Below is an excerpt from GTM Research's latest solar market report, The Global PV Inverter Landscape 2013: Technologies, Markets, and Survivors. For more information on this research, click here.

The uptick in microinverter and DC optimizer adoption, rising from just 51 megawatts in 2009 to over 785 megawatts in 2012, has drawn the industry's attention, along with speculation about the root causes of this interest. While much of the adoption has come from residential PV systems, small and large commercial applications are joining the fray, as well.

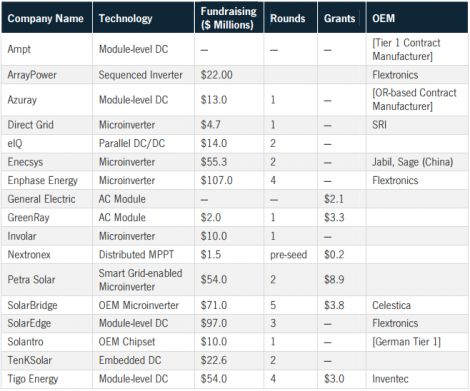

In addition, new players are cropping up every day, with significant venture or private backing. At the end of 2012, the module-level power electronics market had been fueled by over $600 million of venture and public capital -- not including internal corporate development -- even though it still accounts for a tiny 2.5 percent of the overall PV inverter market. While the growth of the space has surpassed expectations, important questions regarding the long-term growth prospects of the market and the various technologies serving it still remain.

FIGURE: Major Investments in Module-Level Power Electronics Companies

Source: The Global PV Inverter Landscape 2013

While Enphase Energy has popularized the standalone distributed optimization unit, the space is littered with companies seeking alternative paths to market adoption. On one side, inverter vendors offer standalone and non-differentiated microinverters and DC optimizers as another product in their suite of offerings to developers, distributors and integrators.

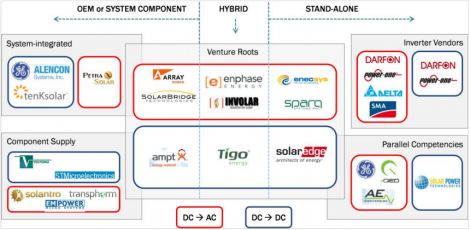

On the other side of the spectrum, companies like SolarBridge seek to provide only to strategic players, such as module vendors. While hybrid (offering both OEM and standalone products) vendors like Enphase Energy and SolarEdge Technologies currently dominate the distributed optimization space, the advantage is more due to early entrance. Long-term, the market will likely be filled with a mixture of all market approaches, with the strength of standalone vendors determined by the robustness of their distribution channels and the success of the OEM model predicated on the strength of their module or junction box partners.

FIGURE: Module-Level Power Electronics (MLPE) Taxonomy

Source: The Global PV Inverter Landscape 2013

While there are numerous companies attacking the module-level power electronics (MLPE) space, three companies (Enphase, SolarEdge and Tigo) account for over 93 percent of the total market share of shipments and installations, with Enecsys, SolarBridge, Petra Solar and others lagging much further behind. The first-mover’s advantage has allowed these players to make critical R&D and distribution partnerships and to gain significant market traction ahead of newcomers.

Prospective technologies that have neither defined a differentiated niche nor made significant gains in their relationships with module manufacturers and distributors will likely go out of business by the end of 2013. Already, we have seen many distributed optimization companies release a glut of press releases only to quickly fade. Nevertheless, new entrants continue to try the space, including much anticipated but slow-to-market products by traditional inverter market leaders SMA and Power-One.

While the field has not been completely set, the microinverter and DC optimization landscape will play out and likely begin to look like the conventional inverter landscape, where the top five companies dominate market share. In fact, given the competitiveness of the space versus the reduced market potential relative to the overall inverter market, companies outside of the leading handful may never reach the scale necessary to be viable. The prospects for the MLPE space over the long term, however, will continue to ensure that new players try their hand at the market.

GTM Research expects large inverter companies, right now focused on the frothiness of the central inverter market, to acquire or develop their own microinverter and DC optimizer technologies post-2013. However, development of the technology may not necessarily be a straightforward process, even upon acquisition. For example, SMA’s 2009 acquisition of OKE Technologies took over three years to coalesce into a concrete product offering. As a result, new business models involving OEM and white-labeled products may bolster the product suites of inverter incumbents.

To learn more about the microinverter and DC optimization market from The Global PV Inverter Landscape 2013 report, visit the report's web page at www.greentechmedia.com/research/report/the-global-pv-inverter-landscape-2013.

41

41

15

15

9

9