GTM Research forecasts 21 gigawatts of PV module manufacturing capacity to come offline by 2015 as the global market reconciles a dire supply-demand imbalance. GTM’s latest report, PV Technology, Production and Cost Outlook: 2012-2016 estimates module supply to be in excess of global demand by nearly 100 percent this year, or roughly 59 gigawatts of total supply compared to 30 gigawatts of total demand. The pain is more acute when considering the greater PV supply chain, as the report forecasts wafer, cell and module manufacturers to retire a combined 60 gigawatts of capacity by 2015.

GTM’s 291-page report covering the PV wafer, cell and module market is the most granular analysis to date on the past, present and future of this maturing industry. The report includes bottom-up cost and price estimates for wafers, cells and modules, as well as competitive analysis of suppliers along a range of metrics including manufacturing capacity, cost, balance sheet strength, technology, bankability and business model. Download the report’s brochure to see the complete scope at http://www.greentechmedia.com/research/report/pv-supply-2012.

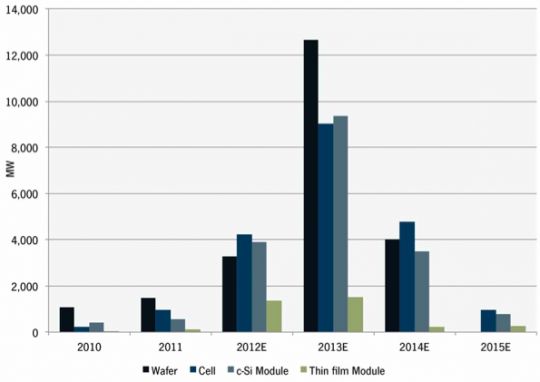

FIGURE: PV Manufacturing Capacity Retirements, 2010-2015E

Source: PV Technology, Production and Cost Outlook: 2012-2016

“The PV manufacturing industry has evolved from a period of secular growth, in which profits grew year-over-year, to a period of cyclical growth” said Shyam Mehta, Senior Analyst at GTM Research and the report’s author. “Fundamentally, this is due to the sheer magnitude of overcapacity that exists in the value chain today and the speed with which feed-in tariffs are being extinguished the world over. We are in a transitional time in the history of the market; the training wheels of subsidies are coming off, and the next few years will see the industry’s first attempt to ride without support. Consequently, the next three years will be an extremely difficult period.”

Mehta commented that aside from a select few low-cost, top-tier firms such as Yingli Green Energy and Trina Solar that can attain manufacturing costs of $0.45 per watt by 2015 and sustained profitability, module suppliers cannot expect to attain financial success by selling commoditized “plain-vanilla” modules. This is due to the intense level of overcapacity and consequent compressed pricing outlook over the next few years.

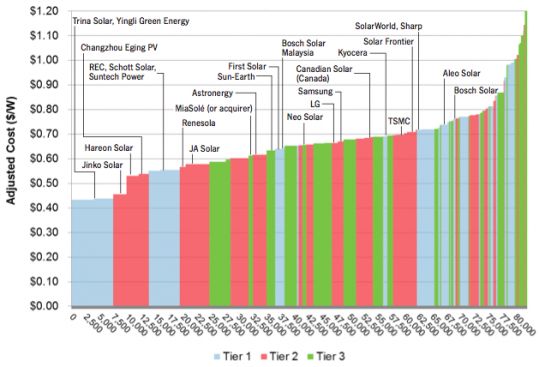

FIGURE: Efficiency/Performance-Adjusted Module Supply Stack, 2015E

Source: PV Technology, Production and Cost Outlook: 2012-2016

“Most current PV manufacturers will have to take a long, hard look in the mirror and make tough decisions about their future role in the industry,” said Mehta. “They can either exit gracefully, or continue as producers in the undifferentiated component market where they have no inherent advantage, or take risks in terms of their business, technology and product models, knowing full well these moves could also end in failure.”

Report Highlights

- PV supply to be nearly 200 percent of demand in 2012, or 59 gigawatts of supply compared to 30 gigawatts of demand.

- Estimated 21 gigawatts of existing module manufacturing capacity to come offline by 2015.

- Crystalline silicon (c-Si) module manufacturing costs to fall as low as $0.45 per watt by 2015 for Chinese Tier-1 suppliers.

- c-Si module average selling price (ASP) to dip to $0.61 per watt by 2015 from Chinese Tier-1 suppliers.

- Average c-Si module efficiency to hit 16.4 percent by 2015 compared to 14.9 percent today.

For more information on this report and the state of the PV supply market, visit http://www.greentechmedia.com/research/report/pv-supply-2012.

41

41

15

15

9

9