High electricity costs (both wholesale and retail), rumors of government tenders, and significant price declines of photovoltaic equipment have attracted a rush of solar development in Latin America and the Caribbean. At the start of 2013, more than 10 gigawatts of large-scale projects have been announced in the region, but just 91 megawatts are currently operating. While 766 megawatts have signed offtake agreements in place, much of the remaining pipeline is highly speculative. Depending on the country, developers are waiting either on interest from large industrial offtakers or for governments to announce solar-specific energy auctions, neither of which has yet to materialize in a meaningful way.

To date, little grid-connected solar has been installed in Latin America, and the industry in these countries is primarily composed of distributors serving the off-grid market. This lack of domestic competition is seen by developers and component manufacturers as an opportunity to be a first-mover in markets with tremendous growth potential. While there are few pure-play solar companies operating in these countries, there are incumbent firms that operate in similar industries that could easily transition into the solar space. As some foreign entrants have already discovered, local knowledge has proven far more valuable than solar-specific experience when operating in these new markets.

In the near term, Chile, Mexico, and Brazil have the most potential for growth, but there has also been development in other markets such as Peru, Ecuador, and some Caribbean island nations. While each national market differs in energy policy, generation resources, and economic strength, they all share some, if not all, of the following characteristics: significant solar resources, high electricity prices, and growing electricity demand.

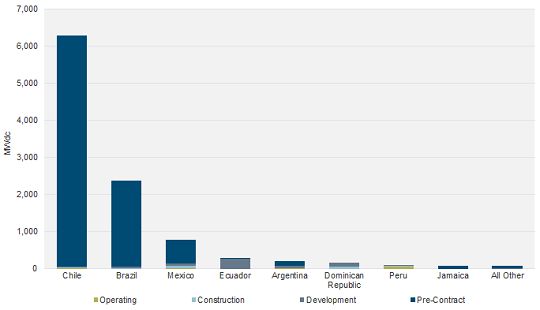

Large-Scale Project Pipeline by Country

Source: GTM Research

Chile has the largest solar project pipeline, with more than six gigawatts of projects announced. Of this, just 10.8 megawatts are currently operating with a further 22 megawatts under construction. On the surface, Chile seems ripe for solar development. The country is in desperate need of new generation, certain regions have some of the highest rates of solar irradiation in the world, the economy is one of the strongest in South America, the government has set renewable energy targets that must be met by the country’s generators, and solar generation is already competitive with wholesale pricing in some instances.

Despite these favorable conditions, significant barriers to development remain, including the complex electricity market structure, hesitancy on the part of large offtakers, and, subsequently, a lack of financing. Many of the announced projects are in the tens or even hundreds of megawatts, but those that have been completed or are under construction are all under 20 megawatts. Companies that have achieved early success in the market include Solarpack, which also connected a number of projects in Peru, juwi, Abengoa, and SunEdison, which is working with the Chilean generation company E-CL.

Brazil is another Latin American market that set the solar industry abuzz in 2012. The country’s electricity regulator, the National Agency of Electrical Energy (ANEEL), introduced new net-metering legislation in early 2012 that promised to jump-start Brazil’s solar market. Despite a flurry of media coverage, the new net-metering regulations did not take effect until December 2012. As a result, the interconnection processes with Brazil’s various distribution companies are relatively untested at this point.

Much of Brazil’s long-term growth potential lies in the distributed market, but it has not been exempt from the utility-scale solar land-grab that has occurred in other Latin American countries. More than 2.2 gigawatts of large-scale projects have already been proposed in the country. Despite this impressive figure, the largest facility slated for completion in the near future is a 3-megawatt plant being developed by a state-owned utility company. Many sub-1-megawatt projects have been announced, but these are largely to prepare for the upcoming 2014 World Cup and 2016 Olympics, as most are to be located on soccer stadiums. Without a doubt, the Brazil solar market will grow exponentially in 2013 -- but this is not a difficult feat to achieve when starting at practically nothing.

Mexico is the last of the three markets with potential for meaningful near-term growth. Unlike Chile and Brazil, in Mexico the framework for the rapid growth of solar, both distributed and utility-scale generation, is already in place. Net metering was enacted in the country in 2007 and is administered by only one entity, the Comisión Federal de Electricidad (CFE), Mexico’s state-owned electric utility. This fact alone immensely simplifies development throughout the country. With regard to utility-scale development, traditionally CFE has owned and operated most power plants in the county, but IPPs have been gaining a foothold in Mexico, especially with regard to renewables. CFE has already constructed two pilot projects -- a 1-megawatt and a 5-megawatt plant, both of which employ a number of component technologies -- and has also signed a PPA with a 46.8-megawatt project being developed by Sonora Energy Group.

In addition to Chile, Mexico, and Brazil, a number of other Central and South American markets have demonstrated some demand for solar. Most notably, Peru installed more than 60 megawatts in 2012 following a large-scale tender in 2010 and has plans for future solicitations. Island nations such as the Dominican Republic and Jamaica, which rely on costly imported fuels, could benefit hugely from both distributed and large-scale solar. However, government policies and the infrastructure to integrate solar generation are not at the point to allow for immediate or meaningful growth in these regions. That being said, these are all countries to watch in the coming years as governments become increasingly aware of the benefits of solar, and as homeowners and businesses continue looking for ways to reduce electricity consumption costs.

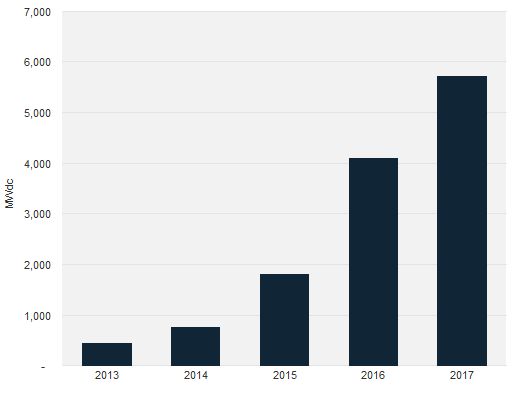

GTM Research Latin America and Caribbean Market Forecast, 2013-2017

Source: GTM Research

GTM Research predicts 66 percent annual growth in demand through 2017. In the immediate term, 2013 will be a huge growth year for Latin America as well, with an estimated 396 percent year-over-year increase in grid connected PV. In absolute terms, 2013 should yield slightly more than 450 megawatts compared to less than 100 megawatts in 2012. A majority of this will come from large utility-scale installations in Mexico and Chile. Brazil will see a number of its megawatt-scale stadium and pilot projects connected and initial growth in its distributed markets as electricity distribution companies begin to adopt interconnection and net-metering procedures. On the whole, Brazil's market will be smaller than those of Mexico and Chile in 2013 but will emerge as a leader in the region in later years. An additional 20 megawatts to 36 megawatts from two projects will come on-line in Peru, both of which stem from the country’s most recent tenders. To learn more about what is occurring in these markets, GTM Research is sponsoring a free webinar tomorrow, Friday, January 25th at 10 a.m. ET.

More in-depth individual market discussions and detailed forecasts are available in the latest report from GTM Research, Solar in Latin America and The Caribbean, 2013: Markets, Outlook & Competitive Positioning. Also available is a database of more than 200 individual large-scale projects representing more than 10 gigawatts of capacity under development in thirteen different countries in Latin America and the Caribbean.

Watch report author Andrew Krulewitz moderate a panel at Solar Summit 2013 on solar in Latin America:

41

41

15

15

9

9