.

- Startup Geostellar won $7 million in financing led by Dallas-based venture firm Matador Capital Partners to lower acquisition costs via an online platform that lets residents model the value of a rooftop solar system at a specific location.

- Sighten landed a $3.5 million Round A of venture funding from Obvious Ventures late last year. Sighten's platform looks to drive down soft costs by addressing the "solar lifecycle, from sales to asset management."

- EnergySage is positioning itself as the Expedia.com of solar. The startup has built an online service that lets customers compare quotes from hundreds of solar installers. Pick My Solar offers a similar purchasing marketplace, along with financing, customer advocacy and maintenance.

- Energy Toolbase is a software proposal platform for modeling the economics of solar and energy storage projects.

- Open Energy is trying to make financing commercial-scale PV projects easier through an online service built to mimic applications for consumer debt.

- UtilityAPI, as GTM has reported, is taking on "another choke point in the solar customer acquisition process -- the cumbersome process of getting utilities to cough up their customers’ energy usage and billing data."

- Aurora Solar is developing solar sales and design software.

- Other firms in the rooftop solar sales and design software business include SolarNexus, MODsolar and ENACT Systems.

- SunShot grant awardees and other firms focused on soft-cost reduction and asset performance include EnergyBin, Faraday, Amplify Energy, kWh Analytics, Also Energy, Clean Energy Experts, concept3D and Urban Glue.

***

GTM Research's latest residential solar report is U.S. Residential Solar PV Customer Acquisition 2017: Current and Projected Costs and Channel Strategies. More details here.

41

41

15

15

9

9