Enphase just entered into a $25 million loan agreement with a lender specializing in "rescue financing" that furnishes capital "to avoid a restructuring or insolvency."

The solar microinverter pioneer is at a crossroads. Despite helping to forge an industry for module-level power electronics and shipping 11 million microinverters, Enphase has found itself undercut on price by string inverters and SolarEdge's optimizer architecture.

Battered by continuing quarterly losses as it fights to maintain market share, Enphase is betting it all on the short-term growth of the energy storage market and its own ability to develop a next-generation microinverter that's markedly smaller, cheaper and more profitable. It's the biggest test faced by Enphase as a public company.

Special situations

As per an SEC document, Enphase entered into a $25 million secured loan and security agreement with Tennenbaum Special Situations Fund IX, with a maturity date of July 1, 2020. "The term loan provides for an interest rate per annum equal to the higher of (i) 10.25% and (ii) LIBOR plus 9.5625%, subject to a 1.0% reduction if the Company achieves minimum levels of Revenue and EBITDA[.] In addition, the Company paid a commitment fee of 3.3% of the loan amount upon closing and a closing fee of 10.0% of the loan amount."

The Tennenbaum Special Situations Fund describes its strategy this way:

We invest in companies undergoing operational, financial or industry change through both private lending activities (often referred to as rescue financing) and through secondary market purchases (which we refer to as both deep-value and distressed-for-control investing). We provide rescue financing to companies that do not have easy access to conventional capital sources and generally require capital to avoid a restructuring or insolvency. In our deep-value and distressed-for-control investing, we purchase debt in the secondary market at a discount to what we believe is its intrinsic value. These investments include 1st lien and 2nd lien loans, bonds and other debt-like instruments that may ultimately provide equity in the form of warrants, preferred or common shares or other equity rights.

This is not cheap money. Enphase just doesn't have that many choices when it comes to capital markets.

The company had total revenue of $64.1 million for the first quarter of 2016 at a GAAP gross margin of 18.3 percent, with a GAAP net loss for the quarter of $18.8 million. Enphase expects revenue for the second quarter of 2016 to be within the range of $76 million to $82 million, with gross margin within a range of 17 percent to 20 percent.

As of March 31 of this year, Enphase had cash and cash equivalents of $13 million, and with borrowings available under its revolver, and stated it could fund its operations "for at least the next 12 months."

Kris Sennesael, CFO of Enphase, told GTM, "Enphase is methodically executing an effective business strategy that was laid out last year: regaining market share by offering competitive pricing, while driving our product cost reductions. In addition, Enphase has a clear path forward developing the world’s only fully-integrated solar, storage and energy management solution.

“This strategy puts temporary pressure on our cash position, so we chose to take out a loan of a type commonly used to support the growth of a company of our size. The action gives us the cash we need as we bring our lower-cost sixth-generation microinverters to market and ensures our balance sheet is strong enough to support our future needs.”

Bold battery sales goals

Enphase is putting a lot of faith in the growth of the Australian energy storage market.

Enphase was "targeting $10 million to $20 million in sales of energy-storage systems this year largely in its first markets, Australia and New Zealand," according to a Bloomberg report from early this year.

In May, according to RenewEconomy, Enphase doubled production targets for its new modular battery storage system in Australia to "a total of 60,000 units for the 2016/17 financial year" after "an overwhelming response from consumers."

Just last week at Intersolar in San Francisco, CEO Paul Nahi told GTM's Jeff St. John, "We have preorders for 70,000 of our battery and energy management systems in Australia alone."

In fact, the first energy storage system from Enphase, a beta, was only installed last week, according to PV News. And that means Enphase has a big production ramp ahead.

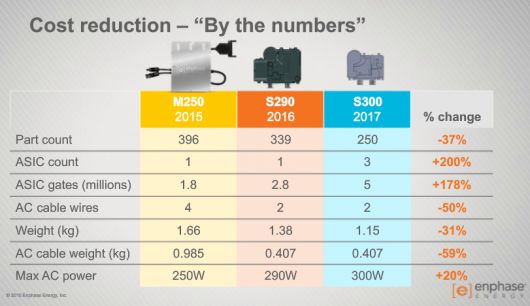

Bold microinverter cost-reduction targets

During an analyst day earlier this year, CEO Nahi said the company would scrub out 50 percent of the microinverter's cost in two years and reach parity with string inverters at 10 cents per watt. Nahi acknowledged that the time when customers would pay a significant premium for the Enphase solution has already passed. He added that the company must also move toward the larger energy market and provide complete energy systems for businesses and homeowners.

Enphase co-founder and CTO Martin Fornage spoke of the ongoing "fundamental research" and innovation going on at the firm.

Fornage offered some details on how the company will attempt to drive down cost. Enphase's next-generation products will continue to integrate more functions into the application-specific integrated circuit (ASIC) and reduce part count.

The company is moving to a lighter-weight polymeric enclosure that reduces grounding requirements and allows for a greater "freedom of design." He said the material allowed for the "lowest transformation cost" while solving some thermal and balance-of-system issues.

Deutsche Bank seems relatively sanguine about the company's prospects.

- "Market share appears to have bottomed in 2015 and the company appears to be regaining share at some of the larger customers (VSLR share is now 65% vs. 40% at the bottom). Most of the market share improvement has been driven by aggressive price reduction (ENPH prices are now at or slightly above SEDG prices of low 20s vs. string inverter companies in the high teens)."

- "Although ENPH expects pricing pressure to moderate in 2H (expecting mid-teens YOY price reduction), we remain somewhat cautious on the overall pricing outlook given the aggressive pricing strategy of string inverter companies."

- "We expect the company to deliver sequential shipments growth of over 30% with further sequential growth likely in Q3. Moreover, the company anticipates to recognize storage revenues starting from Q3 and expects about $10M-$20M revenues from storage segment in 2016, $50M-$70M in 2017. Margins in the storage segment are expected to be in the high teens/low 20s."

- "In terms of new product introduction, the company anticipates Gen 6 product launch from late '16 and expects cost to decline to 15-16 cents/W. Gen 7 is expected to be launched by end of 2017, early 2018 with a cost of 10 cents/W."

- "Finally, in terms of balance sheet management, the company plans to bring inventory levels down below $40M and although cash burn would likely continue through Q2'17, the company appears to have sufficient liquidity through that timeframe after the recent $25M second lien debt offering."

In any case, Enphase faces a harrowing product-development cycle, cost-reduction plan and production ramp on two new products which have to get done, on time and to spec, in order to maintain the company's market viability in microinverters -- and as a going concern.

41

41

15

15

9

9