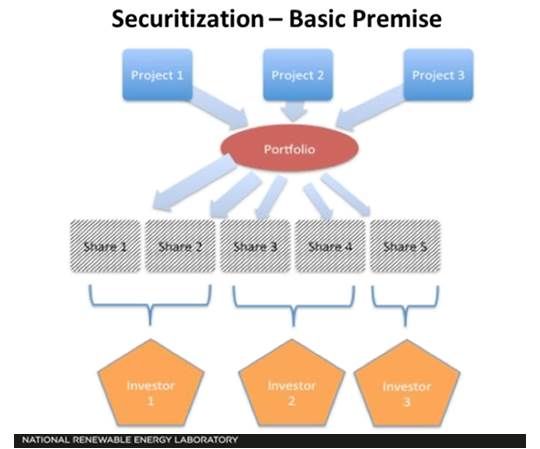

“Securitization,” explained GTM Research VP Shayle Kann, “is taking a portfolio of contracted revenue from solar [or wind] projects, bundling it, and selling it as individual securities.”

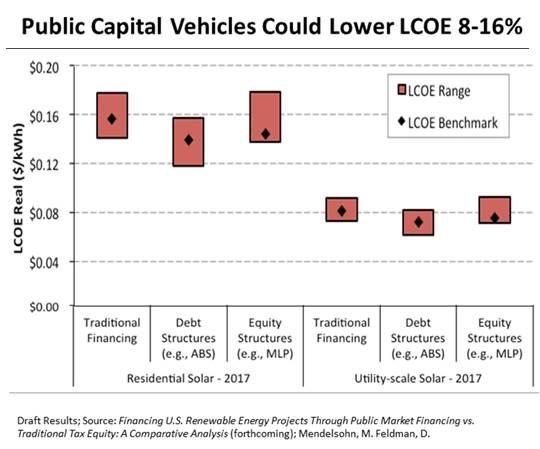

In addition to providing a new source of capital, securitization could also lower the levelized cost of energy (LCOE) of best-quality solar projects up to 16 percent, according to a new report from NREL.

Michael Mendelsohn’s report on the early progress of U.S. Department of Energy (DOE)-funded research on opening up solar to public investment through securitization showed it could lower the levelized cost of solar energy-generated electricity by 8 percent to 16 percent for the best quality projects.

Another measure of the potential rewards from securitization is the prestigious list of participants in the NREL Solar Access to Public Capital (SAPC) working group, which is a renewables industry who’s who of major banks (Bank of America Merrill Lynch, Rabobank); venture capital firms (Capital Fusion Partners, CleanPath Ventures); law firms (Bingham McCutchen LLP, Chadbourne & Parke LLP); ratings agencies (Standard and Poor's, Kroll Bond Ratings); and, especially, solar financiers (Clean Power Finance, Sungevity, SunPower [NASDAQ:SPWR], Sunrun).

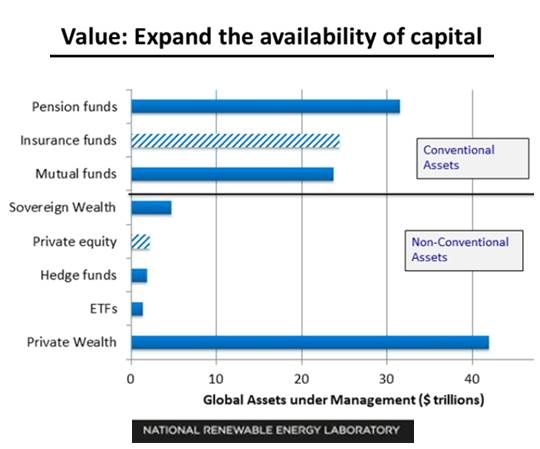

Based on DOE-established targets, the solar and wind energy industries’ need for capital will double and approach $70 billion by 2020. This will greatly exceed what is likely to be available, especially because most industry observers expect that the tax credits that bring equity investment into solar and wind will no longer be available.

The working group’s aim is to establish the viability of asset-back securities, real estate investment trusts (REITs), and master limited partnerships (MLPs) and other public investment vehicles.

Mendelsohn, NREL’s SAPC lead, reported that the working group found those vehicles would allow institutional investors, who hold or have access to more than adequate ready capital, to buy into renewables. Recent assessments by Credit Suisse (NYSE:CS) and Standard & Poor’s and a study by the Climate Policy Initiative reinforce the NREL working group’s conclusion.

To head off concerns that securitization in the renewables, especially solar, would blow up the market as it did in the housing sector in 2008, NREL’s SAPC working group’s DOE grant charged it with a three-year, three-task purpose:

- Simplify investors' due diligence by standardizing evaluation, legal practices, and documents necessary for securitization of renewables investments;

- Evaluate securitization in other economic sectors. Identify the strengths and flaws in assumptions and proposals about how pooling project shares would work for the renewables; and

- Collect data for the evaluation of securitization’s potential performance and credit default risk.

The key qualities investors will want in renewables securities are market pricing, liquidity, tradability, and transparency of their risk in relation to other market vehicles.

As noted recently by Shayle Kann and solar sector investment professionals, the first solar asset-backed securities (SABS) will be in the booming residential solar third-party ownership (TPO) business where, according to Clean Power Finance CEO Nat Kreamer, secure leases may offer a potential cumulative $2 billion or more.

Lease payments would be pooled and divided into tranches of SABS. Eventually, Mendelsohn reported, ratings agencies would prioritize the quality of those tranches just like other investments, from AAA to BB and unrated.

41

41

15

15

9

9