Say what you will about California, but it’s undeniable that the state has been a leader when it comes to transportation and vehicle policy. In the domain of electric vehicles (EVs), in particular, California is showing the rest of the country the art of the possible. Sales of EVs in California exceeded 100,000 earlier this year, and the state is well on its way to doubling that figure.

The center of the action on EVs is, perhaps surprisingly, the California Public Utilities Commission. I say “surprisingly” because normally on this kind of issue, the legislature in Sacramento would be calling the shots. In this case, however, lawmakers have granted a large amount of discretion to the CPUC (as they also did with energy storage legislation), allowing it to determine its preferred policy.

The regulated utilities -- the big three of Pacific Gas & Electric, Southern California Edison, and San Diego Gas & Electric -- have also been stepping up recently with their own proposals for kickstarting the EV revolution.

SB 626, passed in 2009, directed the CPUC to “evaluate policies to develop infrastructure sufficient to overcome any barriers to the widespread deployment and use of plug-in hybrid and electric vehicles.” And that’s about all the law directed. The CPUC did act on this law by the required July 2011 deadline by issuing the first in a string of major decisions (this is how the CPUC promulgates regulations).

The governor also got into the game in a big way in 2012 by issuing an executive order that set forth a number of mandates for the CPUC and other state agencies to implement. Even though the CPUC is an independent agency, Governor Brown still believes that he can set policy, and he did set many major policies in his 2012 order, including requiring that by 2015, all major cities in the state be EV-ready, and that by 2020, California must have sufficient charging infrastructure for up to 1 million EVs and by 2025 for at least 1.5 million EVs and fuel-cell vehicles (collectively referred to as “zero-emission vehicles” or ZEVs) to be on the road.

The big news recently, however, comes from Southern California Edison. SCE recently submitted an application to the CPUC to develop the infrastructure for up to 30,000 EV charging stations in the next few years. SCE will develop the required distribution lines, transformers, and other infrastructure and also provide rebates of up to $3,900 for third parties to own the EV chargers. This is known as a “make-ready” approach because it relies on the utility making the infrastructure ready for third parties to build out the charging stations themselves.

The price tag for SCE’s proposed program is about $350 million, to be paid for with ratepayer funds. This is not chump change, but SCE has asserted that its program will be cost-effective for ratepayers. While we need a lot more evidence to firm up this conclusion, my feeling is that we know enough from many similar analyses to feel pretty confident that SCE is right on this. The key savings from EVs come from the fuel savings, simply because running cars on electricity rather than petroleum is so much more efficient (EVs are 2.5 to 3 times more efficient than gasoline vehicles in terms of energy used).

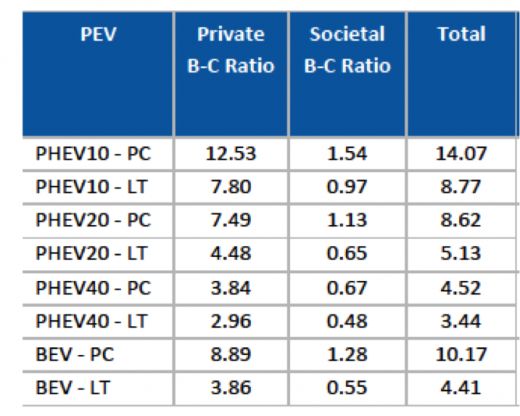

Investments in EV infrastructure are a highly cost-effective proposition for ratepayers and taxpayers because EV transportation is so much more efficient and thus cheaper than fossil-fuel-based transportation. The Transportation Electrification Assessment, a report from ICF International that SCE cites in its application, calculates the costs and benefits for various scenarios, as summarized in Figure 1.

FIGURE: Cost-Effectiveness of EVs

Source: ICF International

A “B-C Ratio” greater than 1 means that there are positive net benefits. Every scenario examined has a benefit-cost ratio over 3, which means that benefits outweigh the quantified costs by at least a factor of 3 for all vehicle types examined. This is a very encouraging result in terms of the ability of EVs to produce net economic benefits for ratepayers and taxpayers.

SCE is asking the CPUC to approve its major new program in two phases. Phase 1 will be a $22 million, one-year pilot to test the concept. Phase 2 will cost more than $300 million and will take four years to complete. The point of SCE’s program is to help California achieve the governor’s 1.5 million ZEV mandate by 2025. This is a big lift, even with California already at 100,000 EVs on the road today. We’ll need a lot more infrastructure to instill confidence in mainstream consumers that they will be able to charge their EVs when and where they want to.

SCE’s focus is on “long-dwell-time” locations like apartments and workplaces. This is the case because SCE sees an opportunity to install numerous Level 1 and 2 chargers at these locations that will allow EV owners to charge up while they’re working or doing whatever they do at home. DC fast chargers aren’t included in SCE’s proposal because SCE feels that the market for these types of chargers is growing adequately on its own.

SDG&E has already submitted a similar, but much smaller, application to install up to 5,500 chargers in its service territory. SDG&E’s application is not as clear as SCE’s in terms of who will own the charging stations themselves, but it is likely that the CPUC will approve (if it does approve these programs) SDG&E’s program in a manner similar to what SCE has proposed: the “make-ready” approach that allows the utility to own everything up to the charging station and to allow third parties to own the actual charging units.

PG&E has not yet submitted an application, but it is almost certain that it will do so later this year or early next year. We can anticipate a similar “make-ready” approach from PG&E.

Business opportunities in the EV charger space

These major new programs provide significant opportunities for third parties to create viable business models. SCE’s proposed rebate per charger of up to $3,900 means that third parties seeking to own EV charging stations in long-dwell-time locations will probably pay nothing, or very little, for these stations. If this is the case, it means that the major costs will be the property lease or property purchase cost and the cost of power bought from the IOU for resale to EV owners.

The revenue options for long-dwell-time charging locations are not as diverse as for charging stations focused on shorter dwell-times, which will generally include DC fast chargers (which can charge some vehicles 80 percent in just 20 minutes, as opposed to four hours or so for Level 2 chargers and far longer for Level 1 chargers). For long-dwell-time locations, charging stations located in workplaces or multiple unit dwellings may offer charging for free as a perk of working or living at that location. Alternatively, monthly subscriptions could be offered for unlimited charging.

The new IOU programs may allow some DC fast chargers to be included at the long-dwell-time locations, in which case there could be higher revenue potential due to faster turnaround.

What does the future hold?

SCE’s application makes the case for its proposed ratepayer funding based on the governor’s mandates for EVs, including the 2025 mandate of being able to support at least 1.5 million zero-emission vehicles on the road. Given the binding nature of SB 626 and the governor’s ZEV executive order, plus the fact that promoting EV adoption through better EV charging infrastructure is a clear economic winner for ratepayers and taxpayers, it seems likely that the CPUC will approve the IOU applications for EV ownership, at least in some form.

If this does happen, we’ll have a much better chance of meeting the 2025 mandate of 1.5 million zero-emission vehicles. I recently took the plunge and bought an all-electric Fiat 500e. I can now speak from personal experience about the features and benefits of EVs, and I think the combination of excellent driving features, amazing fuel economy (my Fiat gets the equivalent of 115 mpg), and low cost of driving will catch on widely in the coming years, particularly as battery costs continue to fall rapidly with scale.

My feeling, which isn’t much more than intuition at this point, is that once we get to the scale of 1.5 million or so ZEVs on the road (the vast majority of which will be EVs), we’ll have reached critical mass, and EVs may well become the default purchase option for many new buyers, including both fleets and individual consumers. If this is the case, California’s long-term climate mitigation goals of an 80 percent reduction in greenhouse gas emissions by 2050 will become eminently achievable.

***

Tam Hunt is the owner of Community Renewable Solutions LLC, a renewable energy project development and policy advocacy firm based in Santa Barbara, California and Hilo, Hawaii.

41

41

15

15

9

9