Greentech Media's research partner in China, Azure International, will be discussing the China Wind market and a new quarterly market tracker in an upcoming webinar November 14th; register here.

In this article, we look at how the issue of curtailment is putting the brakes on the China wind market in some areas, and how the Chinese are responding.

***

For the Chinese wind industry as a whole, 2012 appears to be another year combining elements of the best of times and the worst of times. China surpassed 50 gigawatts of grid-connected wind capacity and is on its way to add a record amount of new wind capacity, increasing the total installed capacity by roughly 18 gigawatts, representing a 40 percent growth rate. In 2011, China surpassed Germany and the U.S. to become the largest wind country by nameplate capacity and is set to become the world’s largest wind energy generator sometime soon. China also currently supplies roughly one-fourth of all the wind energy injected into the grid worldwide.

Yet the sector faces some immense challenges, from ongoing problems with grid connection, ever-growing amounts of curtailed wind generation, new restrictions from State Grid on who can connect, and, perhaps most importantly, uncertainty about whether policymakers will do as they have done in the past to ensure the sector continues its rapid growth.

As recently as two years ago, it was already becoming apparent that China’s wind industry would quickly mature, and that policy would have to shift toward more rational allocation of capital toward projects with the largest potential to supply needed energy at low cost. The latest results from the third quarter of 2012 show that this rationalization is still some ways off: curtailment is still a huge problem, and industry profits are in a nosedive.

Developments shaping the China wind market in the past quarter of 2012 include:

- In the third quarter of 2012, China added an estimated 2.9 gigawatts of new wind capacity, including both connected and unconnected capacity.

- Total China wind capacity reached an estimated 71 gigawatts of nameplate wind capacity at the end of the quarter.

- China is on track to add a further 9 gigawatts in the fourth quarter and reach 80 gigawatts of total capacity.

The installed wind capacity in China rapidly increased from almost no capacity in 2006 to over 66 gigawatts as of the first half of 2012. In the process, China became the world leader in wind power development, installing approximately 35 percent of global capacity. From 2006 to the first half of 2012, China’s installed wind capacity grew 25-fold, while the installed wind capacity in the rest of the world expanded by a factor of 2.6.

The rapid growth of China’s wind industry has been, and will continue to be, concentrated in several wind power bases in Northern and Western China. Inner Mongolia currently dominates within China, with over twice the installed capacity of the next highest province, Hebei. Over the next three years, the installed capacity in Inner Mongolia and China’s other leading provinces is expected to rise by two-thirds when considering just projects currently in the pipeline. This is despite that fact that significant wind power curtailment problems have already emerged in these early growth regions.

Dealing With Curtailment

Curtailment remains one of the largest issues overhanging the future growth of wind power in China. There are several ways of looking at the issue of curtailment. The first is to examine historical data on curtailment, which is available from the China Electricity Council (CEC) data. Unsurprisingly, curtailment is centered on more rural provinces with larger wind capacity such as Inner Mongolia and Gansu province. However, the trend is to see curtailment expanding to other regions of the country, essentially following the latest areas of wind industry growth.

Another way to look at curtailment is to consider forecasts of future wind capacity additions by province compared to expected peak demand in those provinces. The ratio between wind capacity and peak demand would suggest that curtailment will worsen in areas already suffering from the problem, while continuing to expand to new areas.

A third, more comprehensive way to examine curtailment is to analyze projected wind capacity and peak demand when compared to projected additions of transmission and natural gas generation capacity. Without going into detail, while new transmission capacity will reach areas of high containment after 2014, it appears that it will fall considerably short of addressing the curtailment problem. Similarly, China’s natural gas infrastructure lags other countries, and natural gas power additions nationwide will be far lower than the projected increase in wind capacity.

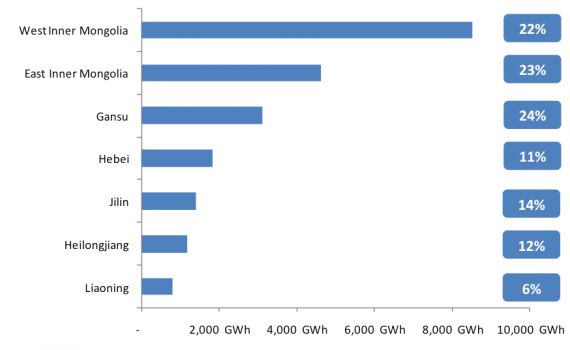

Figure 1: Wind Generation Curtailed, 2009-2011 and Percent of Provincial Total Wind Generation Curtailed, 2009-2011

Source: SERC, Azure International

In 2011, China’s provincial curtailment rates generally worsened. According to China Wind Energy Association, about 15 terawatt-hours of wind power generation was curtailed, representing 16.9 percent of China's wind generation -- implying an economic loss of RMB 5 billion, based on current tariffs. Based on the above data, from 2009 to 2011, the total wind power curtailment in North, Northeast and Northwest China was about 21,700 gigawatt-hours. The curtailed wind power resulted in a RMB 11.6 billion economic loss, which is equivalent to 6.77 million tons of coal, equivalent to 13.4 million tons CO2 emissions.

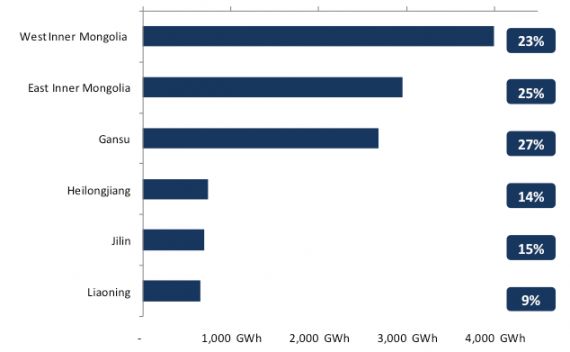

Figure 2: Curtailed Wind Generation and Curtailment Percent by Province, 2011

Source: SERC

In 2011, curtailment of wind power was most severe in North, Northeast and Northwest China, reaching a combined total of 12,300 gigawatt-hours and accounting for 16 percent of the total generated wind power. The curtailed wind power resulted in a RMB 6.6 billion economic loss, which is equivalent to 3.84 million tons of coal or 7.6 million tons of CO2 emissions.

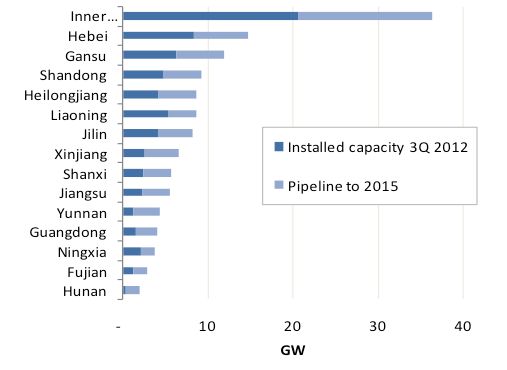

FIGURE 3: Wind Forecast by Province in 2015 (Top 15 Provinces), in gigawatts

Source: Azure International

An overview of our forecast wind capacity by province -- which in this case we have restricted solely to additions currently in our probability-weighted development pipeline -- suggests that curtailment will continue to be a problem for some years to come. All of the top wind provinces will see a higher ratio of wind capacity to peak demand, with six provinces marking a 20% jump in this ratio and another two seeing a greater than 10% increase. (Although the ratio is worst in Hainan Island, the province is small in terms of demand and connected to the much larger Guangdong province.) In particular, China’s Northeast and West regions appear particularly likely to experience increasing problems in terms of wind oversupply. Several of these provinces, such as those in China’s Northeast, are also far from existing natural gas infrastructure. Natural gas generation capacity can more quickly respond to changes in local intermittent renewable energy production, and hence can alleviate curtailment.

Looking to the Future

While China’s wind deployment continues to face these challenges, China’s renewable energy sector continues to build on it’s recent growth. On one hand, China’s renewable energy companies face the same problems of oversupply and problematic finances seen elsewhere. On the other, China’s policies in support of wind and solar will keep these sectors expanding at a rapid pace, unlike elsewhere in the world. China has quickly moved from being a bit player on the world renewable stage in 2006 to being the world’s largest market for many renewable energy technologies, especially wind. China now leads the world in terms of installed wind capacity, and clearly remains a relative bright spot for equipment and component sales. With the U.S. wind industry falling off its own version of the fiscal cliff while Europe struggles to reconcile older feed-in tariffs with new austerity measures, it seems clear that China will retain its new-found lead in renewable energy over the near term.

The implications of this simple truth are immense. They include:

• China will remain the largest market for wind equipment and components, including those supplied by foreign manufacturers.

• Chinese energy companies and renewable manufacturers will continue to grow rapidly and expand worldwide.

• Chinese companies will accelerate their bids for overseas assets, including renewable energy plants like wind and solar farms, as well as technology players. Chinese go-abroad moves will include rescuing financially hobbled companies like MiaSolé or taking stakes in more solid but still cash-strapped industry leaders.

Azure International and GTM Research will be discussing the China Wind market in greater detail on our upcoming webinar, November 14th at 12:00pm. To register, please click here.

41

41

15

15

9

9