First, here's an updated list of the top three profitable, publicly held fuel cell firms:

1.

2.

3.

How do you assess the health of an industry? Is it whether it's growing? Profitable? Innovating? Winning market share from competing technologies?

And where does that leave the fuel cell industry?

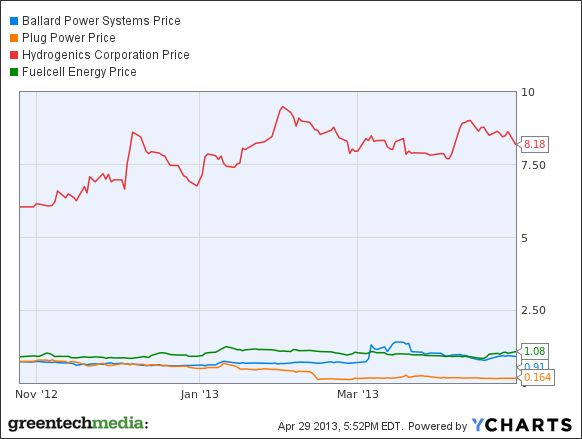

If you look at the financials of the publicly traded fuel cell firms, the story is stark. This is a lackluster, loss-filled business. It's been like that for decades.

| Firm | Market Cap | 2012 Revenue | 2012 Profit / (Loss) |

| Ballard Power (BLDP) | $76.3M | $59.2M | ($18.5M) |

| Fuel Cell Energy (FCEL) | $193.2M | $120.6M | ($38.7M) |

| Hydrogenics (HYGS) | $65.4M | $31.8M | ($12.6M) |

| Plug Power (PLUG) | $6.0M | $26.1M | ($31.9M) |

A few other fuel cell firms, such as Ceres and Ceramic Fuel Cells, are listed on lesser bourses such as the AIM or ASX. They, too, are perennial money losers.

However, the fuel cell industry is beginning to look like two markets: there's everyone else, and then there's the Bloom Energy reality distortion field.

The four public firms listed in the table above collectively earned $238 million in fuel cell revenue and lost $100 million.

On the other hand, Bloom Energy had $101 million in pro forma Q3 2012 revenue alone. And Bloom suggests it will turn a profit, according to Dan Primack of Fortune. Bloom's valuation dwarfs the collective market cap of the public fuel cell firms and its revenue is greater than the collective revenue of those firms. A Bloom board member has spoken of an IPO this year or next. (More on Bloom in a bit.)

Consolidation hit the fuel cell industry in 2012. Clear Edge acquired United Technology's fuel cell business and soon reduced its national workforce by 39 percent. Ballard Power acquired assets from IdaTech. SiGNa Chemistry acquired the hydrogen storage cartridge assets of Jadoo Power. France's McPhy Energy acquired Italian electrolysis firm PIEL. MTI fired CEO Peng Lim and withdrew from the portable fuel cell field, after investing tens of millions.

Fuel cells employ an assortment of membranes, catalysts and temperatures, but in almost all cases, the membranes are difficult and expensive to fabricate, the catalysts are rare and expensive (typically platinum or palladium), and the temperatures required in the processes are relatively high. Fuels range from natural gas to methanol to butane to hydrogen. There are ongoing efforts to reduce the need for expensive metals and to improve the reliability and lifetime of the fuel cell stack.

Leading technologies include PEM (proton exchange membrane), SOFC (solid oxide), and MCFC (molten carbonate). There are a number of other technologies, all equally adept at oxidizing investor capital. GM, Hyundai, Honda, Johnson Matthey, Panasonic, Siemens, Samsung, Sharp, Toshiba and Toyota have invested in fuel cell technology.

Here's an incomplete list of fuel cell companies.

Large Stationary Fuel Cells

Bloom Energy is suggesting that it will turn a profit in 2013. And likely go public, according to a board member.

After raising almost $1 billion in venture capital over a decade from investors including GSV Capital, Apex Venture Partners, DAG Ventures, Kleiner Perkins Caufield & Byers, Mobius Venture Capital, Madrone Capital, New Enterprise Associates, SunBridge Partners, Advanced Equities, and Goldman Sachs, this could be the year.

According to an investor letter cited by Dan Primack of Fortune, Bloom had $101 million in pro forma Q3 2012 revenue, while cost of goods was $106 million, along with $26 million in operating expenses. That's a loss of $42 million on a GAAP basis, along with a net cash loss of $80 million in the quarter. However, those Q3 numbers are hobbled by an inventory and timing issue, and cash burn dropped 56 percent between Q2 and Q3, according to Primack. The firm had a 26 percent quarter-over-quarter revenue increase.

Bloom CFO Bill Kurtz told Fortune in an official statement: "Bloom Energy is pleased with the substantial progress we have made in 2012. On a pro-forma basis, Bloom has become gross-margin-positive in 2012 and is on track with our goal to be profitable in 2013." The claim from Bloom's CFO suggests that Bloom is finally making money on every fuel cell it ships.

Bloom builds fuel cells of the solid-oxide variety with natural gas as the fuel. There is no heat resource in the Bloom Box as in other CHP fuel cells.The 200-kilowatt units are intended for commercial and industrial applications, and the firm boasts an all-star list of customers, including Adobe, FedEx, Staples, Google, Coca-Cola, and Wal-Mart.

In 2012, Bloom raised $100 million of a potential $150 million from Apex Venture Partners and an undisclosed firm. (Jeff St. John of GTM reports on Bloom's valuation and stock sales in the secondary market.)

SiliconBeat reports that Santa Clara Valley's Transportation Authority will get $750,000 in federal funds to help finance a 400-kilowatt Bloom Energy fuel cell facility at a total cost of $4 million. Using the numbers supplied, that works out to $10,000 per kilowatt, which sounds about right for a Bloom Box, although a bit high for a competitive power source.

Bloom's fuel -- natural gas -- is a commodity and subject to price increases. Bloom's business has relied on state subsidies for distributed energy, but subsidies expire. The long-term reliability of the fuel cell stack remains a risk, and some have doubted Bloom's green claims and employment practices.

But in today's difficult cleantech business climate, those profit noises from the CFO are cause for cautious optimism. If Bloom is actually profitable in 2013, the company would be a testament to the viability of capital-intensive, VC-funded cleaner energy breakthroughs and the virtue of distributed power generation.

Scott Sandell, a partner at NEA and Bloom board member, was quoted by Reuters as saying that Bloom will likely attempt an IPO late this year or early next.

Plug Power, despite having sold hundreds of fuel cell systems for forklifts, is currently trading at $0.16 and is out of compliance with Nasdaq's minimum bid price rule and faces delisting. It is also offering itself for sale

FuelCell Energy, revenue and deployment leader in the public company division, builds molten carbonate stationary fuel cell power plants located at wastewater treatment facilities, universities, pump stations and sites that need low-emission baseload distributed generation. POSCO, an investor in FuelCell, is also its largest customer. The company continues to lose money.

Ballard Power is a pioneering fuel cell firm developing PEM-based fuel cells and losing money since 1983. Ballard recently acquired assets from IdaTech. Here are the figures on Ballard's most recent losing quarter.

Small Stationary and Traction Market Fuel Cells

ClearEdge Power of Hillsboro, Oregon builds a PEM fuel cell that converts natural gas into heat and electricity for small businesses and residences. In December of last year, ClearEdge acquired fuel cell industry veteran UTC Power. UTC Power is a maker of large-scale phosphoric acid fuel cells (PAFCs), although the firm also has experience with PEM, alkaline fuel cells (AFCs), SOFCs, and MCFCs.

ClearEdge has raised more than $136 million in VC funding since its inception in 2006 with investment from Kohlberg Ventures, Applied Ventures (the investment arm of Applied Materials), Big Basin Partners, and Southern California Gas Company. According to Sustainable Business Oregon, ClearEdge employs 70 people, down from a high of 150.

ClearEdge's core product is a modular PEM going after combined heat and power (CHP) applications at hotels, multi-tenant buildings and schools, with power ranging from 5 kilowatts to 200 kilowatts. The UTC product extends the ClearEdge portfolio to larger size units.

When last we checked, a 5-kilowatt ClearEdge unit had a $56,000 list price and an installation cost ranging from $10,000 to $20,000. There is a $15,000 investment tax credit. California has a Self Generation Incentive Program (SGIP) that can return $12,500, more if biogas is employed. There is the potential to exploit the SGIP for another 20 percent if the vendor is a California supplier (the approved list is currently limited to Bloom, FlexEnergy, Calgen, and Stem). New York, New Jersey, and Connecticut also have aggressive state incentive programs.

ACAL Energy, a U.K.-based fuel-cell developer, builds platinum-free or low-platinum-content catalysts and PEM fuel cells for applications requiring more than 1 kilowatt of power. The firm has raised more than $10 million from CT Investment Partners, Rising Stars Growth Fund, NorthStar Equity Investors, Porton Capital, and Synergis Technologies. According to the firm's website, ACAL replaces "the fixed platinum catalysts on the cathode with a liquid regenerating catalyst system."

Australian firm Ceramic Fuel Cells builds SOFC-based small-scale on-site micro combined heat and power (CHP) and distributed generation units. The AIM- and ASX-listed firm lost about $12 million in the last six months of 2012 on sales of $2.6 million. Recent announcements include talk of "exploring a number of financing options," which is rarely a good sign.

CellEra, based in Israel, is developing a stationary PEM fuel cell with a design that looks to eliminate the costly platinum catalyst and replace it with transition metals. The firm targets units in the 1-kilowatt to 20-kilowatt range and received $9.2 million in equity funding from Israel's Carmel Ventures and communications giant Vodafone in late 2011. Israel Cleantech Ventures and BrainsToVentures were earlier investors. Vodafone as an investor makes sense -- CellEra looks to swap fuel cells for diesel generators in cellular tower power back-up.

AIM-listed Ceres Power of England sells a 1-kilowatt household SOFC fuel cell that will provide methane-based combined heat and power (CHP) and will take advantage of the U.K.'s micro-CHP feed-in tariff. The firm lost $7.6 million on sales of $502,000 for the last six months of 2012 and lost $23 million for the entire 2012 sales year.

Intelligent Energy of London builds PEM fuel cells for automotive, consumer, and stationary applications. The firm has raised more than $130 million from investors including Meditor European Master Fund. Losses for 2011 were $18.2 million on sales of $23.5 million.

Oorja Protonics targets the traction market with methanol fuel cells and funding from Sequoia Capital. Oorja has a customer in HySA/Catalysis of South Africa in material handling applications.

Technology Management builds a small SOFC fuel cell and has partnered with Lockheed Martin.

Other firms in this size range include Trulite (portable fuel cell generators) and PowerCell (1- to 5-kilowatt APUs).

Fuel Cells for Consumer Product Charging

A recent $25 million investment by RUSNANO in Wilmington, Mass.-based fuel cell firm Lilliputian Systems brings the firm's VC investment total to more than $150 million. Previous investors include Intel Capital, Kleiner Perkins, Atlas Venture, Fairhaven Capital, Rockport Capital, Stata Venture Partners, and Altira Group. The firm was spun out of MIT in 2001 with technology that involves a silicon "chip-based" power generator and recyclable fuel cartridges, aiming to replace batteries in smartphones, tablets, and cameras. Lilliputian has a sales channel deal with retailer Brookstone for its micro SOFC and micro-reformer on a silicon chip.

Point Source Power, a startup spun out of research conducted at Lawrence Berkeley National Labs and funded by Khosla Ventures, has devised a fuel cell for emerging markets. Potentially, consumers will be able to insert biomass into a small case, close it up and put it into a cooking pit or fire. As it heats, the biomass generates gas, which is converted into electrical power via a ceramic membrane inside the device.

Neah Power, originally venture-funded by Intel, Novellus, et al., became a public firm traded on the OTCBB via a reverse merger in 2006. The company lost $1.6 million in 2011 on sales of $0 million for its licensing model with its silicon-based fuel cell.

***

Without a doubt, there are some applications for which fuel cells make perfect sense, such as premium power for the military, remote sites, construction industry, travel, etc.

But for stationary power, fuel cells compete with the grid and diesel gen sets. And few if any fuel cell vendors, other than perhaps Bloom, have proven that they can go head-to-head with those incumbent technologies on a per-kilowatt-hour basis.

Fuel cells can be distributed and do have less emissions. Natural gas is currently cheap. But for fuel cells dependent on the natural gas grid, there's the downside of volatile prices and the sometimes less-than-green processes used to extract natural gas.

Fuel cells have benefited from state and federal subsidies, or in the case of Bloom, Delaware ratepayer bill subsidies. The justification for renewable energy subsidies is often debated in these pages. But in the case of fuel cells, even after incentives, the fuel cell is expensive compared to the grid or to a diesel gen-set.

But somehow, Bloom, by my back-of-the-envelope calculations, will have shipped around 200 megawatts of fuel cells in 2012 to a dream team of customers -- Adobe, AT&T, FedEx, eBay, Coca-Cola, etc. These folks are not philanthropic organizations -- they are looking to save money, and customers attest to a three-year ROI for the Bloom Box. How is Bloom doing this? Perhaps through a PPA structure that keeps potential O&M costs isolated from the customer.

In any case, if Bloom is real -- it will have some big lessons to teach the rest of the fuel cell industry. And if Scott Sandell of NEA is right -- we'll read about it in an SEC S-1 IPO registration in the coming quarters.

Some plush home design from Ceramic Fuel Cells

41

41

15

15

9

9