Greentech Media and GTM Research have led the pack in questioning the viability of amorphous silicon in photovoltaic applications -- especially in chronicling the spectacular faceplant of Silicon Valley semiconductor giant, Applied Materials, their customers, and their a-Si photovoltaic efforts.

We've been less dismissive concerning Oerlikon's efforts in a-Si because in our many conversations with Chris O’Brien, Oerlikon Solar’s head of market development in North America, he's insisted that business is strong and that their aggressive cost targets are in reach.

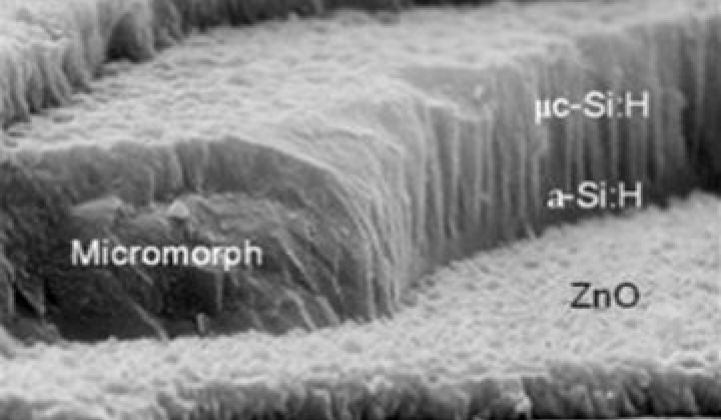

According to O'Brien, Oerlikon has some key first-mover advantages, such as possessing a longer legacy in micromorph (tandem junction) and starting off with an efficiency advantage that became much more important when crystalline silicon (c-Si) joined First Solar as cost leaders. O'Brien also cited their zinc oxide transparent conductive oxide material as an efficiency booster, as well as a new reflective coating from DuPont that allows thinner silicon layer thickness and reduces efficiency degradation.

O'Brien said that Oerlikon's cost last year was $1.30 per watt; this year's is under a dollar and 70 cents per watt is achievable by the end of the year.

Applied Materials is out of the game and Oerlikon should benefit from that exit, but Oerlikon is not competing with Applied. They (or more accurately, their customers) are competing with First Solar and a flock of low-cost c-Si companies. And Oerlikon is going to have to overachieve at execution and R&D to keep up with those pacesetters.

But Oerlikon Solar's first-half financial results were not a good sign.

Oerlikon's orders received for the first half of 2010 were down 98 percent (!) since the prior year, with operating losses of $57.5 million.

But according to the report, "in recent months the solar market has also shown signs of recovery, and Oerlikon Solar won two follow-up contracts from its Chinese customers Tianwei and Astronergy, which were announced in July and August, respectively. In the second half-year 2010, Oerlikon Solar expects to significantly reduce its losses."

Oerlikon Solar, based in Zurich, Switzerland and controlled by Russian tycoon Viktor Vekselberg, is one of the world’s largest suppliers of equipment for building thin-film photovoltaics. The firm has not been profitable since 2007.

O'Brien was quoted in Recharge as saying, “Obviously, there’s been a big change in price expectations in the market, so getting to $0.70 [per watt] has gone from an aspiration to a real imperative."

Other Amorphous Silicon Players

Sharp is going full-speed-ahead with amorphous silicon and recently embarked on a joint venture with Enel and ST Microelectronics in a-Si. Chinese a-Si manufacturer Trony Solar withdrew its IPO earlier this month. Trony's investors include Intel, which owns about 5 percent of the firm.

Also struggling to remain competitive in amorphous silicon are flexible panel vendors Energy Conversion Devices and relatively quiet VC-funded Xunlight. Other startups investigating variations of amorphous silicon include AOS Solar, APSTL, EPV Solar, HelioSphera, NanoPV, Sencera, Sierra Solar, Signet Solar and Skypoint.

All of this action takes place against the backdrop of thin film leader First Solar, soon to have 2 gigawatts of 14 percent efficiency solar module capacity at a cost of less than 65 cents per watt.

I'll leave you with a quote from Chet Farris, the CEO of CIGS PV vendor, Stion, who had this to say about amorphous silicon: it was a "dead duck ten years ago" and "is a dead duck today." It will be "relegated to specialty and niche markets."

Potential amorphous silicon photovoltaic market:

41

41

15

15

9

9