Last week we reported on something of a solar financing milestone when solar installer and financier SolarCity announced its intent to offer a private placement of $54.4 million of an "aggregate principal amount of Solar Asset Backed Notes."

That language may not be titillating to everyone -- but it means we've entered the world of securitized solar, and it's one of the first times it's being employed for distributed PV. It has the potential to lower the cost of solar financing while enlarging the finance pool.

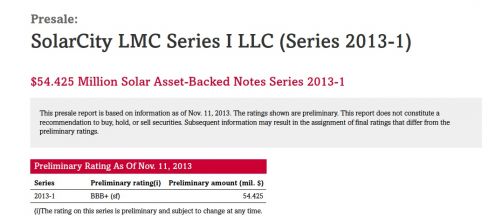

What's important here is the interest rate of 4.80 percent and the BBB+ rating granted by ratings agency Standard & Poor's. These are decent yields and ratings for SolarCity's first deal.

The eighteen-page presale document from S&P provides an unvarnished financial analysis of the difficult-to-analyze SolarCity. It also provides a treasure trove of facts about SolarCity's business and its customers. GTM Research analysts sobbed with joy for this early holiday blessing of solar financing statistics.

Here are some of the facts that warmed the analysts' hearts:

- S&P assumes a solar module degradation rate of approximately 1.3 percent per year

- Residential customers need a FICO of 680+ with no bankruptcy in the last five years in order to qualify for a lease or PPA

- The weighted average FICO score for a residential customer in the securitized pool is 762

- Weighted average PPA price is $0.15 per kilowatt-hour with a 2.07 percent escalator

- California, Arizona, and Colorado (the top solar states) account for approximately 90 percent of SolarCity's total portfolio. S&P views this as a weakness in the transaction.

How many SolarCity contracts have had to be "reassigned" because the customer moves, sells or defaults? (data as of Oct, 2013)

- 2.4 percent of contracts are "reassigned" (~900 systems out of a fleet of 39,000)

- Of this, 82 percent are because the homeowner moved in a normal sale of the customer's home (not associated with foreclosure, death or divorce)

- Of these reassignments, 91 percent have been "fully recovered" (with no impact to the original NPV of the contract)

- Of the 9 percent that weren't fully recovered, there is an average recovery rate of 78 percent, bringing the total average recovery rate of reassigned contracts to 97 percent.

- SolarCity has lost less than 1 percent of its planned revenue from contract reassignment

***

Securitization is one of the hot solar topics to be explored on the upcoming "Standardization and Securitization" panel at GTM Research's U.S. Solar Market Insight conference in December. Panelists include Yuri Horwitz, CEO of Sol Systems, Richard Mull of KPMG, and Nicholas W. Lazares, Chairman of the Board and CEO of Admirals Bank. Learn more about the conference here and register here.

41

41

15

15

9

9