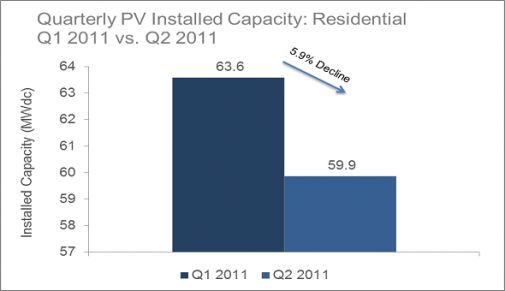

According to GTM Research and the Solar Energy Industries Association's latest quarterly U.S. Solar Market Insight report, installations in the U.S. residential PV market during the second quarter of 2011 fell 5.9 percent to 59.9 megawatts, down from 63.6 megawatts in the first quarter.

Though this trend is disappointing, it is not predictive for the residential segment. The residential market has historically been the least volatile sector in the U.S. PV market.

Source: GTM Research, Q2 U.S. Solar Market Insight Report

Residential installers tend to focus on installation volume and are less able to shift allocation of projects based on prevailing market conditions. While large commercial installers may delay installations in order to take advantage of decreased module prices, residential installers look to run at full steam if projects are available.

Therefore, the residential market rarely experiences the drastic quarterly shifts that may be present in other segments.

Still, the current decline marks the second negative growth quarter in a row for the residential market. This change has been influenced mainly by downward installation trends in Colorado, New Jersey, New York and Pennsylvania. Apart from these four, most state markets were virtually flat over the first quarter.

Looking forward, the availability of residential third-party financing will positively affect the residential market. Through this model, the homeowner pays for the PV system through a Power Purchase Agreement (PPA) or lease structure. Third-party financing offers an economic benefit to residential customers, removing the barrier of the system’s upfront cost and offering the potential for long-term savings on electricity.

As more firms adopt this model, the residential market is expected to resume its growth in future quarters.

41

41

15

15

9

9