It's a tumultuous high-growth era for residential solar in the U.S., and privately held Sunrun is in the thick of it. The company and its rooftop solar installer partners deployed about 100 megawatts of residential solar in 2013, half of what publicly traded market leader SolarCity did in the third-party ownership business -- but still ahead of SunPower and Vivint, according to GTM Research.

In February, Sunrun acquired REC Solar's Residential Division (solar sales and installation), AEE Solar (distribution) and SnapNrack (mounting systems). That made Sunrun a vertically integrated solar installer with trucks, as well as a financier with a direct sales force like SolarCity and Vivint. (Vivint's S-1 IPO registration form was disclosed today.) The REC acquisition gave Sunrun a large, established, multi-state direct-installer channel.

In June of last year, Sunrun won $630 million in three new funds. In April, Sunrun and Sungevity formed a partnership to enroll at least 10,000 new residential solar customers. Under the non-exclusive agreement, Oakland’s Sungevity will acquire customers, while Sunrun will finance the rooftop installation and own the PV system. In May, Sunrun announced that it closed $150 million in equity financing led by an unnamed public institutional investor, along with existing investors Foundation Capital, Accel Partners, Sequoia Capital and Madrone Capital.

"Sunrun provides marketing, financing, monitoring, and O&M services and uses installer partners that tend to be midsize and/or regional installers, as opposed to the very small dealers that SunPower works with. Sunrun is second to SolarCity both in terms of systems deployed in 2013 and funding raised (about $2 billion)," according to GTM Research's report U.S. Residential Solar Financing, 2014-2018.

We spoke with Sunrun's CEO Lynn Jurich, the co-founder of the No. 2 residential solar financier/installer, about the trends and changes in the market as residential solar scales big.

Channels, partners and vertical integration

Sunrun's channel model mixes its own installer fleet with those of other installer partners. "There’s been so much noise and speculation that vertical integration is the only way to go. Whenever I hear things like that, I want to go in the exact opposite direction," said Jurich.

She emphasized, "The channel model has thrived since the [REC] acquisition. You will see us adding more channel partners rather than fewer."

"In fact, our channel is stronger now, and it has grown more since the acquisition, including partnering up with Sungevity. Sungevity is now one of our channel partners, which I think is a real testament to the fact that we have a differentiated offering for the channel."

"I fundamentally believe that you need scale in this industry, but local entrepreneurs are always going to be a piece of the industry. There will always be 60 percent of the industry that’s going to be served by local solar installers. But these guys can really benefit with Sunrun. They’re competing against the SolarCitys of the world. So they can really benefit from having a partnership with Sunrun, where they can leverage our quoting application. They can leverage the brand. They can leverage our best practices. And what we found is that they actually like what we’re doing -- we have that direct business because we’re going head-to-head against the SolarCitys of the world. So we can bring that to them and [say], 'Hey, here’s what it’s going to take.'”

The End of the Investment Tax Credit?

While the industry anticipates the loss of a 30 percent Investment Tax Credit (ITC), Jurich agrees that solar can still be economic without that subsidy. "We think it’s doable. It’s going to be a challenge, but more developed-scale markets show that you can remove 20 percent to 30 percent of the soft cost, which gets you there."

As for the certainty of the loss of the ITC between now and 2016, Jurich suggests, "In Washington, two years is a lifetime." But, she added, "We want to plan for the ITC reduction, absolutely."

Loans for residential solar

The TPO model has peaked, and the declining cost of solar has made loans more viable.

Despite some tepid protestations to the contrary, Sunrun does offer loans. Jurich made this clear by saying, "We offer loans. We offer loans today. We offer cash purchase [options], and I think many people don’t realize that. We do offer both, should a customer have a preference."

"Sunrun completes approximately 200 loans per year with financial partners like local credit unions and banks," according to the company.

Jurich suggests that high customer acquisition costs overwhelm the difference in profit between leasing or owning. When you factor in the total cost of ownership, the advantages of leasing are immediate savings and access to service without the hassle of ownership (i.e., replacing inverters, insurance, monitoring, maintenance, etc.)."

"If you look at some of the variation in quality in terms of workmanship and equipment, I think we’re starting to see...some of the growing pains of the industry. We see variation in terms of different hardware manufacturers. We see variation in terms of quality of installation. And in a market where growth is the only thing that the people are perceiving, that’s a dangerous place."

The CEO suggests that the cost to manage a PV system and take care of it over its lifetime is "thousands of dollars."

Utilities offering solar

Earlier this month, Stephen Lacey reported that utility Arizona Public Service had decided to invest directly in rooftop solar. He wrote, "If approved by regulators, APS will install and manage 20 megawatts of PV systems on customer rooftops in Arizona using local labor, replacing a proposed 20-megawatt centralized solar power plant."

When asked about this plan, Sunrun's CEO responded, "I think it’s a good thing if they do it through their unregulated options. Absolutely. I think competition is good. I think competition means better value to the customer. I think it’s good that we have SolarCity out there pushing us and us pushing them. I think it’s what the consumer wants. So -- through the unregulated business, absolutely. I think when you put it into the regulated arm, it doesn’t make sense for society or for customers, I think, for a couple of reasons. The first one is that the rate of return that utilities are paid is higher than what the private markets will pay. Ten percent to 12 percent return is higher than what the private markets are funding, and that would be less effective…or worse, probably, for the consumer."

She continued, "I think another big issue is we are in the early days of this market, and there’s a lot of innovation to come. So, if we’re going to be cost-effective when that tax credit steps down," innovation is going to be needed in software and processes -- and that's more likely to happen due to the efforts of "a company with Silicon Valley DNA." Jurich added, "For the sake of this industry, long-term, you want it in the private markets."

"Again, one of the reasons why a private company is better at doing this than a utility is that we have the infrastructure to explain and manage expectations for the customer. It can be a somewhat complicated sale, and it’s a twenty-year sale. So customers need to know what they’re signing up for, how net metering works, what happens when they transfer the home. And I believe that private companies like Sunrun are in a position to explain that easily and to [earn] trust from the customer that we’re thoroughly explaining it."

Financing and the IPO

"I’ll be upfront. One of the things I would say is that we, in our last private funding, raised more capital and had a higher valuation than SolarCity’s IPO. I think a lot of people look at an IPO as the endgame. It’s not. It’s just a financing." Jurich said she believes Sunrun has the most effective capital structure, adding, "We believe that our current capital structure, the way we’re financing, is the most efficient. We’re watching the securitization. Certainly, it’s great to see innovation happening, but we believe that our current program offers a lower weighted average cost of capital."

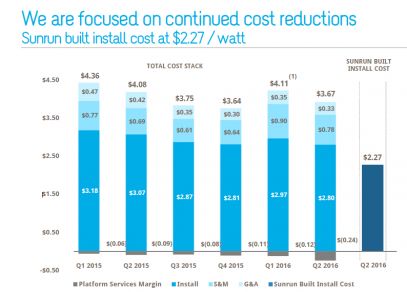

Source: GTM Research's U.S. Residential Solar Financing, 2014-2018

41

41

15

15

9

9